In this episode of the EUVC podcast, Andreas discusses with Fatou Diagne, Founder and Managing Partner at Bootstrap Europe. If you want to get smarter on this topic, don’t miss our upcoming Masterclass on Structuring and deal terms in venture debt with Hemal from White Star Capital.

Bootstrap Europe is a venture investment firm currently raising the fourth fund, aiming for €350-400M, after closing Fund III with €157M. With €250M in assets under management, Bootstrap Europe is headquartered across London, Luxembourg, and Zurich. Bootstrap Europe targets companies in the post-Series A+ or Series B stage—those with venture capital already on their cap table, solid KPIs, or valuable patents and assets in place.

The firm’s sweet spot? European HQ’d companies, or those with European founders or VCs, with an upcoming allocation to support U.S. expansions. They even have 10% of their fund reserved for other exciting regions, like Africa. Bootstrap Europe specializes in geeky, transformative sectors: Deeptech, Life Sciences, Cleantech, Fintech, and SaaS, and some of their notable investments are:

Scandit (Swiss Unicorn) in Machine Vision

Blueprint Genetics (exited investment, Finnish tech used by Quest Diag during COVID - 1 of 2 largest labs in US)

Telensa: largest installed base of smart city lighting worldwide, bought by Signify

Recent undisclosed exciting investments in robotics, AI healthcare, food-tech, RNA tech

Watch it here or add it to your episodes on Apple or Spotify 🎧 chapters for easy navigation available on the Spotify/Apple episode.

Masterclass on Venture Debt: Structuring & Deal Terms with Hemal Fraser-Rawal, GP at White Star Capital

Join us for an in-depth session on Venture Debt with Hemal Fraser‑Rawa, GP at White Star Capital. Designed with senior VCs in mind, this masterclass will offer practical tools, insights and strategies to leverage venture debt in your portfolio.

Key Learning Points

Understanding Venture Debt: Grasp the fundamental principles and the strategic reasons behind using venture debt in investment portfolios.

Deal Structuring: Learn about the typical structures, pricing, and common features of venture debt term sheets.

Strategic Benefits and Drawbacks: Analyze the pros and cons of venture debt from an investor’s perspective.

Exploring Alternatives: Discover other credit-like financial products and understand their similarities and differences.

Geographic Considerations: Gain insights into the geographic nuances of raising venture debt and its implications.

✍️ Show notes

We believe in giving you our guests' thinking directly and unaltered. Therefore, no changes, no AI, no nothing has been done to the following sections.

A look at the person behind & The story of Bootstrap Europe

Fatou Diagne, Co-Founder and Managing Partner of Bootstrap Europe, a Growth Debt fund

Originally from Senegal, still have all family there and often go back (Dakar Art Biennale is one of the best in emerging art - visit in November ;-)

Most proud: apart from my 2 kids and husband? before Bootstrap, I helped set up a weather disaster insurance company in Africa that helped 1.3M people in the first year of operations : power of innovation when crossed with Finance = impact

Then with Stephanie, my partner, whom I have know since we were 17, set up a business advising entrepreneurs and family offices to put their money back into innovation. We managed some €300M and made successful investments in VC (Funds & Direct), PE, healthcare data, music royalties, distressed debt, etc. Growth debt struck us as a completely underserved industry and we sought to fill in the gap

Bootstrap was born with the desire to fund entrepreneurs solving the greatest challenges, across life sciences, software, energy, transportation, deeptech, material sciences, fintech.

We have together invested around €1bn across close to 400 transactions and now doubling down on European technology with new €300M fund IV

Great basis for business partnership was life partnership - rough travels as test / resourcefulness - how to make it happen

This became a solid foundation for the growth of our team and we have been able to recruit very very smart people, very driven

We are now raising our Fund IV, the past 12 months have been fantastic for Bootstrap as we closed our Fund III, we acquired the portfolio of SVB in Germany, we grew our team with fantastic individuals, continued to double down on the European tech ecosystem and have had some great exits in our deeptech portfolio.

Deep dive on trends in growth debt & current market trends.

1. Increasing adoption.

Definite increase in volumes and acceptance - unfortunately, not always for the right reasons in the current environment…

Step back - start with the definition of growth debt. Depending on data sources, the growth debt market - includes everything from true venture lending to bank lending, revenue-based financing, RCF, etc

The size of the European technology debt market is debatable due to the definition:

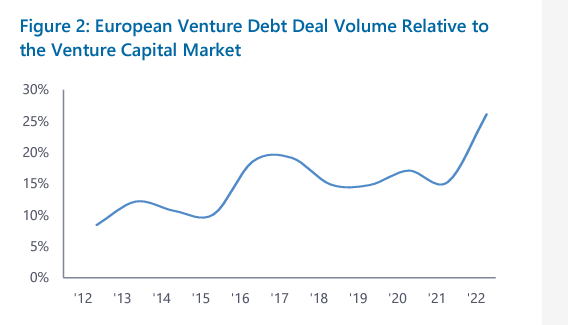

Dealroom & Atomico report - €3.8 bn in 2023, so 6-7% penetration

Sifted: in H1-24 €18.7bn in debt funding vs 47.4bn in equity, roughly 40%

So, the sector has clearly recovered from the double shocks of Spring 2022 and 2023 (Ukraine invasion and SVB bankruptcy)

In our own pipeline, we see a 9x increase since we started writing deals

U.S. VIEW: more elasticity there.

Key takeaways from NYC VD conference: lenders recovered very quickly from the SVB drama, and Q3-23 was a catchup quarter

That said, U.S. growth lending dropped 26% to $30.2bn in 2023 (vs$41bn in 2022 (National Venture Capital Association and Pitchbook)

It dropped again in 2024 by an estimated 20%

Contrasted picture of a resilient market where we are coming from under penetration.

What it means generally is that lenders have stepped up to support technology in Europe - funds are bigger and more ambitious, there are new entrants (banks, RBF), and generally better acceptance. Penetration has, therefore, increased as debt has been more resilient than equity.

2. Sector focus.

Growth Debt lends itself to 2 types of cases:

either sectors with a lot of intellectual property and what we call real tech (long developments, lots of IP, hard to replicate) or real assets or

sectors where unit economics can be stable and predictable and there is a recurrence in revenues (preferably contracted, but this can apply to some B2C)

Now have a look at the sectors that have grown the most in Europe in terms of funding over the past ten years.

We see strong interest in energy transition, healthcare, mobility, semis, etc. In general, deeptech has generated a lot of activity in our pipeline: robotics, semiconductors, sustainable construction materials, and AI-powered life sciences.

In line with the current interest in deep technology, climate tech, energy transition, and AI, these are the sectors that have generated a lot of activity in our pipeline: robotics, semiconductors, sustainable construction materials, and AI-powered life sciences love these sectors and pleased that they are back in favor with equity investors.

SaaS is the bread and butter of Growth Debt. However, it has faced the scissor effect of high historical valuation multiples and decelerating growth > need to grow into those multiples, or acquire yourself out of the issue >> increased growth debt financing as companies seek to delay valuation events

Interestingly, not as many software AI companies in our pipeline, either because they enjoy the hype of high valuations (and therefore debt relatively less attractive) or because quite early stage (majority still at seed and yet to generate revenues)

Life sciences have been a keen user of growth debt, as in this industry, more than anywhere else, the cost of equity has dramatically shot up - think valuations down 90% from the pre-crisis levels with companies trading at cash or discount to cash. Therefore, for quality assets, growth debt is a way to weather the storm until markets normalize.

3. Regional preferences.

Europe itself is a mosaic of over 27-28 jurisdictions, with differences in the historical structure of banking and financial markets, regulation, financial sophistication, and availability of capital that impact the appetite for debt financing.

Take the UK, the oldest and deepest market for Growth debt, and what we call creditors heaven - there is a lot of familiarity with borrowing and a lot of previous successes, with a deep and active market showcasing the various use cases of Growth debt.

On the opposite, you have Germany, where debt itself carries a negative connotation, “Schuld,” and company directors are very careful with borrowing due to their legal liability. Although a lot of education has been spurred, it brings back images of bankruptcy. Of course, a lot has changed, and are more selective as there remains some hesitation and maybe less familiarity with the model

Another interesting market is Spain. Debt adoption has exploded since 2020-21. We have been monitoring the market for a few years but noticed the willingness of entrepreneurs to take debt at very early stages before even finding product-market fit. Banks have “violently” entered the market, providing what they call “seed venture debt.” Great that there is more capital available, as there is still a gap at the growth level. But we are a little worried about the enthusiasm in putting loads of financial risk on top of your operational risk.

Generally, in Europe, and more so than in the US, equity has long been perceived as a factor of success, with fundraisings in themselves being an indicator of success. Wrong. Growing sales is the real success indicator, not just how much you’ve raised. In fact, we worked with researchers from various universities that show a statistically significant higher probability of success for debt-financed companies in the valuation they manage to negotiate. It empirically makes sense because if you have managed to raise equity from top-tier VCs, then passed through the filter of growth debt, and had the discipline to repay your loan, your business should be pretty unique and robust.

We are also pleased to see that there is more appetite for structured solutions than in the past. At Bootstrap we are capable of structuring complex transactions around specific assets or have an incredible speed of execution for time-sensitive M&A or exit situations.

U.S.:

As mentioned in the U.S. the use of debt is more systematically associated with each equity round

Also bigger is better - the average venture debt round has increased from $19M in early 2023 to $26M in Q1-24.

Economic influence & macroeconomic conditions.

1. Economic conditions.

U.S. start-ups have more beta - they are more sensitive to changes in economic conditions than EUR peers > investor in the tech market more closely tied to the stock market (think pension funds, endowments), interest rates, and inflation; therefore have a disproportionate impact on their sentiment and liquidity.

EUR start-ups rely heavily on government funding either directly (through subsidies, government-backed loans, guarantees, R&D tax credit, etc) or indirectly (the EIF probably supports 25-40% of the capital going into the tech ecosystem).

2. Investor sentiment.

In Europe, I almost felt we were reflecting Warren Buffet: “Be fearful when others are greedy and greedy only when others are fearful.”

U.S. Venture debt suffered more than EUR in 2023.

At the same time as SVB was being sold to First Citizen in the U.S. and SVB UK being sold to HSBC, when the German assets of SVB went for sale by the U.S. FDIC, everyone who is someone in European Growth debt had a look at the assets. Specialty lenders in Germany and large banks like Deutsche Bank considered it. The U.S. govt told some people to simply not bother.

The only continental European assets of SVB - It was a performing loan book. So really attractive.

We ended up winning the bid and integrating the SVB German portfolio in our books, thereby supporting the German ecosystem. It made us the largest lender in that geography, and fits exactly with our growth strategy.

We continued to double down on European tech, matching the push to create the champions of tomorrow in sectors like Energy, Semiconductors, Fintech, and Health Tech. I am proud to say that we have never been more active as we sought to work with our VC partners to support companies who either wanted to take advantage of market conditions and pursue attractive M&A opportunities or where the fundamentals of their own business were still solid but they suffered from the market conditions.

That said, everywhere, in U.S. or Europe, lenders became more selective and terms became a bit tighter.

3. Term changes.

Interest rates: move to floating rates after Ukraine invasion

Margin vs base rate has always been stable over the past 20 years. So when you move from 0% to 3.5-4% in Europe or 5.5% in the U.S., your borrowing cost increases that much

Tempted to say that U.S. growth lending is much more based on VC support, so almost always tied to a recent equity round

Some sorts of debt financing much more available in large deal sizes in the U.S.: eg working capital or equipment loans (think financing of NVIDIA chips, for instance)

4. Innovation in structure.

RBF for fast-growing consumer or SaaS startups

equipment based financing

revolver (seasonal businesses)

Increase complexity in terms and collateral packages > not a bad thing as for smart equity investors, this can unlock more borrowing capacity.

As borrowers get increasingly sophisticated, we see adoption reach similar patterns as in the U.S.

Market maturity.

Growth debt. vs. Equity.

Equity will always be No.1 source of capital because of the nature of technology development.

There is a normalisation of the use of debt, and actually, research shows a strong correlation between success and the ability to raise growth debt.

Negative experiences with debt would have been negative with any other source of capital - here it is more keenly felt due to the required repayments.

Key factor of success is figuring out the WHY of debt fundraising and ensuring you don’t pile up too much of it.

New players.

Banks:

before banks were worried about the impact of growth loans on their capital base due to Basel II requirment.

Now, the demise of Silicon Valley Bank has highlighted the beauty of its model on the asset side. The deposit base of SVB and the margins they were able to generate from FX, RCF, working capital, transactions, etc has led banks to consider the impact on their capital as a CAC in order to secure those deposits and the additional margins

Large asset managers: more present in 2021 and early 2022 than recently but some deals that have a profile of asset or equipment backed, we see large facilities being put in place. In Fintech in particular, when you think of onlending (Koyo Loans in Spain or Defacto in France) or large asset backed facilities (Northvolt in Sweden), it makes sense for a Citigroup, a JP Morgan or a Goldman to step in and charge juicy margins because these companies are not yet fully bankable.

RBF and programmatic lending: this form of lending is well adapted for startups with a high proportion of recurring revenues (whether B2B or B2C) and relies on an array of data points to assess and price the credit risk. In our experience, these end up being more expensive and less flexible than with a pure-play Lender. However, they have their role in the financing stack and work on certain amounts.

EIB continues supporting startups at the larger end of the spectrum (eg Northvolt 300M financing) even though some borrowers are becoming wary of the highly dilutive structures. EIB has rolled out very large facilities with highly dilutive equity kickers and put options, and startups who are not able to draw the full loan end up with quite an expensive structure. That said, they are one of the only ones who can mobilize very large facilities, state-backed, and therefore, they have their place in the market.

American players in Europe: we are not so sure where they stand with their European strategy - we have seen some come and go, others more active lately. Therefore, it will always be more momentum-driven. BDCs, in particular, have restrictions linked to the fiscal benefits they have due to their status and can’t invest more than 30% outside of “Qualifying Assets,” so that’s the most they can dedicate to European deals.

Future projections

Predicted growth.

Boring is beautiful in debt > steady increase and sophistication as the equity markets mature.

Don’t see splash entry of new players as it is repeat game due to the relationships that need to be created and nurtured. Complex jurisdiction landscape in Europe, Very technical

Continued upward trend due to high demand and state of equity markets

we see the level of knowledge and sophistication increasing all across the boards, specifically as repeat entrepreneurs realize that it is an extraordinary tool to finance their next success.

More collegial financing structures and perhaps increasing ticket sizes, as equity markets recover and lenders capacity increase

Brilliant future for European tech: Europe has come a long way and is catching up with the US: more IPOs (ARM, Birkenstock), more M&A exits and almost as much fundraising last quarter.

We always had a pan-European vision because you never know where the next billion dollar company will come out of: ARM in the UK, Skype in Estonia, Adyen in NL, UI Path in Romania, Mistral.ai in FR.

Very few teams have the breadth of experience and presence to cover the whole of Europe. We have one of the most diverse teams in the venture lending space - 11 nationalities: UK, FR, GER, CH.

Impact of AI and tech.

You would not believe the size of the tech stack you could end up with if you adopted all the latest tech:

note-taking software, deal sourcing database and AI, smart portfolio management platform, research and competitive monitoring, automated due diligence, fund operations, KYC, GPT-everything

we watch these developments carefully and so far have adopted a handful of AI-based tools in CRM with Affinity, in fund operations with Quantium, and in research / due dil with Open AI that allows us productivity gains of up to 30-40% - that’s huge! it allows us to focus on the interesting and valuable part of our business - people-to-people interactions.

Future thoughts.

Growth debt is just for growth for the most successful start-ups (only 2-5% of tech businesses can ever take the debt).

We will never do your copycat app or B2C company,

We like geeky technologies, and in the next cycle, we believe these will be successful.

If you are thinking about taking growth debt, start the process early, start the process when you still have a good runway, be straightforward with your potential lender, and run a process to ensure not only do you get the best terms for your company but the right lender to partner with you over the long term.

🤗 Join the EUVC Community

Looking for niche, high-quality experiences that prioritize depth over breadth? Consider joining our community focused on delivering content tailored to the experienced VC. Here’s what you can look forward to as a member:

Exclusive Access & Discounts: Priority access to masterclasses with leading GPs & LPs, available on a first-come, first-served basis.

On-Demand Content: A platform with sessions you can access anytime, anywhere complete with presentations, templates and other resources.

Interactive AMAs: Engage directly with top GPs and LPs in exclusive small group sessions — entirely free for community members.

🧠 Upcoming EUVC masterclasses

Advanced small-group sessions that take you from good to great. Lectured by leading GPs, LPs & Experts.

VC Portfolio Management: Capital Deployment and Reserve Planning

📅 Tue, September 24 | 4:00 PM - 6:00 PM CET | Lecturer: Anubhav Srivastava, Tactyc

Venture Debt: Structuring & Deal Terms

📅 Tue, October 8 | 11:00 AM - 1:00 PM CET | Lecturer: Hemal Fraser-Rawal, White Star

In-person Comprehensive Portfolio Modelling Masterclass

🌍 London 📅 Thu, Oct 24 | 10:00 AM - 1:00 PM BST | Lecturer: Marc Penkala

🌍 Milan 📅 Tue, Oct 29 | 10:00 AM - 1:00 PM CET | Lecturer: Marc Penkala

Benchmarking Session for GPs & LPs

📅 TBD - preregistration open now | Lecturer: To be announced 🤫

Got ideas or requests for future topics to cover? Let us know here.

🗓️ The VC Conferences You Can’t Miss

There are some events that just have to be on the calendar. Here’s our list, hit us up if you’re going, we’d love to meet!

Bits & Pretzels Investor Summit | 📆 30 September | 🌍 Munich, Germany

How to Web | 📆 2-3 October | 🌍 Bucharest, Romania

WVC:E Summit 2024 | | 📆 7-8 October | 🌍 Paris, France

North Star & GITEX Global | 📆 14 - 18 October | 🌍 Dubai, UAE

Invest in Bravery | 📆 21th of October | 🌍 Kyiv, Ukraine

0100 Conference Mediterranean | 📆 28 - 30 October | Milano, Italy

culttech summit | 📆 5-6 November | Vienna, Austria

GoWest | 📆 28 - 30 January 2025 | 🌍 Gothenburg, Sweden

GITEX Europe 2025 | 📆 23 - 25 May 2025 | 🌍 Berlin, Germany