EUVC Newsletter | 14.07.23

Yay - 10.000 Subscribers! 🥳 Read on for Lessons Learned from a GP's Postponed Fundraise, Raising Capital in The GCC, 9 mistakes LPs can easily avoid, 2023 European Private Capital Outlook

Firstly a heartfelt welcome to the 425 newly subscribed venturers who have joined since our last post! If you haven’t yet, join the 10,205 LPs, VCs & Angels that do or share it with your besties- as you can see. We’re super happy 😺😸

Table of Contents

Upcoming events:

Expand Northstar - the ultimate startup and investor connector event

TechBBQ - where hygge and tech meets

Lessons Learned from a GP's Postponed Fundraise

Raising Capital in The GCC

9 common mistakes Limited Partners can easily avoid when investing in venture funds by Samir Kaji

2023 European Private Capital Outlook: H1 Follow-Up

This Week’s Partner: Luca Faloni 💫

Still donning a suit to dazzle those LPs? Seems a bit much for the summer fundraising tours, no? We’ve partnered with Luca Faloni to get you dressed for success with great quality and durable products you’ll love.

Don’t settle, go discover their timeless looks, made from luxurious materials, crafted by skilled artisans in Italy and delivered directly to you. As always, free shipping & returns.

Upcoming Events

Expand North Star in Dubai - the ultimate startup & investor connector event.

15 - 18 October, Dubai

Investors are turning to new relationships as we continue to face challenges in a downturn. Join Expand North Star to discover Dubai, the UAE and the rise of the Global South ecosystems.

Gain insights on market access opportunities, and the latest on ADGM, Mubadala, and Catalyst Partners, as well how DFDF are transforming the global investment landscape with $1 billion target for assets under management by the end of 2024. You’ll connect with the people driving The UAE's digital economy to grow more than $140 billion in 2031and Dubai’s recently announced ambitious $8.7 trillion economic agenda for the next decade, known as D33.

TechBBQ - where hygge meets tech

September 13- 14, Copenhagen

7500+ attendees, 2600 startup reps, 340+ speakers, 620+ Scaleup reps , 880 investors and 150+ media reps. Clearly, TechBBQ has become the heartbeat of the startup and innovation ecosystem in Scandinavia. It began as a humble BBQ gathering for tech enthusiasts and entrepreneurs in 2013, but has since evolved into a large-scale summit that draws attendees from around the world for two days of inspiration, networking, and growth.

Lessons Learned from a GP's Postponed Fundraise

Today, I'm spilling the beans on some lessons learned from a GP's postponed fundraise. This post (and many others) would not be possible, if we weren’t LP investing as GPs typically don’t line up at the doors of the press to share their failures, but by marrying our investing, talking and writing, hopefully these learnings will help you on your journey in venture 💡

In these times of LinkedIn, twitter and now threads, we’re all too aware that life feels all about showcasing the wins and sweeping the setbacks under the rug. However, it is precisely in these moments of adversity that valuable lessons are learned and growth opportunities emerge, so let’s all be better at sharing these🌱.

Highlights from the announcement: 🌟

Fundraise put on hold due to negative market sentiment. ⛔

GPs plan to resume in the future. 🚀

GPs refocused on deploying their own capital, seizing sensibly priced investment opportunities. 💰

Recent investments: Series A in innovative entertainment venture and Seed round in sustainable mobile service provider. 🎉

Completed a follow-on investment. 🤝

Portfolio companies growing at a slower pace than during Covid but remain well-capitalized, improving profit margins. 📈

Two portfolio companies preparing for future fundraising rounds (Series A and Series B). 📢

GPs actively publishing thought leadership articles about their verticals and sharing insights on fundraising in 2023. 📚

Impressive 112% YoY growth in brand awareness and investment pipeline. 📈💥

Important note: we were already aware of this and were informed of the halt in the beginning of the year 💡

(Re)claim the narrative ✨💰

When things get tough, it’s all too easy to lose ownership of the narrative, but by tuning into the negative sentiment swirling around their vertical and geo specifically, they could reclaim the narrative and confirm that they’re focused on actively deploying whilst sharing exciting deal updates.

Transparency and Clarity in Pausing Fundraising 📣💎

A notable aspect of the GPs' approach was their lack of hesitation in pausing the fundraising process. Instead of pushing forward against the headwinds with some good ol’ posturing, they chose to be clear and upfront with both existing and prospective Limited Partners (LPs) about the decision. 🚫📈

This transparency demonstrated their commitment to maintaining trust and fostering open communication with their investors. The lesson here lies in the significance of honest and transparent dialogue, even during challenging times, as it cultivates stronger relationships and ensures alignment with stakeholders. 💪💬

The art of capital deployment 💰🎯

In response to the postponed fundraise, the GPs made a deliberate decision to focus on deploying their own capital, capitalizing on the availability of investment opportunities in the market. Importantly, this decision was supported by overall numbers, indicating that sensible and attractive investment prospects were indeed present 📊.

Reinforce trust with your LPs 💬🤝

By showing vulnerability through transparent communication, the GPs built trust and reinforced the mutual commitment with their LPs. The lesson here is the value of proactive communication and the positive impact it can have on investor relations, even during uncertain times. 🌐💡

The persuasive power of articulating thesis & strategy 📚

By clearly communicating their investment philosophy, market insights, and strategic approach, they (re)ensured that their target LPs had a comprehensive understanding of their value proposition. This emphasis on effective communication strengthened their positioning and facilitated alignment with investors who shared their vision 🗣️💪

Core learnings? Own your narrative at all times, reclaim it if you’ve lost control of it (even if by no fault of your own), be honest and transparent, and stick to your strategy.

Raising Capital in The GCC

Last week we shared that we’ll be going to Expand Northstar in Dubai and some wise (?) words from Jason Calacanis on exactly why the region is on fire concluding that now is a pretty good time to start building relationships in the region. For this week’s edition, I’ve asked our good friend Omar Hassan from MENA Tech Fund how to do just that. Let’s hear it from him:

The past five years have been phenomenal in terms of cementing Dubai's position as a truly global hub for technology, investments and business.

What that has created is a rush of venture capitalists coming here to raise what they think is "easy money" That boat has sailed!! However, there's plenty of smart money here, looking to build long-term mutually beneficial partnerships.

I would say to any fellow VC coming to Dubai to really be clear about:

What are you bringing to the table? Access to European deals isn't going to cut it, there are 101 other funds pitching that.

How is your portfolio or future portfolio going to fit into the MENA region? many of the strategic LPs or FOFs are looking for investors that can bring innovative technologies to the region or to their large operations here.

Where are the gaps currently in the venture community in Dubai / MENA and how can we close any of those gaps? There's no more room for generalist funds.

Your pitch deck won't get you far…..people buy people and if you don't have time to invest in meaningful relationships and partnerships then you better look elsewhere.

If you’re interested in diving deeper on this, keep an eye out for our upcoming episodes on the pod and check out this oldie but goldie with Sharif El-Badawi from Dubai Future District Fund 👇

9 common mistakes Limited Partners can easily avoid when investing in venture funds by Samir Kaji

David Cruz e Silva 🎙 ’s note: Oh, how I've witnessed individuals, enticed by their glamorous networks, foolishly throwing their fortunes at companies that ultimately sink faster than the Titanic. It's a bitter reality.

That's why I strongly recommend this piece by Samir Kaji where he highlights some of the common LP mistakes. Incredibly relevant for anyone thinking seriously about their portfolios and investment strategy.

Over the last 20 years, venture capital has increased its place in investor portfolios, primarily owing to a few factors: 1) Performance of the asset category relative to other categories (top quartile VC according to Cambridge Associates has averaged nearly a 28% net IRR from 1996-2019 2) Growing length of time tech companies stay private (over the past 25 years, we’ve seen the duration to exit go from 4 years to over 8 years) and 3) Increased influence of technology in our everyday lives.

For high-net worth investors, venture capital has historically been only 5-15% of their portfolios. However, as we’ve said many times, venture capital is something that is easy to do poorly, and very difficult to get right.

As such, it's crucial for Limited Partners (LPs) to be aware of common pitfalls and navigate their venture capital strategies with careful planning. Here are some common mistakes we see:

Investing cyclically: The venture capital landscape is not immune to market cycles. The investor frenzy that we witnessed from 2019-2021, followed by a retreat in 2022-2023, is a testament to this fact. Historical Cambridge data suggests that the top-quartile returns increased by 27% and 38% in the five vintage years following a correction, compared to the three years leading up to it. This underscores the importance of consistency in VC investing across market cycles and vintage years. A long-term commitment to VC allows the asset to self-fund over time (typically by years five or six), mitigating the risks of high-point investing (and missing out on down market vintage years). It's prudent for investors to establish a desired asset allocation and maintain consistency in annual deployments.

Overrating track records: Track records are an important glimpse into a manager’s ability to execute. However, while it provides a reference point, it may not always be a strong proxy for future performance. Though studies have shown some level of performance persistence in venture capital, the reasons typically have to do with the “why” and “how” a manager has succeeded (or not). Additionally, track records take a long time to truly provide an accurate representation of a manager’s probability to perform. When looking at track records, investors must also consider micro (team / fund size) and macro (competition, economic) when making an ex-ante decision on a manager. In recent years, valuation methodology also needs to be further examined as it’s often possible a track record may be inflated (or deflated) due to the holding value a fund is keeping of a particular asset. A nuanced understanding of VC is required to understand how to go deeper than headline numbers.

Treating Venture as an index: Venture capital is not a monolithic industry, but a multifaceted landscape where a small percentage of companies drive the bulk of returns. It is an outlier business, and it's crucial to understand that the narratives that often make headlines are overly simplistic.

According to indices from Cambridge and Pitchbook, top quartile VC has historically outperformed bottom quartile VC by over 20 points of net IRR per year since 1996. This significant dispersion of returns underscores the fact that, like other private fund categories, there are good VCs, and there are poor VCs. The difference is that the return dispersion between these groups is vastly more prominent in VC.

As venture capital has fragmented across firm and fund types and stages, it's become increasingly challenging for investors to distinguish between opportunities. For instance, a $20MM seed stage fund cannot be compared to a $2B venture fund simply from a cash on cash return potential standpoint without assessing risk, cash flow (time to liquidity), and other relevant factors.

The venture market has arguably broken into three very distinct categories - small seed stage firms, multi-stage early stage funds, and growth-focused funds. Comparing funds across cohorts that have very different characteristics often leads LPs to inaccurate and incomplete comparisons.

Fees: When it comes to fees, they are indeed an important metric and need to be taken into account. However, the ultimate objective when investing in VC is maximizing net return performance. We often hear investors state they won’t invest in funds over the long time standard of 2/20. Instead, the analysis should be whether the fee structure presented by the manager is justified and can still provide the appropriate performance (i.e., top quartile returns).

Many of the top funds, including Sequoia, have 30% carry structures, yet they have consistently provided performance to investors. Fees shouldn’t be ignored in the analysis, of course, but they shouldn’t be a single data point to be dogmatic around.

Ad-hoc Investing: A common pitfall in VC investing is the tendency to select funds based on a one-off assessment, without enough evaluation as to overall portfolio fit. Successful VC investing requires careful portfolio construction and an understanding of how different investments correlate. It's not just about picking winners; it's about building a balanced, diversified portfolio that can weather market volatility and deliver sustainable returns.

Momentum Investing: The Fear of Missing Out (FOMO) is a common phenomenon in VC. Whether it's market-based (like the late-stage investing frenzy of 2019-2021) or sector-based (AI funds, Web3 funds), caution is definitely advised. When trends become hot and apparent to everyone, marginal companies get funded at inflated valuations, increasing risk and depressing returns.

Market Timing: The average VC fund deploys capital over 3-6 years, yet some investors attempt to time the market, waiting for valuations to decrease further or something else to happen. In a long-dated asset category like VC, where funds have built-in time diversification, market timing is ineffective and often counters return optimization. The focus should be on deal quality and manager expertise, not on trying to predict market movements.

Self-sourcing direct deals: While investing directly in companies and co-investments can be exciting, it's also risky. Most startups don't return 1x capital, and if you're not fully immersed in the field, the risk of adverse selection is high. We've seen individuals invest in companies based on their networks, only to underperform due to the skewed risk/return profile of these deals. Remember, over half of VC funds each year, run by full time professionals, underperform (below median) relative to expectations. A more effective approach is to start with fund investments and gradually move towards sponsor led co-invests, and then ultimately self-sourced direct deals.

Diversification: Diversification is crucial in VC, both across time and managers. Each year, 30-50 companies (at the high end) drive the majority of returns. Ensuring sufficient coverage, particularly in early-stage investing, is key to capturing these winners.

VC investing is a complex and dynamic field that requires a strategic approach, a long-term perspective, and a deep understanding of market dynamics. It's not about chasing trends or timing the market; it's about building a diversified portfolio, staying committed through market cycles, and focusing on deal quality and manager expertise. As we navigate the venture capital landscape, Venture capital (VC) is a journey, not a sprint. It's a marathon that demands a steady pace, a clear vision, and an unwavering commitment to the long game. The venture capital landscape, with its ebbs and flows, the rise and fall of trends, and the constant evolution of sectors and technologies, is a dynamic and complex field. As such, it's crucial for Limited Partners (LPs) to be aware of common pitfalls and navigate their investment strategies with prudence and foresight.

2023 European Private Capital Outlook: H1 Follow-Up

As we reach the halfway mark of 2023, it's time for a comprehensive update on the European private capital landscape. The year began with a deceleration in PE and VC dealmaking, in Europe, according to the H1 2023 European Private Capital Outlook by Pitchbook.

The scarcity of large deals became evident as PE buyouts, which heavily rely on debt financing, faced the challenge of rising interest rates and increased capital costs. Consequently, PE firms became more selective in their deal completions, leading to extended due diligence processes.

So, the VC landscape saw a decline in large deals with lofty valuations, resulting in a slowdown in dealmaking across financing stages, geographies, and sectors.

Here are the key takeaways from the report:

Take-Private Deal Value Will Reach €30B.

The take-private deal value is falling short of expectations, reaching only €1.7B across 14 deals by May 31, 2023. The year-end target of €30B is unlikely to be met.

Surging interest rates have reduced the use of leverage in PE dealmaking, resulting in less activity and fewer potential targets for take-private transactions.

Cooling inflation rates and a potential slowdown in interest rate hikes could lead to a more transparent economic outlook and benefit public company share prices.

The unpredictable nature of the PE landscape makes it challenging to make accurate predictions about take-private activity.

€45B Record of Dry Powder in The EU VC Ecosystem

The European VC ecosystem is projected to have a record €45 billion of dry powder in 2023, driven by solid fundraising and cautious capital deployment due to economic and geopolitical uncertainties.

Nontraditional investors, shifting their focus from traditional stocks and bonds, have contributed to the growth of the European VC ecosystem.

Fundraising has remained strong, reaching €6.8B, while VC deal value has decreased by 32.1% in Q1.

Rising interest rates and limited capital availability have led VCs to hold onto dry powder for funding future investments.

The level of the dry powder depends on factors like the severity of recessions, business confidence, and potential shifts in investor focus to other asset classes.

The record amount of dry powder is not expected to be quickly deployed, as venture capitalists exercise caution and diligence in their investment decisions.

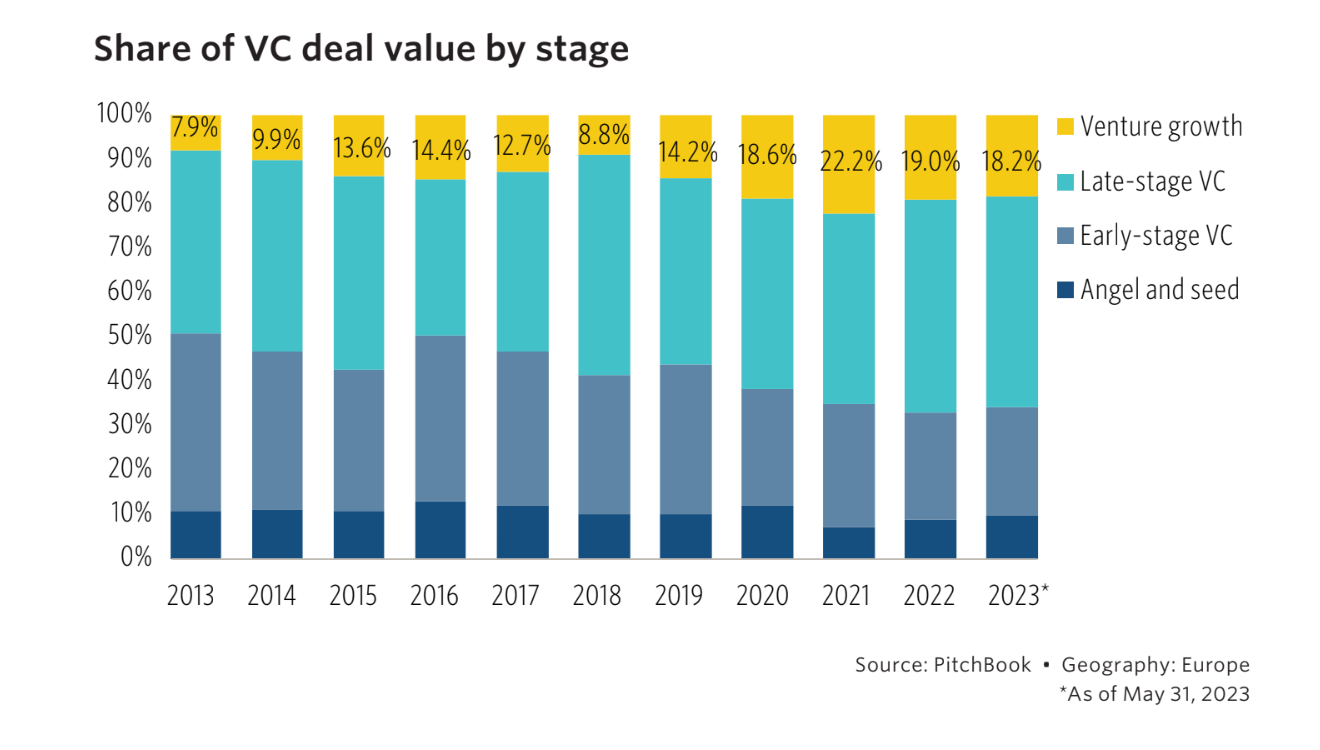

Venture Growth will make up 25% of Total Deal Value in Europe

The venture-growth stage in Europe was expected to account for over 25% of all deal value, driven by the rise of unicorns and late-stage businesses.

Nontraditional investors are particularly interested in the venture-growth stage due to larger investment sizes and the potential for IPO exits.

Abundant capital within the VC industry has allowed companies in the venture-growth stage to remain longer in the ecosystem, providing insulation from public market volatility and regulatory costs.

Deal sizes in the venture-growth stage have decreased, with a shift towards early-stage deal value.

The number of new unicorns in 2023 has been relatively low compared to the previous year.

US investors will participate in a quarter of all deals

The European VC market has historically been smaller than the US market, but it has been growing and attracting capital from outside the continent.

European cities like London, Paris, and Berlin have improved their regulatory frameworks for startups and have seen significant growth in deal activity and capital investment.

European cities are climbing the global ranks and challenging more significant VC players in China and the US, with Stockholm and Tel Aviv emerging as local VC hubs.

Recent European success stories in VC funding rounds have involved US participation, and US VC firms are establishing teams and offices in Europe to explore regional opportunities.

US valuations tend to be higher than European valuations, making European investments more attractive to US investors.

Tired of your back-office? So were we...

Take your syndicates or funds to the next level with Vauban’s funds and SPV services - and don’t forget to use this form for a very special treatment 🫠