Welcome tothe newsletter that rounds up the week in European Venture from a GP/LP perspective.

And heartfelt welcome to the 52 newly subscribed venturers who have joined us since our last newsletter! If you haven’t subscribed, join 7,109 angels, VCs and LPs by subscribing here:

Help us connect European ventureby sharing the below super promotional pre-written email with your friends 💖 we’ll buy you a 🍻 next time we meet for it!

New report on getting the most out of your deal sourcing efforts 🤓

How do you source deals?For most VCs, Affinity.co is the go-to CRM. But do you know how to get the most out of it?

The team recently put out their 2023 VC Investment Sourcing Guide and I think it’s well-worth a read - and the perfect hand-out to your associates and analysts (!).

Been wondering how some dealmakers remain successful in the face of a shifting market? Register today and see what Affinity's Relationship Intelligence conference, Campfire London, has in store for you on February 8!

🤔 Why track records are so important 💾 What data's required 📈 What the track record should cover ⛔ Top 3 mistakes made by VCs 🧙♂️ Why storytelling is key and how to compensate for a thin record (so far).

About Michel & Betterfront: Michel is the CEO and co-founder of Betterfront, a B2B vertical SaaS company dedicated to private markets. Previously, Michel led due diligence and fund managers selection for the Siemens’ pension fund. He started Betterfront out of his frustration of poor alternative investment analytic solutions.

What we listen to 🎧

The European VC, #143 Chris Wade, Isomer - Part 2

Today we are happy to welcome one of Europe's true OG LPs: Chris Wade, co-founding Partner of Isomer Capital. With an extensive career as a founder, startup mentor and LP with more than 50 Venture fund investments under his belt, Chris is a guy you should want to know. At Isomer, Chris co-leads their fund investments and leads their co-investment program - and has a weekly section in the EUVC newsletter where he shares his perspectives and learnings from the week gone by. Tune in for the second of a two-part episode where we reflect on the year that has gone by and predict what is in stock for 2023.

In this episode you’ll learn:

Why Chris believes 2022 was a year of landmark achievements in technology that we should all remember and why perseverance and necessity are key to innovation

Why 2022 was also a year of tears, how Chris thinks about the war in Ukraine and it’s impact on society and venture capital

What gives Chris hope going into the year of 2023

The European VC #142 Chris Wade, Isomer - Part 1

Today we are happy to welcome one of Europe's true OG LPs: Chris Wade, co-founding Partner of Isomer Capital. With an extensive career as a founder, startup mentor and LP with more than 50 Venture fund investments under his belt, Chris is a guy you should want to know. At Isomer, Chris co-leads their fund investments and leads their co-investment program - and has a weekly section in the EUVC newsletter where he shares his perspectives and learnings from the week gone by.

Tune in for the first of a two-part episode where we, in this instalment, explore.

In this episode, you will learn:

How Chris’ path as an entrepreneur has formed his thinking and behavior as a limited partner

Why Chris chose to devote his life to found and build Isomer Capital

What guides Chris as an LP and how it informs you in your work with LPs

Why venture capital is like the road to enlightenment for a buddhist monk

The UrbanTech VC #09 Mobility in cities - a political entrepreneur’s view - Martha Marisa Wanat, Young Leaders Academy

Mobility New Designs and Society for Urban Mobility. She is a political entrepreneur, sustainable mobility expert, singer and speaker! Martha is part of the founding team of Young Leaders Academy (in partnership with URBAN FUTURE), a value-driven education and consulting collective by and for the next generation of sustainable urban development.

In this episode you’ll learn:

what are different concepts & role models mobility wise in Europe (e.g. Pontevedra - but also Aachen)

the role of moderators is essential in projects with citizen participation

without winning citizen’s heart it will be hard to get them on board

what characterises political entrepreneurship

GIFs & Memes 🙊

🚨 View the newsletter in browser to watch the films without it being a mess. Promise it’ll be worth it.

This week’s stories 🗞️

No, venture capital will not change fundamentally - PT 2

The game of the last five years—at least—is over. And no one really knows how to play the next one. For years, venture capitalists focused on backing companies they believed would be marked up by late-stage private investors like Tiger Global Management. “Picking winners” meant picking companies that could raise a big growth round at a higher valuation. But those growth investors have retreated and a new strategy is needed. Every venture capitalist I talk to has a different view on what will emerge. Will investors go back to basics and back proven founders? Will they go far afield and look for investments in newer, riskier growth areas? I’m not sure investors at the same firms are even on the same page. This is all getting sorted out now. "

As said, David felt he had to give his perspective:

𝐀 𝐍𝐞𝐰 𝐕𝐞𝐧𝐭𝐮𝐫𝐞 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐏𝐥𝐚𝐲𝐛𝐨𝐨𝐤 𝐢𝐬 𝐍𝐎𝐓 𝐧𝐞𝐞𝐝𝐞𝐝 I cannot overstate how much I disagree. Might it be because of structural differences between #Europe and US?

🧓 𝐄𝐯𝐞𝐫𝐲𝐨𝐧𝐞 (𝐰𝐡𝐨 𝐡𝐚𝐬 𝐞𝐱𝐩𝐞𝐫𝐢𝐞𝐧𝐜𝐞) 𝐤𝐧𝐨𝐰𝐬 𝐡𝐨𝐰 𝐭𝐨 𝐩𝐥𝐚𝐲 𝐭𝐡𝐞 𝐠𝐚𝐦𝐞 -> According to Atomico's report, 31 #unicorns were created in 2022; ap. 50% more than the last 5 year average excluding 2021 -> 100 unicorns in 2022 says more about hype than value creation -> In 2020 $40bn was invested, in 2022 $80bn was invested. We are 18% down from 2021; but 𝐢𝐭’𝐬 4𝐱 𝐭𝐡𝐞 2020 𝐧𝐮𝐦𝐛𝐞𝐫! -> It's horrible that 14k employees of European headquartered startups lost their jobs. But let's remember that in 2021 all board room conversations revolved around: "it's so hard to find people and costs are horrific!" -> 2021 was an aberration where FOMO ruled. Check session with Chris Wade: https://lnkd.in/dG-aF-u6 -> It’s 𝐮𝐧𝐝𝐞𝐧𝐢𝐚𝐛𝐥𝐞 that there’s continued long term growth in one the world’s most interesting venture markets (i.e. EU)!

🚫 𝐒𝐞𝐜𝐮𝐫𝐢𝐧𝐠 𝐟𝐨𝐥𝐥𝐨𝐰-𝐨𝐧𝐬 𝐢𝐬 𝐧𝐨𝐭 𝐰𝐢𝐧𝐧𝐢𝐧𝐠 -> The inflow of US later stage investors in Europe is a recent phenomenon that marked 2021/2022 -> VC (& returns) existed way before this -> The toolkit to hunt unicorns (based on valuations - aka wishful thinking) is very different from the toolkit to hunt dragons (startups that return a fund - aka cash in the bank) -> Learn more about dragon hunting with Nico Goulet: https://lnkd.in/dnuuafhu

All in all: 1️⃣ If company fundamentals grow, so will the long term valuation (it only really matters at time of acquisition/exit). 2️⃣ Many sectors (such as Climate Tech 🌱, Life Sciences 🧬, Deep Tech or Sustainability ♻️) have remained resilient. 3️⃣ Same goes for early stages with some preliminary data showing no changes in valuations, and some evidence of increasing valuations 😲.

Securing followons is not winning, but it's still one of the key metrics for early stage VCs (MOIC) that make sense while you operate your first two funds. Actual returns (DPI) only start making sense around a decade after launching your first fund.

Also, if follow-ons are not secured, most of your portfolio dies and so does your fund and your chances to raise another one. So while it's not winning, it's a requirement to have a chance to win.

Moreover, a lot of early stage VCs used to sell early to later stage VCs during the last few years, to provide liquidity to their LPs. This will probably disappear (or at least slow down) in the next few years, removing one sure way of monetizing your top portcos early.

So in this regard I'd say I agree with the author of the article that new measures will be necessary, especially for those less patient early stage funds (i.e. funds will less patient LPs) which relied on exiting to later stage VCs.

Interestingly, the part I’ve bolded in the above by Borys runs contrary to what I’ve heard a few too many herald lately … let’s make less risky bets and take money off the table earlier. Anyways. Joe Schorge pitched in:

Media seeks attention, and extreme statements get more attention. Unfortunately its common in VC markets, we are already prone to extreme statements. What's great, and a sign of market maturation, is that in this cycle there are more strong, rational and thoughtful voices to call it out, like you David Cruz e Silva 🎙.

Alongside tech/VC declines in 2022 we also had massive public stock declines/losses/valuation adjustments. Have you seen a lot of suggestions to shut down the stock exchanges and start over with a new playbook? (aside from our friends in DeFi/Crypto - go team!)

Companies need follow-on finance on their road to profitability, but that is not THE game. It is building strong companies, around strong products, and in my view with the least capital and dilution possible.

As others note, in VC its not a return until you can buy beer with it: cash to cash is all that matters. Interim 'valuations' are how we measure progress, and always a flawed measure.

So yes strategies adjust when trading is challenged and capital more costly. But stock and VC markets continue, investors make their trades, and we invest as usual - in good VC fund managers helping good entrepreneurs build good companies. 2023 is going to be great!

And now the greats are all on this, let’s hear it from Mike.

I don't think VC is fundamentally changing, the playbook is adapting though. The current problems were caused in part by quantitative easing, which (for this cycle) goes back to 2010. At least for the Fed. Its not that the VC model is broken, people got greedy. Due to low interest rates a lot more money ended up in our asset class and due to more investment activity a lot more companies received (more) funding. One of the most unhealthy consequences that emerged imo: many investors started betting on the premise that quick follow on rounds will lead to quick value. Some managed to get out in time with secondaries or exits. Most, especially late stage, had to face the consequences last year.

Especially in the crypto space we have seen a lot of this 'quick in and cash out before the crash' behavior. When you look at the fundamentals, the 2008 crisis also has recognizable elements: cheap credit that fueled a housing bubble. On top of that banks started packaging those loans, increasingly with high risk mortgages, selling it to others until the bubble burst.

So changes in VC behavior at the moment are merely driven by those market corrections and thats healthy. I think we all agree that 2021 was completely out of hand. Greed and fomo typically leads to a bad outcome eventually. This is what we have to change, not business VC fundamentals. It’s the macro incentives that were flawed and kept for way too long imo.

That being said, I think other forces do change the VC playbook and fundamental changes are needed for certain categories.

Certain impact categories, for instance, need longer fund cycles. There the traditional 10 year cycle is flawed.

Also, we have seen the power of mega funds and the increasing amount of early stage niche funds. I wonder what will happen in the middle.

Finally, I think we will see more and more open/hybrid fund models and also funds that operate more like startups. At least partly product driven. Data is going to play an increasingly important role.

Mark Harré, co-founder of 2bX and host of The Urban Tech VC podcast pitches in and reminds us all not to bitch.

Venture Capital as an industry is feeling typical growth pain at the moment if you ask me. The whole industry has indeed been built around valuation step ups in follow on rounds. We have been so high on crazy unjustified valuation step ups the we forgot that at the end there is only one KPI that matters in the game. Money on Money, and I mean real money, NOT paper money!

VCs have been telling stories about decacorns while ignoring that the majority of tech exits always have been mid market deals sort of. IMO the playbook of the past years has been irrational madness nothing else. We need to get back to basics of our business.

Stop complaining about high interest rate environment and acknowledge that many of the venture hall of famers have built their funds in times of "high" interest rates. It is possible for sure we just need to remember the basics of our business...

Now let’s round it off with a comment by Anthony Danon, co-founding partner of Cocoa 🍫 (and also our beloved co-host on The Super Angel Pod) 👼

The last year and a half+ has been a period of extremes and some of the fundamentals got diluted from extreme behaviour (e.g. focusing more on up rounds and short term valuation uplifts than what the companies would become at scale). The short-term feedback loops encouraged more and more capital invested and raised and a virtuous cycle around that.

That being said, core fundamentals of VC are unchanged in my view so i very much agree with you David Cruz e Silva 🎙!

(In Europe) Currently seeing adjustments in the market at early-stage around being more disciplined (although it's an industry made for exceptions ;) and on putting more weight on how companies evolve at scale (multiple profile, etc) + the importance of fundraise risk. Some rethinking on exit strategies of Seed/early-stage funds and protecting against down markets / structured rounds but that is part of a broader evolution of the thinking of managers as the ecosystem matures.

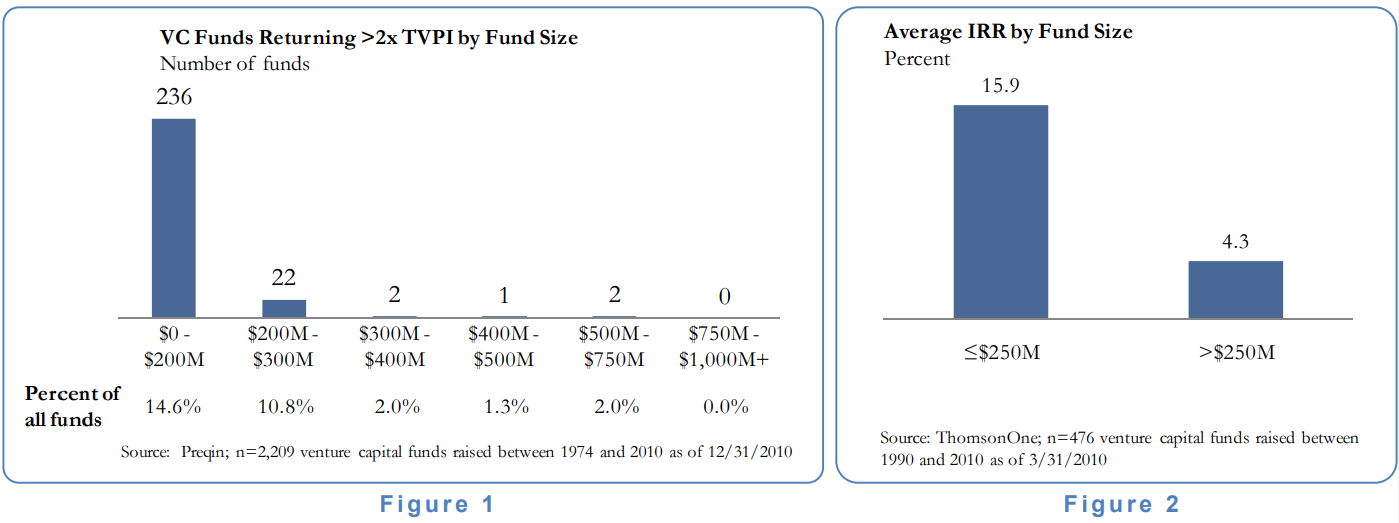

No venture fund larger than $750M has ever returned more than 2.0x to its limited partner investors. Fewer than a dozen funds larger than $300M have. On the other hand, over 250 funds smaller than $300M have cleared that same bar (Figure 1). A similar gap exists when performance is measured by cumulative IRR, which is 15.9% in funds smaller than $250M versus just 4.3% in funds larger than $250M (Figure 2).

In spite of the clear performance difference by fund size, venture capital has become increasingly concentrated in large funds since 1998, with 50-60% of all new capital raised in the asset class committed to funds larger than $300M. Before 1998, fewer than 40 venture funds over $300M had ever been raised. Since then, more than 600 funds have. Unsurprisingly, overall returns for the entire asset class have declined over that same period (Figure 3). This increasing concentration, combined with the systemic challenges in the U.S. market for initial public offerings3 , accounts for much of the reason venture capital returns have struggled in the last 10 years.

The inescapable conclusion from this data is that larger venture funds generally underperform smaller funds, despite the presumed advantages of track record and brand name that allowed them to raise such large pools of capital in the first place. But why is that?

Commonly cited explanations include: too many dollars per general partner, too many portfolio companies per general partner, and too much management fee per firm. Each of these contains an element of truth, but none fully explains why returns in venture decline with increasing amounts of capital under management, unlike in other private equity asset classes like buyouts or real estate. For example, buyout funds larger than $750M can return 2.0x or better to their limited partners, as 11% have managed to do since 1990, even though they have similar dollars per general partner and management fee profiles as a comparably sized venture fund4 .

A conclusion I have a feeling Mr Holle of Speedinvest would challenge (as he kinda did in our recently published episode with him diving into why they’ve raised 500M to do “Seed at Scale”) 👇

Kevin’s original conclusion also makes me recall our friend and fellow meme-lover Robin Haak’s recent post “Emerging managers consistently outperform - especially in times of crisis 👇.

Emerging managers are hungry, driven, with grit and passion, want to do better, often follow a vision and a thesis, and constantly improve and adapt to the market to make it fit. They have to outperform; otherwise, there is no second or third fund - as simple as that.

During this stagflation, we are witnessing a trend that accelerates - while companies in private and public markets become more efficient, Limited Partners are reevaluating their current portfolios and shifting their allocations. We see a "U-Curve," and with this, money from institutions, family offices, and High Net Worth Individuals is re-deployed in:

1) Professional FoF (Fund on Fund) who do the evaluation work, due diligence, and understanding of trends, we see them rising.

2) Shift to "Blue Chip" Venture Capital (e.g., Sequoia Capital, Verdane)

3) The atomization of VC in the early stage: Specialized Micro- and Nano funds and experienced Solo GPs

The mediocre are having a hard time fundraising. With that said, a "No first-time funds" investment rule handles not only legacy habits but also feels outdated, especially in a crisis. This time and these outstanding vintages ahead in the early stage are a fantastic time to reevaluate the portfolio strategy and adapt accordingly.

Talking about emerging managers, I like to share the following findings.

"We want our GPs focused on picking outliers, not creating them. Emerging managers can provide differentiated and diversified access to a pool of start-ups that more established brand names may not have access to." Jamie Rhode of Verdis Investment Management

"We look for managers whose investment strategy is tailored to their unique, durable competitive advantage, who have demonstrated that they add significant value to founders, and with whom founders and other investors love to work."Alex Edelson, Founder and General Partner at Slipstream

Emerging managers manage smaller pools of money and must invest before anyone else gets in.

Emerging Managers recognize new trends early; their existing funds do not bias them.

Emerging Managers are better networked – they have been start-up founders themselves and/or where the first line of contact in their previous position in a fund.

Emerging Blue Chips

One group Robin doesn’t mention in his post that I’d like to show some love is the emerging blue chips as well. Funds I’d advise that you keep your eye out for count:

- Altantic Labs(Berlin) who’s now on their 5th Fund and leading the charge in transformative tech.

- Hoxton Ventures (London) who just raised their 3rd Fund of >$200m for European Seed.

- 42 Cap(Munich) Currently on Fund 4, investing in Enterprise Software. Read their thesis here for an insightful read on this space that too many think they know all about.

And one that have probably crossed over to the promised land and become an furnishment in the hallowed halls of fame: Seedcamp, currently on Fund 5 and only going up 🚀 Remember, their first fund was only 2 M€ (albeit 10 years ago). Hear that story here 👇as well as the learnings from it.

Aristotle was wrong about a lot of things, but I quite like his conception of virtues as intermediates between too little and too much of something. For example, courage sits between cowardice and rashness. In a similar vein I try to find middle paths between ignoring threats and despairing about them, between dismissing opportunities and glorifying them, and between asceticism and hedonism.

Finding these balance points is an ongoing process as it is easy to be drawn away to either extreme. The story of Odysseus needing to navigate between Scylla and Charybdis can be read as a metaphor for this challenge. As an aside, the same is true for making choices in startups and I have a series of blog posts about that.

I am sharing this framework in the hope that it may be helpful to others. Also if more people start thinking and operating this way, maybe we can get past the current state of discourse which favors extremes.

May you all find the right middle paths in 2023.

James Heath’s predictions for 2023

This week, James Heath, Principal at Dara5, gave his predictions for 2023 - what do you think!? And as for his historical hitrate - go here to see his own evaluation of his ‘22 predictions. Spoiler: He did not see The UK having 3 Prime Ministers in one year, the passing of the Queen, or the crash (but tbh, who did!?).

🌊 Deployment speed will decrease - although there is more ($200bn+) dry powder than ever, it will take several years to deploy as mega rounds become rarer and fund due diligence intensifies. Fund cycles will be back to 2-3 years

2️⃣ Secondaries, secondaries - 2023 vintage performance will be led by secondaries funds. The entry points will also become so attractive that all funds will have to have some form of secondary strategy attached, both from a buying and selling perspective

💰 Valuations won’t go down further - average valuations across all stages won’t show any material changes from the last two quarters. Founders should choose downrounds over complex structures if the choice is faced

🛣️ Hardware will pave impact’s path - LPs and GPs must accept that hardware is a fundamental part in climate investing, in order to create real climate changing solutions. The energy shock highlighted the dangers of over relying on fossil fuels - hardware investments will be up in 2023 and this will be led by climate

♻️ A new wave of startups will fuel the gap left by the recession - Airbnb, Uber and Groupon all came along during the GFC, as a way for consumers to earn and save more money. New winners with this outlook will emerge in 2023, perhaps in the reusing / upcycling world

🌍 The MENA region will be the fastest growing region for VC funding year on year, which will be driven by its prospering younger population and LPs continuing to become ex-USA

🧐 There will be a signficant reduction in total capital raised by VC funds, as LPs reduce the volume of funds they enter. This will happen by up to 30-50% of 2021 and 2022 numbers. LPs who invest in 2023 vintages will be rewarded in years to come

🛩️ The smallest and largest funds will face the biggest battle to raise from LPs. Micro VCs are fundamentally important to the VC ecosystem but will find it the toughest. The most popular fund size will be $50m - $300m, where risk and reward is most optimised

🎬 Software companies will face a new three-stage demand contraction cycle; 1) new business will reduce by 50%; 2) churn will increase from c.15% to 25-30% as more companies go out of business; 3) seat contraction will occur as customers do not hire as fast and others make redundancies. NDR should be the key metric for investors over ARR growth 🏢 The office will be back - companies will turn attention to creating locally and as a result, the office will return. Expect employees to be in the office for a minimum of three days a week, with a day or two at home. A new wave of PropTech winners will emerge, facilitating office environments that will attract the best talent

❤️ Whatever happens this year, innovation is a heartbeat and isn’t a function of the world’s capital markets. When times are good, people start great companies. When times are bad, people start great companies. It’s easy to forget this after the rollercoaster of 2022!

Barack Obama’s 2022 End of Year Lists

It’s no secret I’m a big fan of Obama (like his politics or not, that voice is amazing - and all his books are narrated by himself as audiobooks on Amazon, so that’s a perfect fall-asleep-real-fast-routine right there 😍). Cool fact: the dude was barred from entering the democratic party’s convention just 5 years before he was elected President because he had bummed the wrong tickets from a friend. That’s a personal venture story right there. Either way, if you don’t know what to read (or listen to!) here’s a pretty good list to start.

2022 Reflections.. not!

It’s funny how our friends in European VC have the same humour 😁 Kudos to both for making fun of all of us who couldn’t refrain from feeling that everyone should know every single reflection we’ve had on the year gone by 👏

Business Insider’s article on VC predictions for 2023.

2023 (scary) predictions: VC firms go public, merging of solo GPs and micro funds, “the party round is over", {put yours in the comments}.

According to Melia Russell from Business Insider, the next year promises to be exciting. Top VCs shared their thoughts on what we’re going to see in 2023, here are the most interesting ones:

— “The party round is over,” claim VCs. Sounds flimsy to me, especially considering the fact that almost 25% of laid-off tech workers start their own businesses now. Most likely, they will turn to their network, looking for syndicating small checks, as it always was.

— Reaching a unicorn valuation will be significant and rare again; no more hundreds of unicorns a year.

— VC firms will go public as they look to access other sources of capital.

— Fewer first-time venture funds will launch; venture will consolidate. Solo GPs and micro funds struggling to raise new capital will be merging. That's a challenge that we at Uniborn are going to put out two cents into.

— The rise of the tech ecosystem in the Middle East and North Africa. VCs expect a lot of innovation from Dubai, Riyadh, and Cairo.

— Creators will birth the next iconic consumer app; the conditions are perfect for takeoff.

— Startups will gobble up their competition. The mental and behavioral healthtech category may see a lot of dealmaking.

🇮🇹 P101 - €150m; target €250m, fund 3, first close - Milano 🇱🇹 Practica Capital - €32m; target €70m, fund 3, 🌍 Baltics, first close, early-stage - Vilnius 🇺🇸 Beyond Capital Ventures - tbc, fund 1, 🌍 Africa, impact, final close - New York

"I am really enjoy reading to The Lowdown newsletters every week, I never skip any of them. In fact its one of the few weekly newsletters I read at all. The Lowdown newsletter really stands out with the relevant information that happened in the VC investing during the week, nuggets, commentary and it is all provided with the EUVC style that includes really spot on comments and also humor 😊 These guys constantly spit out the best content related to EUVC investing out there" - Dag Ainsoo, GP & CFO of Startup Wise Guys

Really enjoyed this week's read Mr. A. I' biased I know....