Investment Benchmark Report on European Venture

Unicorn stables swapped for graveyards, Europe is a tale of (at least) two cities, ClimateTech is hot hot hot, FinTech still deserves massive respect, and you're nothing but the sum of your email 💌.

Affinity just launched their Investment Benchmark report and we’ve been enjoying it. Read on for the eu.vc (satirical) commentary on select graphs and findings and dive deep to draw your own conclusions 👇

On the fence whether you should give it a read? You shouldn’t, the below is actual footage of a well-known German VC reading it from his tech-conference-escape-barn in the Swizz Alps.

The dry TL:DR

Unicorn birth rate drops 80% in Germany, 55% in UK and 45% in France. But don’t forget - 2022 still matched the birth rate of 2020!

Capital invested surged in a couple of geos: Croatia >400%, Iceland ~350%, Portugal >200% and Greece nearly 100%. Greece, Switzerland, Italy, Estonia, Serbia and Romania also saw near-50% increases.

Capital invested plummeted in others: Netherlands leading with a drop of more than 50% and Germany, Sweden, Norway and Lithuania following closely with ~40%. UK dropped 20% which is of course significant given the €€-volume this represents.

Climate tech getting almost as hot as the Earth’s atmosphere making regions like the Nordics continue their growth trajectory.

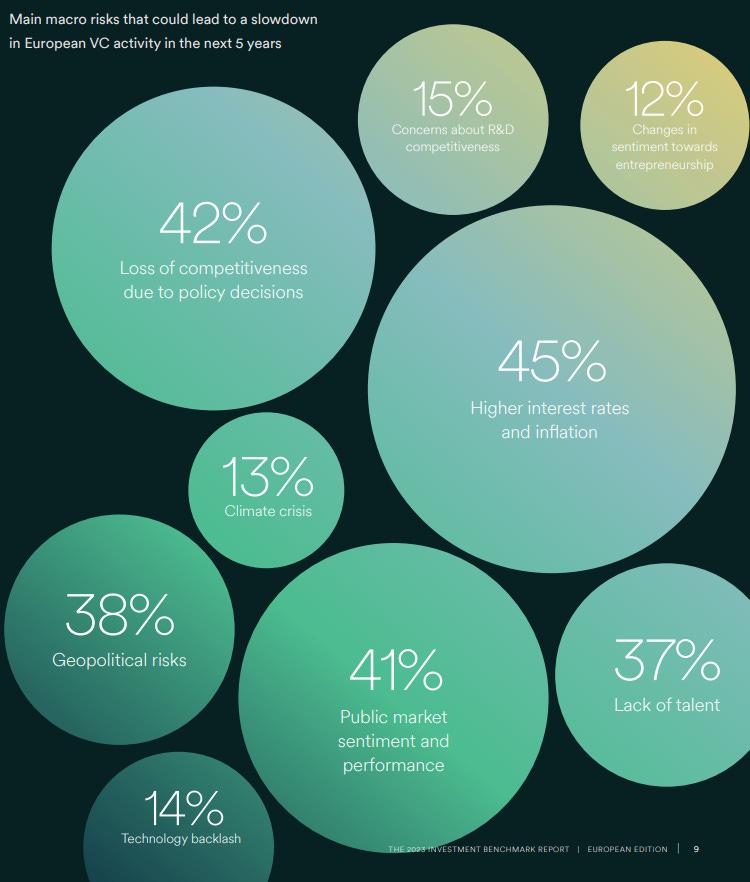

Interest rates, inflation, poor public marketing sentiment, and loss of competitiveness due to policy decisions are what’s most likely to cause a slowdown in European VC activity according to European VCs themselves.

You’re the sum of your email - Top European VCs consistently send more emails than their lower-performing counterparts.

Southern Europe is getting plugged in with countries like Italy, Croatia, Greece, and Spain growing their network from H1 to H2 of 2022 by a whopping 251%.

The snarky eu.vc commentary

Take away #1: What goes up must come down

Despite the downturn, the U.K., with its usual tech swagger recently taken to new heights by PM Rishi Sunak’s sitdown with The Fresh Prince of Tech Air Harry Stebbings, reclaimed its crown as Europe’s unicorn factory in 2022 reigned supreme with France, Germany and Sweden trading for the run-up spots.

And no doubt, the magnitude of the drop in unicorn minting that we all so viscerally felt during the Lord’s year of 2022 can definitely be seen in the numbers: The U.K. took a 55% hit, Germany a staggering 80%, and France a hefty 45%.

If this was Vanity Fair, Forbes or another far more read outlet than eu.vc, we’d continue this dissection of the numbers into analysis and conclude that VCs are finding their groove wielding tightened investment criteria in a market calling for steadiness with reliable returns favored over wild risk-taking.

However, this is eu.vc so instead we’ll leave it to Gimli to give us all the sage advice needed:

But if that doesn’t suffice. Here’s another:

Take away #2: Europe is a tale of (at least) two cities

I always find it a little funny to see graphs like this on an annual basis, ‘cos what do they really mean? Will Croatia sustain a 400% YOY increase in ‘23? Or will our Dutch and German friends see their VC economy shrink another 50-40% this year? Likely not.

Looking at this I think it’s wise to transcend the national developments and look for the regional trends. Doing so, it warms my heart (and feeds my ever-hungry wallet) that the emerging regions remain emerging, even through the troubling times of 2022 - onwards and upwards my friends.

Gotta love having exposure to these regions. If you don’t yet, it’s about time to get it (probably the only worthwhile advice you’ll get in this post, tbh, so you can stop reading now if you want 🧠).

Take away #3: Reshuffling in the Unicorn Stables

First, feast your eyes on this the below graph. While fintech obviously took a nose dive in 2022 (Thx Mr Bankman-Freid?) but a (huge) nod should be sent to everyone building in Europe’s fintech industry, nonetheless, as it’s grown at a rapid pace. In fact, London now ties with the Bay Area as the top global hub for fintech startups, having received a staggering $9.7B in investment in 2022.

Climate tech is another area where we’ve made significant strides with Europe having raised 42% of all climate tech dollars and growing 26% faster than the U.S. year-over-year (🥳).

Of course, Security and Gaming should not be disregarded, especially going forward with the entrance of very clever LLM’s (go Legal and RegTech?) and Gen AI more broadly.

Take away #4: ClimateTech’s getting almost as hot as the Earth’s atmosphere

Writing this end of June during the longest early-summer drought and being witty with this title feels almost like playing with fire, which we all know isn’t smart during a drought. Nonetheless, there it is. Luckily it seems like the famous dollar bill might be getting ready for a revamp.

Fun fact: the continued growth in climate was a significant contributor to the Nordic ecosystem allowing the region to achieve its second-highest year for VC funding in 2022.

So to all the non-climate VCs who enviously comment on the success of their climate counterparts’ fundraising traction, there’s only one thing to say:

After all, ClimateTech has been out of favor for yeeeears. Back then it was just called CleanTech. So let’s let them have it this time and just enjoy that the energy industry has managed to raise $34.6B across 1,388 deals in 2022 ⚡.

Take away #5: Refocusing on domestic markets

2022 was the year when both EU and US investors refocused on their domestic markets. U.S. investment 2022 dropped by over $10B, a 29% decline from the previous year, more or less matched by EU investment’s $8.3B drop in US rounds. Thumbs and smiles all around.

As a consequence, US investment now accounts for “only” 28% of all investment into Europe, down by almost 4% from 2021 and a similar drop in number of US investors is observed.

Take away #6: Oh lord help me, not again

Completely unrelated to the MAGA/MEGA picture above, loss of competitiveness due to (poor?) policy decisions comes in as the second biggest risk factor for European Venture’s continued growth. It’s truly interesting to see how startup, innovation, and job creation can be at the top of policy maker’s agenda at the same time as the tech environment perceives exactly that as a main risk for the sector 🤷♂️.

Adding to that, some would say that the main risk, Higher interest rates and inflation are as much the direct result of policy maker’s (sleeping) at the wheel. Before I get into more trouble, I’ll stop commenting on this chart and leave it for you to dive into. Dive deeper in the report here.

Take away #7: In VC, you’re the sum of your email

I tend to liken VC to highschool. For better or worse, climb the ladder of popularity and you’re on your way to success. And yes, that can be done in other ways than tweeting all day 🐥

So why do I say this? The Affinity report’s findings lend a pretty solid argument: First of all, top VCs work their network more heavily 👇

Secondly, data from the Affinity platform shows that ~45% of deals originate from a dealmaker’s existing relationship network and deals coming from warmer sources close 25% faster than their counterparts.

And overall, the network of top VCs is bigger and grows faster.

And to close this off, I want to bring your attention to something that truly stood out for me in the report: the top VC firms in the Southern region of Europe (countries like Italy, Croatia, Greece, and Spain) have grown their networks rapidly with an impressive 251% in network size from H1 to H2 of 2022 🚀.

Obviously, this has to be due to the emergence of some new top firms in the region, but nonetheless, sitting in the north of Europe, I’m celebrating that the days when Southern Europe was just a holiday destination seem to be behind us 😎.

Think we did a 🦀 job drawing insights? Go to the source then.

Think we did a bang-up job? Do share 💞

Great conclusions 👍 Take away #7 is my favourite 😂