Newsletter 2.11.23 | The LP Perspective on Why Now Is Europe's Time

If you're a fundraising VC, this is the newsletter you will want to put in your data room for all prospective LPs that are hesitant to bet on Europe 👀

Welcome to the EUVC Newsletter 🗞️

Join us in welcoming 567 LPs, VCs & Angels who have subscribed since our last post (yes, it’s been a month since our last ‘real’ newsletter)! If you haven’t yet, join the 18,017 insiders that do & share it with your besties🤗

Recently, our good friend Michael Sidgmore published an episode with Joe Schorge - Founding Partner of Isomer Capital on Why Now Is Europe’s Time. We loved it and have mined it to be able to share the wealth of insights with you.

Table of Contents

Listen to the AGM-podcast 🎧

The Hardest Thing About Raising Isomer Fund I

The Rise of Europe

What’s On The Mind of Global LPs When talking Europe

The Sustainability of The European Opportunity

European Capital Scarcity

The Influx of Government Capital

The Path to Unlocking European Pension Fund Money

Tapping Into The European Opportunity

Why Local Seed Funds Will Continue to Dominate Europe In Most Cases

Global Ambitions in European VCs

The Make Up of A European Top Fund

Picking Outlier Managers

The Secondaries Opportunity in Europe

European vs US VC performance

Advice to LPs and Allocators who are looking at Europe

Upcoming events

Why now is Europe's time with Joe Schorge & Michael Sidgmore on AGM.

In Michael’s words:

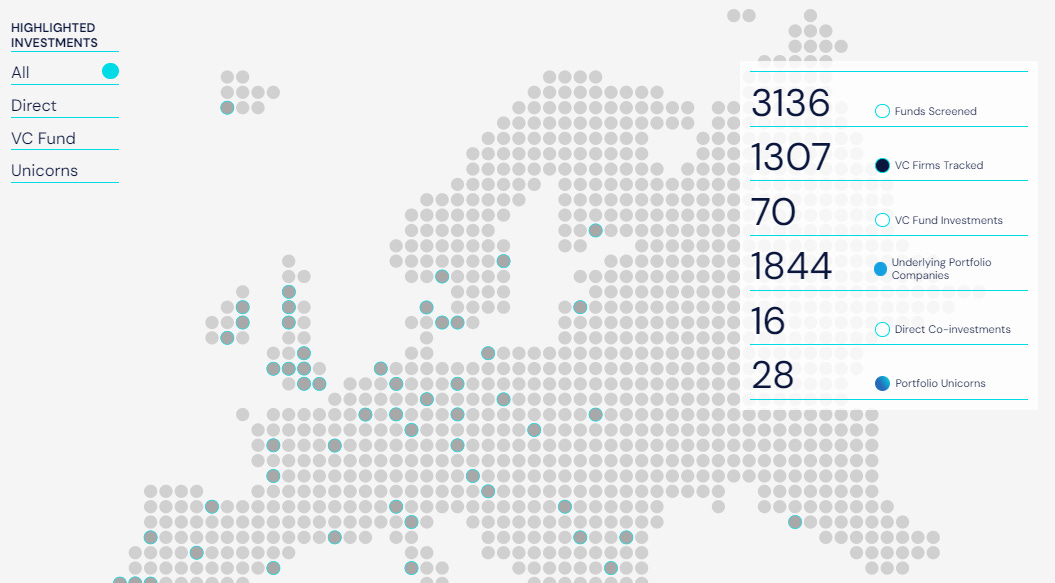

I discuss the rise of Europe with Isomer Capital’s Co-Founder and Managing Partner Joe Schorge. Isomer is a pan-European fund-of-funds, co-investment, and secondaries platform that is on its way to €1B AUM. They’ve invested in 70 VC funds, including the likes of Seedcamp, Hoxton Ventures, Atlantic Labs, and leading European companies like Sorare, Refurbed, Zenjob, and more.

Joe has a fascinating perspective on European’s tech ecosystem on a number of dimensions. He’s an American who moved to Europe in the late 1990s to work in tech before moving to the allocator and investor side. He worked as an investment consultant at Cambridge Associates, where he advised institutional investors in Europe and MENA on strategy, planning, and implementation that amounted to over $2B of capital across 75 transactions in private markets. He was then a Managing Director at Pomona Capital in Europe, where he focused on secondaries, fund investing, and co-investments, which paved the way for him to found Isomer as one of the early institutional pan-European fund-of-funds based in Europe.

Listen to the episode below and make sure to subscribe to Alt Goes Mainstream

This edition is brought to you in partnership with …. Moonbit

Safeguarding Your Crypto Journey with Moonbit

Experience automated, personalized portfolios tailored to your risk. With Moonbit, you're always in control using your API keys. Match your mood with strategies for every market.

Assess & align at moonbit.ai. Expert portfolios await.

The Hardest Thing About Raising Isomer Fund I

“The biggest problem was if you looked in the rear view mirror at European venture returns in the prior decade, they were pretty bad. Not pretty bad. They were just bad, just plain bad […] But you're investing for the future. And what we saw was really the seeds of greatness. “

The foremost issue was that when you glanced at the European venture returns through the rearview mirror of the past decade, the picture was grim. Not just mildly disheartening, but decidedly poor.

Europe had navigated through several cycles with sporadic successes, yet on an index level, the scenario wasn't persuasive. If a large institutional player took this to committee juxtaposed against elusive benchmarks, the argument fell flat. Nonetheless, investing today isn't an echo of the past—it's a pledge to the future.

What we observed were the initial sprouts of excellence. A meticulous analysis revealed the solid fundamentals—the burgeoning technology, swiftly generated revenue streams, and the economical facet of founding a company and marketing digital products. This scenario was rather fresh at the time. Today, it's a clear-cut trajectory, and investing in this upward trend appeared extremely promising.

However, presenting a compelling narrative to Limited Partners (LPs) to illustrate this promise was a challenge. It demanded a forward-looking, innovative mindset to invest at that juncture. Thankfully, we encountered a cadre of visionary LPs willing to venture forth and help build what Isomer has become today.

The Rise of Europe

If you look at the 90s and 2000 venture in Europe, you saw a lot of bankers and consultants who went into venture more focused on balance sheets than on building product and operations and what got me really excited was that all evaporated. And this new guard, which really came in the post financial crisis period, was built on the US model.

The significant shift Joe observed was when European VCs started adopting US tactics, marking a deviation from the traditional focus on balance sheets to a more product and operations-centric approach. This change, emerging post the financial crisis, reflected a US model, propelled either by exposure to the US market or the global hyper-network enabling shared learning across borders.

A decade ago, startups in Europe embarked with best practices and ambitions akin to those in US tech hubs like California, Boston, or New York. Applying such methodologies to Europe's market, characterized by capital scarcity yet abundant in tech talent and good founders, promised exciting returns. And indeed, it played out as anticipated, with the last 12 years bearing witness to this success, albeit with some ambiguity around 2015.

Fast forward to Joe’s near eight-year tenure at Isomer, the allure of Europe remains robust. The tech landscape here, rejuvenated post-crisis, echoes a global narrative: the rapid scalability of software in a hyper-networked world, with more fluid movement of talent and capital. Early investments, underpinned by a diversifying strategy, have opened avenues for outsized returns, a claim now substantiated by data, benchmarks, and a growing list of unicorns.

We were saying, if we're right, there would be lots of billion plus companies created. Well, now they're here. Many have exited and they've done really well. I used to make the case in every pitch. I don't so much anymore. It's a very different talk these days.

Conversations with LPs have evolved from advocating for Europe's potential to discussing how to navigate the changing dynamics, especially in the face of recent market declines and capital slowdown. Long-term investors recognize the importance of enduring through market cycles, unlike newer entrants who might struggle with downturns. This cycle of high entry and low exit isn't a sustainable strategy in any market, underscoring the nuanced discussions we are engaged in today.

What’s On The Mind of Global LPs When talking Europe

The discussions have certainly evolved over cycles. Initially, the dialogue was about unveiling the potential I saw in Europe, which was then burgeoning. The narrative quickly shifted as growth became the headline in every tech publication—each year setting new records in capital infusion, deal counts, and other key performance indicators, culminating in a peak in 2021 with soaring valuations. The discourse clearly transitioned from justifying Europe's potential to strategizing around this growth.

However, with the latest market decline, slowing capital commitments, and ensuing write downs. Undoubtedly, the narrative has changed a bit with newer newer investors, unfamiliar with downturns who are grappling to comprehend and navigate this phase. Unfortunately, a trend of entering high and exiting low among some investors exemplifies a lack of market savvy, shaping a part of our current discussions.

However, with long-term investors, today's dialogue is richer, underscoring the necessity of investing through market cycles, as opposed to attempting market timing. Here, the focus is on discerning the enduring fundamentals amidst these market corrections, and deliberating on the investment thesis moving forward.

The Sustainability of The European Opportunity

A decade ago, the sustainability of the opportunity in Europe was a concern. However, the question of whether Europe could foster a robust and diverse range of self-sustaining activities is no longer a worry. The strong returns witnessed have not only galvanized Limited Partners (LPs) but have perhaps more significantly, ignited a spark among more founders.

This mirrors the well-documented 'PayPal Mafia' effect where successful exits lead founders to become repeat entrepreneurs, angel investors, or even venture capitalists, thereby fueling the venture capital flywheel. Ross's annual presentation effectively articulates this, reaffirming what we as investors already know. Investing in regions where capital is abundant and valuations are high often yields less favorable outcomes compared to regions with capital scarcity and lower valuations.

If your entry point is one third to one half, then you don't need the exit to be as big to develop a high multiple and that's what gets me excited to be investing today. Prices are prudent again. DD is prudent.

The higher returns in Europe don't possess a mystical quality; they are a simple function of lower entry points, which require less significant exits to achieve high multiples. This is the allure of investing today where valuations and due diligence are prudent.

However, the narrative of capital scarcity in Europe might be shifting with the entrance of notable venture capital firms like Andreessen Horowitz, alongside an established presence of others like Accel, Bessemer, and IVP. Their move hints at a changing landscape, yet the prudent valuations continue to make Europe an enticing market for investment.

European Capital Scarcity

If you ask a European who's lived in a system that's grown year on year, they say, “Gee, there's way too much capital here.” If you talk to an American, she’ll say “You guys don't have any capital over there. What are you doing? You need more growth funds.” But my point of view is that I believe capital is getting too prevalent when fundings are being done on a FOMO basis.

The perception of capital scarcity in Europe varies depending on whom you ask. Europeans, accustomed to a steadily growing system, often feel overwhelmed by the influx of capital, questioning its effective deployment. On the other hand, Americans might perceive a dire need for more growth funds in Europe.

I find the tipping point concerning when investments are driven by a Fear Of Missing Out (FOMO), characterized by competitive bidding in funding rounds. This isn't a healthy sign, but rather an indication of excess capital. A more measured approach, where funding discussions are tailored around achieving the next milestone within a 12 to 18-month growth plan, is a more prudent practice in my opinion.

Despite the influx, Europe hasn't mirrored the frenzied investment climate observed in the US. This isn’t to claim any superiority in the ecosystem, but perhaps a habitual prudence born from a historical capital scarcity. This scarcity has fostered an operational focus, especially in early-stage funding.

Indeed, many American funds have ventured across the Atlantic, though there seems to be a slight retreat recently, possibly due to the need to consolidate their core portfolios back home amidst market corrections. This cautious step back underscores a broader narrative of balancing expansionary zeal with prudent investment strategies.

If U.S. capital, especially at the growth stage, retracts, there are two dimensions to consider: the granular bottom-up aspect and the overarching systemic perspective. From a bottom-up standpoint, strong, well-received companies in Europe continue to secure funding despite a renewed emphasis on prudence in the investment realm.

When we have a great company in our portfolio that's growing strongly, that has a product customers love and it needs funding, it's getting funding.

The market still has a considerable amount of dry powder ready for worthy investments, alleviating concerns regarding funding availability for standout companies.

On the systemic front, various government reports suggest that the initial hurdles of seed and early-stage funding have been largely surmounted across Europe, with numerous funds providing that crucial initial capital. However, as these companies mature and seek further capital for growth, a potential bottleneck emerges. The discourse now leans towards cultivating local growth capital instead of relying on external heavyweights like Sequoia. While their participation is valued, the drive to retain promising deals within local or regional growth funds is gaining traction.

The Influx of Government Capital

If we simply put 0. 5 percent of European pension money into this market, done, problem solved.

The pathway to fostering a robust investment ecosystem in Europe hinges on patience and success, with a preference for minimal market intervention. While the artificial instigation of growth funds serves as a transient remedy, it's crucial to phase out such measures promptly to prevent distortion in the free market's operation.

While Joe hold reservations towards market tampering, the ongoing initiatives, many spearheaded by governments like BIF in Central Europe, BPI in France, and KFW in Germany, are commendable. These programs, now extending their focus to growth-stage funding through venture debt, growth capital, and fund investing, are stimulating the inception of new funds by stepping in as Limited Partners, much like their early-stage counterparts.

The crux of a thriving investment landscape lies in the organic development fostered by generating returns, which in turn attract institutional investors. A pivotal moment awaits when a significant portion of European pension funds are allocated to this market. As posited by Atomico in their State of European Tech reports, a mere allocation of 0.5% of European pension funds into this market could potentially resolve the funding gap.

The essence is not the absence of capital but the alignment of investor missions with visible, consistent returns over a substantial period, say 10 to 15 years. Joe favor a scenario where the market gradually matures and organically devises solutions, over one where artificial mechanisms are overly employed to expedite the process.

The Path to Unlocking European Pension Fund Money

There’s a really nice recent example in the UK where a group of pension funds have signed something called the mansion house compact, which is a kind of statement of intent and an explanation that, Hey, we are falling behind the best investors in the world in returns by not having more risk in the portfolio, done properly.

Pension funds across different countries need to grant themselves the autonomy to venture into private markets more actively. The narratives of pension fund investments vary from Germany to the UK and France, but a common thread is their underinvestment in private markets, encompassing not just venture and growth sectors, but buyouts and other realms too. This trend, albeit shifting gradually, still has room for acceleration. A recent initiative in the UK, the Mansion House Compact, signifies a collective intent among pension funds to embrace more risk to enhance returns, aligning with global best investment practices.

The onus is on pension managers to undertake a meticulous approach, armed with a well-thought-out strategy before delving into these markets. It's about fostering a long-term investment ethos rather than succumbing to boom-and-bust cycles prompted by sporadic interest.

It’s a big opportunity for Europe in general, but all those pension funds that haven't done this before, they need an entry point. Sometimes I say; We've met 1,400 VC firms so that you don't have to, and we’ve picked around 40 out of that group over time, and we're very happy to help you. We love it.

Fund-of-funds or co-investment platforms can act as pragmatic entry points, especially in evolving markets. These avenues provide a semblance of risk mitigation while acquainting investors with the market dynamics. Isomer Capital, for instance, serves as a stepping stone for many investors new to the European venture scene or even the venture sector altogether. By curating a diverse, resilient portfolio, they offer a learning curve for Limited Partners (LPs), allowing them to gauge the market, and subsequently, intensify their engagements based on preferences.

Sifting through a vast array of VC firms to cherry-pick a select few, requires true commitment to the space and often requires a guided entry into the market. It's about nurturing an understanding, fostering comfort, and eventually enabling more profound, informed engagements, which is a promising prospect for Europe and the broader investment community.

Tapping Into The European Opportunity

If you look at UiPath, there were three seed funds that did the very first round that made really outsized returns. And I'm pretty confident no one had heard of those funds at the time. Two of them are GPs of ours and the third one is also a great, great firm. So that's really what we're trying to do; Provide that first funding of those.

The European investment scene inherently necessitates a distinct approach compared to the U.S. due to the absence of a centralized hub akin to Silicon Valley. Though London stands as a significant hub, the European landscape is more fragmented with thriving hubs in Berlin, Paris, Stockholm, and beyond, each boasting a tapestry of unicorn companies. This geographic dispersion is both a treasure trove of diverse talent and innovation and a challenge in identifying and accessing potential high-growth opportunities, especially in less conspicuous regions like Romania.

This scenario steered Joe and his team towards a fund-of-funds strategy, not because it was strategizing around being a soft entry point for LPs but as a means to have a vantage point across the diverse European landscape. By investing in a meticulously curated assortment of funds, each with a local or sometimes sector-specific focus, they saw that they could extend their reach and enhance their likelihood of early engagement with promising ventures. The success story of UiPath, initially backed by lesser-known seed funds, two of which are Isomer GP partners, exemplifies this strategy.

Crafting a portfolio that encapsulates the breadth of Europe's innovation landscape, spread across 44 jurisdictions, is akin to assembling a complex puzzle. It demands a delicate balance between geographic and sectoral focus, achieved through a blend of investments in funds with local market dominance and those with a pan-European sectoral outlook. For instance, while a notable fund in Paris might have a comprehensive grasp of its local ecosystem, a broader European perspective is crucial, especially in sectors like enterprise software, to avoid blindsiding by neighboring innovations.

Isomer’s aim transcends merely spotting the 'next big thing'; it extends to nurturing these ventures through their growth trajectory, leveraging co-investments and secondaries. The anecdotal observation that local VCs often have a stronger foothold in pre-seed and seed stages in their respective regions, transitioning to a broader pan-European engagement in subsequent stages, underscores the nuanced dynamics of European venture investing. Through this multifaceted strategy, Isomer aspire to not just traverse but thrive amidst Europe's rich, yet complex innovation ecosystem.

Why Local Seed Funds Will Continue to Dominate Europe

Put yourself in the shoes of the founder. You're a founder, you're two guys in a garage, you're trying to build a beautiful piece of tech. You're not a funding expert. You don't know about the venture landscape. You're two guys in the garage. The first day you need some money, you stick your head out of that garage and who do you see? Well, it's for sure not the pan European fund located in a different country. It's the local tech people that you look up to. They may be angels. They may be exit founders themselves.

The assertion that local seed funds will continue to reign in Europe for the foreseeable future is rooted in the inherent benefits of proximity and nuanced understanding of local markets. Envisioning from a founder's perspective, the initial quest for funding is likely directed towards familiar local tech personas, be they angels or exit founders, rather than a distant pan-European fund. This localized support not only facilitates funding but also offers hands-on assistance in the early stages of product development, creating a nurturing environment for nascent tech ventures.

The narrative expands to the broader dynamics of European investment, underscoring the essentiality of local seed funding in fostering successful startups, as evidenced by the trajectory of companies like UiPath. The portfolio construction, thus, is envisioned as a meticulous endeavor, aiming to cover the breadth of Europe's innovation landscape, a task demanding a balanced blend of geographic and sectoral focus.

Global Ambitions in European Founders

The need of tapping into the U.S market is largely contingent on the sector in which a European tech company operates. As an example, enterprise software and consumer-focused ventures may need to take very different routes.

For enterprise software entities, the U.S market, being a hub for substantial customers and potential acquirers, beckons as a lucrative frontier necessitating a well-thought-out expansion strategy. Conversely, consumer-centric ventures, especially those attuned to the European consumer psyche, might find ample opportunity to thrive within the European market, rendering a U.S expansion less compelling.

Think of a comparison between DoorDash and Deliveroo. Deliveroo's discernment to eschew the fiercely competitive U.S market, in favor of less saturated markets in Asia and the Middle East, underscores the merit of a meticulously crafted geographic strategy in fostering a company's growth trajectory.

Another example is Fintech vs Gaming. FinTech ventures might find their services intricately tied to local regulations, making them less adaptable to the U.S market. On the flip side, the inherently global nature of gaming companies allows for a virtually borderless market reach right from inception.

Global Ambitions in European VCs

European VCs are modeling themselves on the best VCs in the world, not the best VCs locally. They've all studied the methods, they've seen the successes and understood the fund models deployed by the best, and that's what they're using. They're not iterating to a decent model. They're just studying the best and launching on that.

Today's European VCs are invigorated by the notable success witnessed in the field, fueling their ambition to emulate it. This, in turn, is nurturing a new generation of VCs who are shifting their mindset. They are now setting their sights beyond local paradigms, aspiring instead to mirror the world's leading VCs.

This shift traces back to the inception of Isomer, which was spurred by a collective endeavor among VCs in Europe to emulate the best. Joe saw them scrutinizing effective methodologies, and analyzing successful fund models employed by eminent VCs, aiming not just to iterate to a decent model, but to leapfrog to the best practices right from the get-go.

The Make Up of A European Top Fund

“If you don't have a nice model to get to 3X net as a baseline, there are easier ways to make money … [The best then] have one, two or three really big outliers driving a few to two X fund level returns and then often they have a good book as well.”

On what constitutes the 'best' in Europe, the benchmark Joe proposes is a 3X net return. If a VC can't achieve this baseline, there are indeed more straightforward avenues to financial gain. It's crucial to dissect a VC's model concerning the stage of investment, average entry price, ownership, reserve ratios, and realistic exit assumptions, rather than chasing the dream of housing eight unicorns in one's fund. The focus should hinge on demonstrating how average exits in Europe can be optimized to yield substantial returns. Interestingly, small funds are more often that most think, multiplying their value by five to 10 times, thereby far exceeding expectations.

The essence of a stellar strategy lies in a bottom-up approach. It begins with early-stage investments acquired at low prices, which holds the opportunity lead to the identification of a few unicorns, thereby elevating the fund's overall performance. The key is in not merely offering capital but elucidating why your fund is the preferable choice for founders. It's about showcasing the added value you bring to the table and how you plan to propel returns.

The most successful fund manager typically sow numerous seeds at low costs, embracing a diversified portfolio. Pinpointing a winner during the pre-seed or seed stages is a tall order, hence, a broad spectrum of investments is imperative as any one of them could skyrocket to success.

The most successful funds often have one to two standout outliers that significantly drive up the fund-level returns, frequently accompanied by a solid portfolio. Joe described in the episode how he has observed a few of these managers who possess an uncanny knack, right from the initial founder meeting. It's as if they have an intuitive sense, akin to a sommelier's nose, that detects something extraordinary. Though they might not pinpoint what it is, they're willing to place a modest bet.

Picking Outlier Managers

Indeed, finding true outliers is a challenging query. It would of course be ideal to witness a spectacular five-fund track record of such discernment, making the investment decision straightforward. There are a handful of such funds, and investing alongside them is always a pleasure. However, in Europe, it's often about analyzing an angel record or past successes in business.

Many have been founders themselves, naturally attracting a robust deal flow. The Isomer approach can be described as a comprehensive 360-degree due diligence. Engaging with individuals who have previously collaborated with these teams, be it past investors or coworkers, helps craft a clearer image of their pursuit and the likelihood of success.

Understanding their strategy and assessing their execution capability is an arduous task. Isomer aims to converse with a wide spectrum of individuals to identify the highest probability of success, especially when they back first or second funds. There's a blend of science and art involved – evaluating historical career achievements while also being drawn to the ambition, logical construct, and unique thesis presented.

Fund ones are particularly intriguing as they often outperform despite the conventional association with higher risk. When meeting someone establishing a new firm, it's evident that they've dedicated years to strategizing, a level of deliberation rarely seen in third or fourth funds. Fund ones and twos often exhibit an impressive aggregation of data and a well-refined thesis, often accompanied by prior deal preparations, offering a glimpse into potential portfolio successes.

However, there's no silver bullet. Underwriting such funds necessitates rigorous effort, reflecting a meticulous blend of analytical assessment and intuitive judgment.

The Secondaries Opportunity in Europe

As with anything, buyer beware … Whenever we look at a secondary, unlike secondaries in the private equity world, we don't really think about the discount. We think about “what could this company, or this basket of companies, exit at?” And if we discount that back by our target return, we get what we'd be willing to pay.

European unicorns hold promise, yet a subset of overvalued companies may falter, hence the timeless advice of 'buyer beware' holds true, especially when considering investment at the last round price. When evaluating a venture secondary, our focus shifts from the immediate discount to the potential exit valuation of the company or the collection of companies within the fund. By back-calculating from our target return, we derive the price we're willing to offer, only then comparing it to the current valuation. A deal materializes if the seller finds the discount agreeable; if not, we move on.

The landscape reveals a substantial liquidity need among Limited Partners (LPs), founders, and early investors, with some seeking exit from overvalued ventures. The influx of 'tourist investors' during 2019 and 2021, who retreated when the market dipped, has now created opportunities. Discerning investors can unearth valuable assets and strike beneficial deals with those unwilling or unable to remain invested. The accumulated assets over 12 years of NAV growth with minimal liquidity represent a sizable opportunity, even just if a couple percent trade, it’s potentially a three to 5 billion opportunity a year.

European vs US Venture performance

The revelation that the European venture market has outperformed the US market across three, five, 10, and 15 year intervals, as per Cambridge Associates fund returns benchmarks, often astonishes individuals, especially US Limited Partners (LPs). This surprising data contradicts conventional beliefs, as many US LPs had long dismissed Europe as a potential venture capital hub, focusing instead on domestic or sometimes Chinese markets. However, presenting this data has sparked a newfound curiosity towards the European market, indicating that disregarding Europe in one's venture growth allocation could be a significant oversight.

This shift in perspective is essential, as Europe presents a unique landscape with its own set of challenges and opportunities. One of the major concerns is the potential boom-bust cycle, reminiscent of the hype cycles of the 90s and 2000s, where overvaluation and overfunding led to sharp corrections, leaving investors wary and the ecosystem set back. The preference is for a prolonged, steady growth period, contrasting the US's sharper valuation curves that often lead to significant markdowns during downturns. A case in point is how some American LPs reported a 20-30% haircut in their venture book, while in Europe, the markdown was a more modest 5-8%. This discrepancy is attributed to a lesser hype cycle in Europe, fostering a healthier, gradual growth.

The advocated funding approach is to align investments with the operational needs of companies, veering away from the fear-driven overfunding spurred by capital abundance and FOMO (Fear Of Missing Out). This cautious, step-by-step growth strategy, grounded in hard work and prudent decision-making, is seen as the sustainable path forward, as opposed to the creation of massive funds infused with "dumb money."

Interestingly, the success and stability of the European ecosystem are becoming a magnet for talent. The region is not only being recognized for its venture potential but also as an attractive place to live. Anecdotal evidence suggests a trend of individuals from the US and other regions joining or founding startups in Europe. Furthermore, the lure of a better standard of living in certain European countries is drawing talent, both from within and outside the continent. Even within Europe, the migration of individuals seeking better living standards is noticeable.

Moreover, the burgeoning success of the ecosystem enables companies to pull expertise from traditional industries and big-name companies, a trend less conceivable 15-20 years ago. This pull is also extended to individuals who had migrated to the US for education or early career opportunities but are now returning to Europe to leverage the growing opportunities in the venture space.

The evolving narrative is contributing to a self-propelling cycle of success. As the ecosystem matures and success stories multiply, the attraction for talent intensifies, further enriching the ecosystem with the necessary expertise to propel companies into later stages of growth. This harmonious cycle, fueled by prudent growth strategies and the influx of talent, positions Europe as a significant player in the global venture landscape, challenging the previously held notions that had relegated it to the periphery of the venture capital world.

Advice to LPs and Allocators who are looking at Europe

It's imperative not to directly transpose a US VC strategy to Europe; instead, invest time in comprehending the distinct landscape, either through partnerships with firms like ISOMER or by engaging directly with the diverse, vibrant markets across various European cities—not just the well-trodden paths of London or Berlin.

The European venture scene reveals opportunities where less competitive capital leads to better pricing while still nurturing robust tech companies, promising attractive returns. For instance, initially, Spain might not have seemed a lucrative venture market, but upon closer examination, it has proven to offer remarkable investments and fund managers. It's about continuously reviewing and discovering the hidden gems scattered across Europe.

The excitement extends to Eastern Europe, showcasing a plethora of highly educated, ambitious individuals alongside a substantial technical foundation. Despite the scarcity of capital, the region holds promise for those willing to delve into its complexity. Similarly, the Nordic markets are acknowledged for their potential, with everyone on the lookout for the next big thing post-Spotify. France, albeit challenging for outsiders, holds gems like SoRare, provided one is integrated within the French ecosystem.

Switzerland, often overlooked, is a heavyweight in the crypto and web three spaces, with Ethereum having its roots there. Each market in Europe has its unique offerings, requiring a tailored approach, patience, and thorough exploration.

Venture Capital, though categorized as an 'alternative' investment, is seen not as an alternative but a pathway to drive real, life-altering innovation. The enthusiasm lies not in short-term conveniences like faster pizza delivery, but in leveraging technology to address global challenges like climate change. The optimistic outlook is that technology will unveil solutions yet unimagined, and venture capital can play a pivotal role in fostering innovations that not only solve real-world problems but also generate significant financial returns.

The investment in high-quality managers and companies tackling substantial issues, thus, goes beyond just monetary gains—it aligns with the broader vision of utilizing venture capital as a tool for meaningful, world-altering innovation. Through this lens, every market, every venture, and every investment is a step towards a better, technologically advanced, and solution-oriented future.

Upcoming events

📺 Virtual events we’re hosting

Data Driven Portfolio Modeling | Jan 17, 2024, 12:00 PM - 1:30 PM

🤝 In-person events we’re attending

Hit us up if you’re going, we’d love to connect!

GoWest | 📆 6 - 8 February | 🌍 Gothenburg

Super Venture | 📆 4 - 6 June | 🌍 Berlin

Nordic LP Forum & TechBBQ | 📆 September | 🌍 Copenhagen

North Star & GITEX Global | 📆 14 - 18 Oct | 🌍 Dubai

GITEX Europe 2025 | 📆 23 - 25 May 2025 | 🌍 Berlin