Pioneering Community Raises in European Venture

How to think about community raises, the pros and cons, the questions you should ask yourself.

By now, you’ve likely realized that we’re spearheading community raises with the VCs we believe are blazing the trail in Europe. So seeing Ryan Hoover’s recently published article on how to raise a fund in public, I of course had to add my 2 cents, as well as some thoughts on how we do it at eu.vc.

But first a caveat: obviously, the regulatory framework in Europe doesn’t allow you to raise in public as is the center of gravity in Ryan’s article. But that doesn’t mean you can’t run a community raise for investors that know what venture is about, but don’t have cash stockpiled for decade-long illiquid investments 💸.

First, let’s get the motivations right.

To not get rude, let’s explain this one in XKCD style:

I guess it’s pretty obvious why the above isn’t the way to go. Regulatory issues, ethical issues, division of work/exposure/gains issues, etc. Suffice it to say, if you’re thinking along those lines, no need to book a meeting with the bald guy. There are others happy to play like that, just do a Google search.

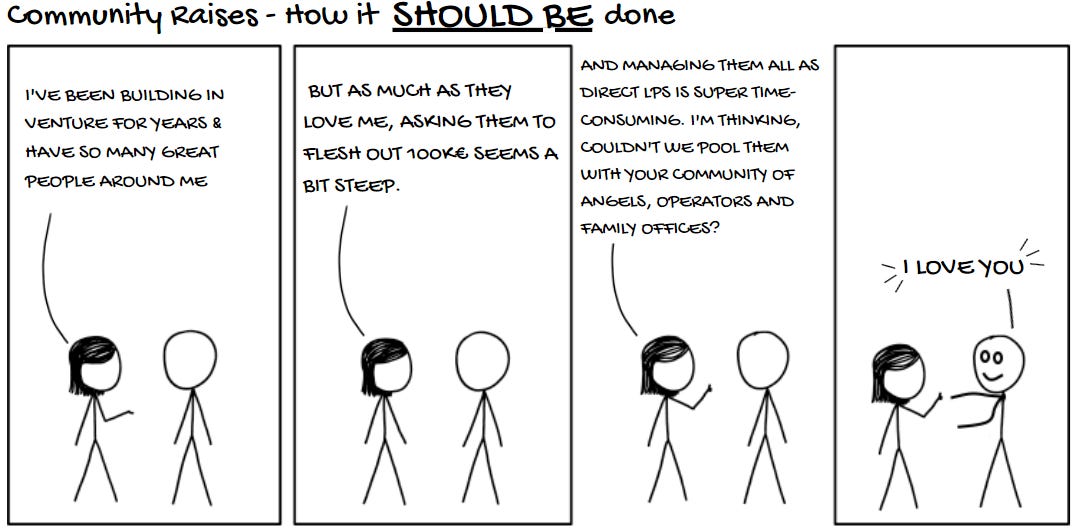

Instead, let’s turn to how we do it.

So why do we put it like this?

Firstly, there’s some regulatory considerations. If people don’t understand venture (shorthand for ‘being a sophisticated investor’) they most likely shouldn’t be investing in venture funds.

Secondly, what we’re on a mission to do is connect European Venture. Full stop. That means VCs, LPs and Angels. And founders, operators, execs, ecosystem champions, etc. in their capacity as angels. That’s who we talk to in our podcast, that’s who we talk to in our newsletter. That’s who we create our memes for.

Finally, we’re building communities. Not peddling capital. We’re getting kick-ass investors into vested communities to back the managers that blaze the trail in Europe. A sausage slinger from Blackpool won’t do much for you and you likely won’t be having long slack threads discussing deal flow or new market entry tactics with him. That’s the conversations we’re building our syndicate communities to foster.

That said, we’re of course pretty tight with some HNWs and FOs who we’re kicking tires and co-investing with. So guess there’s some cash-peddling going on as well after all 🤭.

The pro’s of community raises?

To expand the funds’ network

Venture is inherently relationship-driven. And having a small army of embedded operators, founders, and angels vested in your success can be a superpower for your firm.

We raised our latest fund from over 350 LPs. It’s been very helpful having some of the world’s most talented marketers, engineers, designers, salespeople, and founders financially invested in our, and the portfolio’s success. Our Community Raise was one of the best decisions we made.

Ryan Hoover, Weekend fund.

In our syndicates, we see portfolio founders and operators joining. We see angels from past and future deals joining. We see ecosystem champions from accelerators and incubators joining. All people, who with their investment embark on a decade-long vested relationship with the manager. All people who are incentivized to make introductions, help founders out, and diligence deals in the areas they know best.

Further, we’re proactively seeking to expand the GP’s network. We activate our own community of Angel LPs, which counts hundreds who have committed to back Europe’s trailblazers.

Diversify your LP base

By having a vehicle with lower minimum commits, investors from more diverse backgrounds can participate. The notorious 100k minimums are one of the worst blockers of democratizing access to the wealth creation of private market investing and busting open the asset class is a core motivation for us at EUVC.

For that reason, using our syndicate to increase the representation of minorities is front and center in our raises. We’re proud to say that we’ve recently closed a syndicate with >50% women LPs.

Become furniture

When we commit to a manager at EUVC, we commit more than just capital. We commit to helping that manager cement their brand and firm in the European ecosystem. A well-thought-out community raise and syndicate can help you build and sustain that more effectively. Make money with and for the right people and they’ll become your best ambassadors.

The Cons of community raises

Every LP will need to provide proof of accreditation

As you all know, this is the premise for investing in VC in Europe. Not much to say there, other than “wtf regulators? Delusional founders can take money from any bloke off the street into their startup, but a manager with a diversified portfolio, track record and who adheres to strict regulatory requirements can’t!?”

At least, just as the US have had great innovation happen on investor onboarding process, so have we in Europe with the likes of Odin, Vauban, Leva, Uniborn, and many more. That at least makes the process easier, but still. The requirements remain and the GP cannot lead or raise the vehicle themselves. Enter community syndicates such as ours 😊

It can be operationally heavy

For sure it is. No doubt about it. In the case of managers working with us, this is of course lightened considerably. But there’s still work and bringing on a community LP syndicate will never be without work – at least not if you want a curated value-add LP community out of it.

There’s always risk in taking on a bad partner

A bad partner can show him/herself in multiple ways: sharing confidential information, acting as less than an ambassador for the firm or having ridiculous demands causing unnecessary work.

The way we build our community raises, we’re the deal leads and the small-ticket investors are our LPs, not the GP’s. In other words, we’ll always be a buffer between the group and the fund manager, allowing us to ensure that the GP isn’t flooded by unfair demands. They’re our responsibility.

To protect against the sharing of confidential information we do multiple things: of course, we vet investors and make sure they understand and sign our community LP pledge, our NDA, and that the information shared to the syndicate is redacted of information that should not be shared in the market. Especially information on portfolio startups is subject to such redactions. Though larger investors that we work closely with may of course hold preferential positions.

This said about the pros and cons, let’s turn to the how.

How to run a community raise

If you’re thinking about running a community raise, there are some things to consider. Here are the high-level questions we always encourage VCs to consider before embarking on this journey.

What are you looking to achieve? Is it just to access capital or about building community? Are you doing it to democratize access to your fund? Where are you looking to build brand - with retail investors or tech investors, if at all?

What’s the allocation size and what can you realistically raise? If you’re a highly coveted manager whose fund has filled out in mere months, expect a similar dynamic for the community raise. If you’re not, it’d be surprising if lowering the minimum ticket would make you so. To be perfectly honest, we always say that if you’re not an established big brand VC, you should expect the raise to be anchored by your established community, meaning people who know and respect you and for that reason want to vest their own success with you.

What’s your commitment to the raise? Raising from a larger group of individuals is always easier when you’re a known entity with a strong brand and market communication. In other words, what’s your content pipeline and media strategy?

What’s your fundraise timeline? And where would the community raise fit and how long should it ideally be? You should make sure this is done at a time when it doesn’t hurt your main raise.

What’s the profile of investors you’re looking for? If you’re looking to build a community with value-add investors, you shouldn’t take this question lightly - if you do, it’s probably because it’s more about the money and branding than actual community building. Which is fair! Just be straight about it.

Who do you wanna partner with? As said, there are multiple players around, some big and known, others less so. Aside from checking them against your answers to the above, we also urge you to consider who you trust. As an example, we know of a case where the deal lead set up a structure where the LPs’ returns unnecessarily (and worse, unknowingly!) will be severely impacted by taxation (of up to above 50%!). You don’t want to be associated with that.

One of the points at which we’re a bit different most is our commitment to building value-adding communities. In fact, we’ve made it a litmus test that the capital shouldn’t be the main driver, but rather the value-adding community should. With us, the capital only acts as a mechanism to align interests and ensure long-term commitment on both sides.

Aside from this, we’re probably also different from most in that we commit the EUVC content and events machine to work for the managers we back. We wanna be the hypeman in their corner. Hopefully, this can help them build momentum and interest with LPs that maybe otherwise hadn’t noticed them. In fact, only a few weeks ago a past guest on the EUVC pod asked us if we could change a fact in an old episode with him that had become outdated, as he had needed to correct it to multiple LPs during their raise. So yes, it seems our episodes do reach the ears of the right people.

How will you engage the community? Once the investment is done, you’ve just brought on a new type of LP that wants to engage with you, but you’ll need to take the initiative (together with the lead of the community syndicate). Given our investors’ profiles, we only work with partners that are ambitious in this respect.

Think a community raise is for you?

Don’t hesitate to reach out - but expect us to be thinking whether you fit into the first or second cartoon 🙏