Conviction, Consolidation, and Smart Capital

LP pressure, climate’s next phase, and what founder-first capital really means — plus the last chance to nominate for the EUVC Awards

Hi friends 👋

Before we dive into this week’s edition, a quick but important note.

A huge thank you to everyone who has already submitted nominations for the EUVC Awards. It’s encouraging to see the ecosystem engage so thoughtfully. If you haven’t submitted yours yet, there’s still time. Nominations close on March 6.

Today we’re spotlighting two categories that reflect where European venture is maturing: CVC of the Year and Exit of the Year.

Now, let’s turn to this week’s podcast episodes.

We start with Max Bray and Juliet Bailin, both Venture Partners at Kindred Capital, on the real state of LP conviction: why even strong first-time funds are struggling, why the “middle” is getting squeezed, and how the venture model is splitting into a barbell of extremes.

We then shift to climate’s next phase with Lubomila Jordanova, co-founder and CEO of Plan A, in a conversation recorded just weeks after Plan A’s acquisition, together with Carmel Rafaeli, Founding Partner of The Table. It’s a refreshingly honest conversation about how climate software is being stress-tested by regulation, buyer complexity, and the messy dynamics of the real economy and why consolidation is emerging as a strategy, not a failure.

Finally, we step into what “smart capital” looks like when it’s anchored in a real ecosystem with Andy Lurling, founder and GP of Lumo Labs. We go deep on why Eindhoven still matters, how Lumo built a focused digital deep-tech thesis around health and cities, and how they operationalise founder support rather than improvising it.

As always, thank you for reading, sharing, and pushing the conversation forward. It genuinely makes this community stronger.

Hope you enjoy,

with 💖

David & Andreas

Virtual | Wednesday, March 4 | 02:00 PM - 04:00 PM GMT

If you’re building or managing a venture fund, your returns are shaped long before the exits happen. In this advanced 2-hour online masterclass, you’ll sharpen your ability to design, stress-test, and optimise your portfolio through better construction and decomposition.

You’ll learn how to structure entry and follow-on strategies, track capital deployment over time, simulate write-offs and exits, and model key performance metrics like TVPI, DPI, RVPI, and NAV with greater precision. We’ll focus on practical decision-making, real-world trade-offs, and dynamic asset valuation—so you can assess whether your strategy is truly set up to deliver.

Ideal for emerging fund managers, established VCs, family office and CVC professionals, and active HNIs who want to strengthen their fund modelling and make more informed portfolio decisions.

Table of Contents

The EUVC Awards

Insights of the Week

Podcasts of The Week

Max Bray and Juliet Bailin, Kindred Capital: LP Conviction, $15B Funds & The Venture Barbell

Andy Lürling: Lumo Labs, Smart Capital from Eindhoven, and Investing in AI for Health + Cities

Serving Europe’s Builders with Live Announcements

Events and Community Gatherings

The EUVC Awards: Nominations Are Still Open

As European venture continues to mature, expand, and professionalise, the way we recognise excellence must evolve with it. Today, venture in Europe operates at a greater scale, with deeper institutional participation and a stronger sense of shared responsibility for the ecosystem we are collectively building.

The EUVC Awards are designed to reflect that reality.

They recognise outstanding venture capital firms, investors, and ecosystem contributions across Europe. But recognition only carries weight when it is grounded in fairness, credibility, and context. Excellence cannot be assessed in isolation from scale, mandate, strategy, or responsibility.

For 2026, we have introduced deliberate refinements to ensure the awards remain aligned with the structure and substance of European venture today.

A huge thank you to everyone who has already submitted nominations for the EUVC Awards. It’s encouraging to see the ecosystem leaning in early and thoughtfully.

Today, we’re spotlightling two categories that reflect where European venture is maturing: CVC of the Year and Exit of the Year — recognising the growing role of corporate venture and the importance of durable, well-executed liquidity events in strengthening the ecosystem.

Help define what excellence in European venture truly looks like. If you haven’t submitted your nominations yet, there’s still time. Nominations close on March 6.

The EUVC Awards: CVC of the Year

Presented in partnership with CMS

Over the past year, we’ve doubled down on the corporate and CVC space — featuring some of Europe’s most active and forward-thinking CVCs, including Fidelity, Emerald, BMW, TDK Ventures and more. We also brought the community together at the EUVC Corporate Summit, creating a dedicated forum for dialogue between corporates, founders, and VCs.

Why? Because the average CVC lasts just 3.7 years — not due to lack of capital, but weak governance, unclear mandates, limited C-suite alignment, and poor ecosystem integration. Yet when done right, CVC can be one of Europe’s most powerful innovation engines.

To build momentum behind this work, we’re introducing the EUVC Award for CVC of the Year — recognising a corporate venture team that combines strong investment performance with real ecosystem contribution. We assess consistency, governance, founder engagement, co-investor collaboration, and long-term strategic value — not just capital deployed.

This is the first year the EUVC Awards include a dedicated CVC category, judged by our panel including Jeppe Høier, Corporate Venture Capital expert and co-founder of EUVC Corporate.

At their best, CVCs don’t just invest — they endure.

Nominations are still open. Submit your CVC of the Year candidate.

The EUVC Awards: Exit of the Year

In venture, headlines often celebrate the biggest exit. But size alone does not define success. What truly strengthens the European venture ecosystem is value creation, when a firm backs a company that not only exits, but delivers exceptional returns to its investors and recycles meaningful capital back into the market.

This award recognises exactly that.

We honour the firm that has generated the greatest value back to its fund and, by extension, to LPs and the broader European innovation economy through a standout portfolio company exit. It is a celebration of venture capital at its best: disciplined entry, hands-on value creation, and a strategically executed exit that maximises returns.

Importantly, this is not about headline valuation alone. It is about venture outcomes. It is about timing the market with conviction. It is about choosing the right exit path, whether IPO, strategic acquisition, or secondary transaction, and executing in a way that compounds value. It is about turning years of company-building into realised performance.

Past winners exemplify this approach.

2024 — SV Health Investors for EyeBio, demonstrating the power of deep sector expertise paired with precise strategic timing.

2023 — Capnamic for LeanIX, showcasing how conviction-led backing and thoughtful scaling can translate into outstanding returns at exit.

In recognising this year’s recipient, we celebrate more than a transaction. We celebrate the firms that close the loop, transforming ambition into realised returns and ensuring that capital flows back into Europe’s next generation of founders.

Insights of the Week

Fund Modelling in VC: Assumptions Sheet Construction

This masterclass centres on the assumptions sheet — the structural backbone of any VC fund model. It examines how strategy, portfolio construction and valuation dynamics converge at the input level, and how small shifts in core assumptions can materially reshape outcomes. It reframes the assumptions tab not as a static input page, but as the causal engine of the model, where sensitivity and judgement matter more than cosmetic complexity.

By learning to construct and stress test structural assumptions, you develop a clearer understanding of how asset development paths, ownership, dilution and valuation shifts cascade through return distributions. Led by Marc Penkala (āltitude) and our very own David Cruz e Silva, the session strengthens the analytical discipline required to build, evaluate and challenge a VC fund model with confidence.

Citrini’s Doomsday memo is flawed - This is the future I want to live in

In his recent piece “Citrini’s Doomsday memo is flawed,” Gregory Dewerpe, Founder and Managing Partner at noa critically challenges a viral memo from Citrini that warned of AI-triggered economic collapse and mass unemployment by 2028. Dewerpe argues the memo is built on two fundamental mistakes: it assumes demand is fixed and that AI simply replaces human labor. Drawing on economic history, he shows that falling costs from technological breakthroughs typically unleash latent demand and create entirely new categories of work, rather than shrinking the economy. Instead of a doomsday scenario, he advocates for a future where AI-driven abundance expands opportunity, boosts purchasing power, and fuels innovation across sectors.

Venture in Eastern Europe Report 2025

How to Web have published their Venture in Eastern Europe 2025 flagship annual research report, delivering a comprehensive analysis of venture capital activity across the region. Built on structured data and rigorous market analysis, the report maps capital flows, stage distribution, sector performance, and cross-border investment trends to illuminate how Eastern Europe’s startup ecosystem is evolving. Designed for investors, founders, LPs, corporates, and policymakers alike, it translates raw funding data into actionable insights on market maturity, capital concentration, and emerging structural shifts.

Podcasts of the Week

Max Bray and Juliet Bailin, Kindred Capital: LP Conviction, $15B Funds & The Venture Barbell

What exactly are LPs buying when they allocate to venture today and do they still believe in it?

In this episode, Andreas sits down with Max Bray and Juliet Bailin, both Venture Partners at Kindred Capital, to unpack what’s really happening beneath the fundraising headlines.

Max shares the raw reality of trying to raise a first-time fund in 2025 — strong unicorn-founder GPs, credible angel track records, and still struggling to secure second meetings.

Juliet offers the counterweight: LP frustration isn’t always ignorance. Sometimes it’s a rational response to how venture has been practiced — especially around transparency, liquidity discipline, and the unrealistic expectation that a GP should be world-class at everything.

This is not doom. It’s mechanics.

Key takeaways from the episode:

▪️ Early-stage venture looks structurally unattractive in uncertain cycles.

In volatile macro conditions, venture appears as the longest-duration, least liquid, hardest-to-underwrite asset class. Many LPs — particularly non-dedicated ones — rotate toward liquidity: public markets, bonds, secondaries, later-stage. Not because venture “doesn’t work,” but because patience is unevenly distributed.

▪️ Even strong first-time funds are struggling.

Unicorn operators. Angel track records. Clear positioning. Still no second call. The fundraising bar isn’t just high — it’s selective in new ways.

▪️ LP frustration is sometimes rational.

Two recurring friction points:

– Transparency: How are deals really sourced? How is pricing conviction built? How does portfolio construction evolve?

– Liquidity discipline: Are reserves managed intentionally? Is DPI a strategic goal? Or is the fund riding hype cycles?

Execution variance across GPs is wider than many admit.

▪️ LPACs should be sparring partners, not governance theatre.

The best LP–GP relationships are candid and iterative. Not ceremonial.

▪️ Europe’s structural gap: few have lived full cycles.

Compared to the US, fewer LPs and GPs in Europe have experienced multiple complete venture cycles. Pattern recognition is thinner. That matters in downturns.

▪️ Solo GP economics are brutal.

On smaller funds, 2/20 rarely works cleanly. After legal, admin, compliance, travel, portfolio support, and GP commit — there’s not much margin. Many solo GPs are effectively underwriting personal risk in exchange for carry. The romance of the model obscures the structural pressure.

▪️ Founders are asking a sharper question: “Why you?”

Not vibes. Not logos. Not generic value-add. A credible reason why partnering with this fund increases the probability of success.

▪️ AI is compressing software defensibility — maybe.

If software is easier to build, do we see smaller outcomes and fewer unicorns? Or does AI accelerate centralisation through distribution, data, and category leadership? The power law may persist even if the mechanics shift.

▪️ Alternative capital models are rising quietly.

AI roll-ups. Search-style structures. Blended debt–equity. Capital models tailored to asset-heavy or cash-flowing businesses. Venture was broadly applied over the last decade. The next may be about capital precision.

▪️ The middle-market squeeze: selection, not collapse.

This isn’t venture dying. It’s tolerance for fuzzy positioning disappearing. LPs want clarity on outcomes. Founders want the probability of success. Funds without sharp identity feel the pressure first.

🎧 Listen on Apple or Spotify, with chapters ready to explore.

Lubomila Jordanova, Plan A: Climate Isn’t “Over”

Climate isn’t “over.” But building in climate has entered a new chapter, defined by shifting regulation, politicized narratives, buyer confusion, and a market that funded dozens of overlapping platforms.

In this episode, Andreas and co-host Carmel Rafaeli, Founding Partner, The Table talks with Lubomila Jordanova, Co-founder & CEO of Plan A, just weeks after Plan A joined forces with Diginex, the NASDAQ-listed sustainability technology company, at the end of 2025.

The conversation is part of Leaders Shaping a Resilient Planet, a series spotlighting exceptional founders in climate tech who happen to be women. The focus is not identity as a theme, but execution as a discipline. These are operators building in some of the most complex and capital-intensive parts of the real economy.

This is not an acquisition recap. It is a clear-eyed discussion about what it takes to build and responsibly exit a climate tech company in a market that is maturing quickly.

Key takeaways from the episode:

▪️ Climate capital is still unevenly distributed.

Andreas opens with a stark framing: women-led climate startups continue to receive a disproportionately small share of venture funding. The structural imbalance in capital allocation remains real — even as urgency around climate grows.

▪️ What The Table is building.

Carmel outlines The Table’s model — a 370+ investor co-investing community focused on women-led climate ventures (pre-Seed to Series A), plus an evergreen Foundation providing recoverable grants alongside equity. Catalytic capital, not charity.

▪️ Plan A chose to lead consolidation.

Lubomila’s framing is pragmatic: the category was heading toward consolidation. Better to initiate and shape it than risk becoming the laggard reacting to it.

▪️ Regulation whiplash reshaped the landscape.

Rollbacks, shifting ESG rules, politicisation, and enterprise buyer complexity made scale harder — and made strategic combination more logical.

▪️ Fundraising logic evolves into acquisition logic.

With over 20 shareholders, complex governance, and growing enterprise demands, the question became: what structure best preserves growth and mission?

▪️ Founder outcome vs VC outcome isn’t binary.

Lubomila pushes back on the “10x or bust” narrative. The acquisition allows investors to roll into a NASDAQ-listed parent, retain upside, and operate with public-market transparency.

▪️ Climate gets mis-measured with SaaS KPIs.

Carbon accounting and decarbonisation sit inside supply chains, logistics, packaging, and enterprise planning. They are not pure SaaS abstractions.

▪️ The uncomfortable truth: some climate software is consulting with a digital layer.

Lubomila contrasts Plan A’s ~80% gross profit and multi-year enterprise contracts with heavily funded peers operating at 30–40% margins and heavy account staffing.

▪️ Unit economics matter more than category hype.

Investors bundled “climate” into one allocation bucket — but carbon removal hardware ≠ ESG reporting ≠ enterprise decarbonisation workflows. Return expectations should match domain realities.

▪️ Climate shouldn’t be one allocation bucket.

Segmentation is critical. Different sub-sectors require different capital stacks, time horizons, and return narratives.

▪️ Investor perception is a founder tax.

Visibility can create bias. Lubomila describes being misread as an “influencer founder” despite technical depth and operational performance.

▪️ Boardrooms bring baggage.

Each investor carries pattern-matching from other portfolios and cycles — often misaligned with the company’s actual operating context.

▪️ VC doesn’t operate in isolation.

Public markets, private equity, and macro capital flows ultimately determine what’s “bankable.” Venture enthusiasm alone doesn’t sustain categories.

▪️ Public-company KPIs change the conversation.

Post-acquisition, performance metrics become sharper, more standardised, and more visible — reframing how climate software is judged.

▪️ Three founder principles:

– Humility: someone will always be better funded. Focus on customers and team.

– Ecosystem over ego: durable outcomes require community.

– Real-economy problems are big enough: you don’t need sci-fi narratives.

▪️ Motherhood during the exit.

In a rare moment of operational honesty, Lubomila shares she was pregnant during the transaction. The takeaway isn’t just symbolic but structural: support systems and community make execution possible when life doesn’t pause.

🎧 Listen on Apple or Spotify, with chapters ready to explore, and stay tuned for future episodes of Leaders Shaping a Resilient Planet as we continue conversations with the builders shaping a more resilient world.

Andy Lürling: Lumo Labs, Smart Capital from Eindhoven, and Investing in AI for Health + Cities

In this episode, we sit down with Andy Lurling, founder and GP of Lumo Labs, to unpack what it actually means to build a focused early-stage fund in a market where “AI” can mean almost anything.

Lumo Labs is unusually specific: digital deep tech, deployed early, anchored in Eindhoven — home of Philips’ industrial legacy and the High Tech Campus often called the “smartest square kilometer in Europe.”

Andy is an entrepreneur-turned-investor who built and exited his own deep-tech company (first backed by the European Space Agency), before being pulled into fund formation by two cornerstone ecosystem players. What emerged wasn’t just another early-stage fund, but a thesis built around real-world constraints: health systems under pressure, cities generating most emissions, and software-first deep tech that can scale without heavy hardware drag.

This is a conversation about selection discipline, ecosystem leverage, and why early-stage support needs to be structured — not improvised.

Key takeaways from the episode:

▪️ Why Eindhoven matters: Lumo isn’t just “based in” Eindhoven — it’s shaped by it. Philips’ R&D DNA, deep engineering culture, and the High Tech Campus ecosystem create dense, early-stage digital deep-tech deal flow.

▪️ From founder to fund: Andy built EyeOpener, combining satellite navigation + gyroscope data to track high-speed objects, with ESA as first investor. Building through the financial crisis shaped his capital discipline — and his bias toward resilience.

▪️ The fund emerged from the ecosystem: Lumo didn’t start with “let’s raise a fund.” Two anchors — the High Tech Campus owner and the Brabant Development Agency — effectively pulled the team into formal fund management.

▪️ Fund I → Fund II progression:

Fund I: €20M, 23 pre-seed/seed investments.

Fund II: €40M+ raised so far, targeting €100m final close.

▪️ Digital deep tech, not hardware-heavy: Lumo is software-first. They can tolerate hardware components, but avoid hardware development and inventory risk. The preference is hardware-agnostic platforms that scale across ecosystems.

▪️ AI + one: AI is the base layer. Core categories include:

– Digital security / cryptology

– IoT infrastructure

– AR (“display of the future”)

Typically it’s AI combined with one of these deep-tech wedges.

▪️ SDGs as a forcing function, not marketing: Lumo adopted UN SDGs early (2016/17) to constrain focus. Over time, they centred on:

– Good health & wellbeing (largest allocation)

– Sustainable cities & communities

– Climate action (urban-focused)

– Quality education (smallest bucket)

▪️ Urban climate as the “source problem”: Instead of broad climate generalism, they focus on cities — where emissions, pollution, water, mobility, and infrastructure pressures converge.

▪️ Health thesis: cure → prevention: Rising healthcare costs + workforce shortages mean systems must move upstream. Earlier diagnosis reduces intensity, recovery time, and systemic burden.

▪️ Smart capital is operationalised: Lumo runs a structured founder-support program across four pillars:

– Leadership development

– Product–market fit

– Storytelling & marketing (especially for technical founders)

– Follow-on readiness (Series A preparation)

▪️ Monthly digital check-ins: Rather than relying on gut feel, they systematise founder engagement with short recurring data-driven updates.

▪️ Geographic focus with extensions: Core: Netherlands, Belgium, Germany.

Extended reach: Spain, Portugal, Nordics via scout presence.

▪️ Portfolio reality: 30 companies total; 3 closed; 9 (soon 11) progressing toward scale-up stage — a disciplined early-stage mortality rate.

🎧 Listen on Apple Podcasts or Spotify, or queue it up with chapter markers ready to go.

Serving Europe’s Builders with Live Announcements

Biorce’s $52M Series A and the Race to Cut Clinical Trials in Half

Clinical trials take, on average, 12 years and billions in capital before a drug reaches a pharmacy shelf. Could that timeline be cut in half?

In this episode, Andreas sits down with Pedro Coelho, founder & CEO of Biorce, fresh off closing a $52M Series A led by DST, with long-time backer Norrsken continuing its support.

Biorce is building what Pedro calls a clinical trial operating system — an AI-driven platform that helps pharmaceutical and biotech companies design, generate, and execute trials in one integrated system.

One example:

100+ page trial protocols that once took three months to draft can now be generated in 90 seconds at ~86% accuracy.

The ambition is bold:

reduce development timelines from 12 years to 6

cut development costs by roughly 50%

eventually enable a “one-click clinical trial”

But this story isn’t just about AI infrastructure. It starts with Pedro’s father being diagnosed with melanoma. A clinical trial extended his life by ten months. After his father passed away, Pedro sold his previous company and turned fully toward rebuilding the system.

This conversation goes beyond product:

building pre-AI vs building in the AI era

why Biorce built its own internal CRM

hiring “mini CEOs” for high-velocity phases

conviction as motion — not analysis paralysis

moving to Austin to build a second A-team

TAM vs TAP — and why platforms reshape markets

Pedro describes Biorce as a bullet train moving at 1,000 miles per hour. Walls appear. You either break through or adjust course. But you don’t slow down to map every obstacle in advance.

The $52M round isn’t the finish line. It’s fuel.

Fuel to expand into the US. Fuel to double down on AI research. Fuel to compress one of the most expensive and time-consuming systems in modern healthcare.

Biorce isn’t just optimising clinical trials.

It’s trying to rebuild the lifecycle entirely.

Incard’s £10M Series A and Why Fintech Isn’t “Done”

Europe’s banking stack wasn’t built for high-growth digital operators.

Not for D2C brands spending six figures a month on Meta.

Not for agencies juggling multiple revenue streams.

And not for founders who want real-time clarity without stitching together six tools and burning a weekend on reconciliation.

In this episode, Andreas sits down with Theo Cesarini, CEO & co-founder of Incard, and Thomas Depuydt, Managing Partner at Smartfin — lead investor in Incard’s recent £10M Series A — to unpack the thesis behind building a financial operating system for modern entrepreneurs.

The UK-based fintech is betting that the future isn’t another neobank. It’s a customisable orchestration layer combining banking infrastructure, payments, and an App Store of vertical-specific modules.

For Smartfin, the conviction came down to three things: market timing, defensible architecture, and execution velocity. In a crowded fintech landscape, Incard’s wedge is depth — not just issuing cards, but embedding itself into how digital-native businesses actually operate.

For founders, the impact is tangible:

cashback economics that matter at scale

real-time spend visibility

consolidation across accounts

automation that turns finance from admin into advantage

Theo calls it “the Marty Supreme of banking” built for GenZ founders, lean teams, and operators who don’t want finance to slow them down.

And perhaps most tellingly: they won’t freeze your account when volume spikes.

This is a conversation about fintech’s next chapter and why crowded markets can still produce large winners, how AI reshapes org design, and why the next generation of financial tools will look less like a bank… and more like a platform.

Sahil Patwa, Tenet: AI Rollups, Empathy-Driven Transformation, and Why Buying SMEs May Beat Selling SaaS

SMEs make up the backbone of Europe’s economy, but most of them still run like it’s 2005.

In this episode, Andreas sits down with Sahil Patwa, General Partner at Tenet, Europe’s first inception-stage investment firm dedicated to AI-powered rollups. Tenet launched last week — and already made its first investment.

Tenet’s thesis is simple:

AI can already automate close to 50% of knowledge work.

Now apply that to white-collar service businesses — firms that are low-margin, slow to scale, and heavily dependent on human labor.

The result is a new model:

Acquire service businesses

Build an AI-native operating layer

Automate 50–60% of core work

Expand capacity 3–4x

Move margins from ~5–10% toward ~30–40%

Scale through M&A and, eventually, organic growth

Sahil calls it AI Pro — AI-powered rollups and he draws a clear line between this and search funds: search funds buy businesses and run them slightly better. AI rollups buy businesses and transform the underlying economics.

That requires capital not just for acquisitions, but for:

building proprietary technology platforms

driving change management

integrating operations across rollups

In the SaaS world, adoption fails because people have to behave differently. In the AI world, if designed well, the system can behave differently — while people stay the same.

Tenet’s first investment is Tax Force, a rollup strategy in German tax advisory. Tax is not sexy, but it is structurally broken.

In Germany:

it takes ~7–8 years to qualify as a tax advisor

the industry faces severe talent shortages

many firms actively refuse new clients

Sahil believes 50–70% of tax advisory work is automatable with today’s AI

If AI can remove the admin-heavy core work, advisors can spend time on relationships, judgment, and high-value advice — while serving far more clients.

This conversation goes beyond the Tenet launch:

why AI rollups may outperform SaaS in SMB markets

what the “inception-stage” rollup founder profile looks like

why M&A skill matters — but is learnable

the operational reality of integrating messy, human businesses

why some rollups may scale like VC companies, not PE assets

Tenet is betting that Europe’s next decade-defining companies won’t just be software startups.

They’ll be industry rebuilds powered by AI, scaled through acquisition, and executed by founders who can do both product and people.

AI rollups aren’t about buying sleepy businesses. They’re about turning them into platforms.

This Week in European Tech with Dan, Mads and Lomax

In this episode of Upside, Dan Bowyer, Mads Jensen of SuperSeed and Lomax Ward of Outsized Ventures unpack a week that didn’t feel like a normal news cycle — it felt like three systems colliding at once.

Nvidia delivers another blowout quarter and the market barely reacts. Ukraine, four years into war, is quietly evolving from aid recipient to Europe’s most important live defence innovation lab. And AI safety — once framed as a moral north star — is being repriced in real time by geopolitics, procurement pressure, and competitive escalation.

This isn’t just tech volatility.

It’s capital, sovereignty, margins, and deterrence all moving simultaneously.

Key takeaways from the episode:

▪️ Nvidia is still executing flawlessly — but perfection is now priced in. Fourteen-plus consecutive beats reset expectations. The debate shifts from “how strong?” to “how sustainable?” Inference mix, custom silicon creep, and 70%+ margins become the real questions.

▪️ The shovel seller looks strong. The ecosystem beneath it is less certain. If foundation model economics remain structurally lower margin than expected, the entire AI infra stack gets re-rated upstream.

▪️ Ukraine has become a 21st-century defence R&D engine. Rapid drone iteration, software-defined battlefields, weekly countermeasure cycles. This is high-frequency innovation under existential pressure — and much of that capability won’t disappear post-war.

▪️ Europe’s defence budgets are rising. But announcements aren’t markets. The breakout signal will be large, repeatable multi-year contracts for venture-backed suppliers — not another NATO memo.

▪️ AI safety is no longer absolute — it’s conditional. When leading labs signal they won’t slow down unless clearly ahead, ethics becomes context-sensitive. Competitive pressure hardens incentives faster than policy can stabilise them.

▪️ Distillation at scale turns IP into geopolitics. If frontier intelligence can be harvested cheaply by strategic competitors, model training becomes a national security issue — not just a corporate one.

▪️ SaaS isn’t dead — it’s being redefined. SaaS as system of record. AI as system of action. The value layer persists, but pricing, integration depth, and data moats determine who survives.

▪️ Foundation model margins are the hidden constraint. Hypergrowth with compressed gross margins forces uncomfortable math. Growth-first narratives eventually collide with capital market discipline.

▪️ Europe’s deep tech wedge is real — chips and quantum are credible strengths. The bottleneck isn’t science. It’s long-duration scale capital, retention, and resisting US listing gravity.

▪️ The “abundant intelligence” scenario isn’t science fiction — it’s credit risk. If intelligence becomes cheap and pervasive, labour pricing, enterprise software value, and even financial system assumptions get stress-tested.

🎧 Listen on Apple Podcasts or Spotify — and if you’re building in defence, AI, chips, or deep tech, this one’s worth queueing with chapter markers.

Events and Community Gatherings

Join The EUVC Summit 2026 | 22/04/2026, London

Europe’s builders take the stage.

The EUVC Summit returns with founders, operators, VCs, and LPs focused on one question: how Europe wins.

From what it really takes to build category-defining companies in Europe, to how capital, conviction, and long-term alignment must evolve to compete globally — this is a working room, not a trends conference.

More details coming soon.

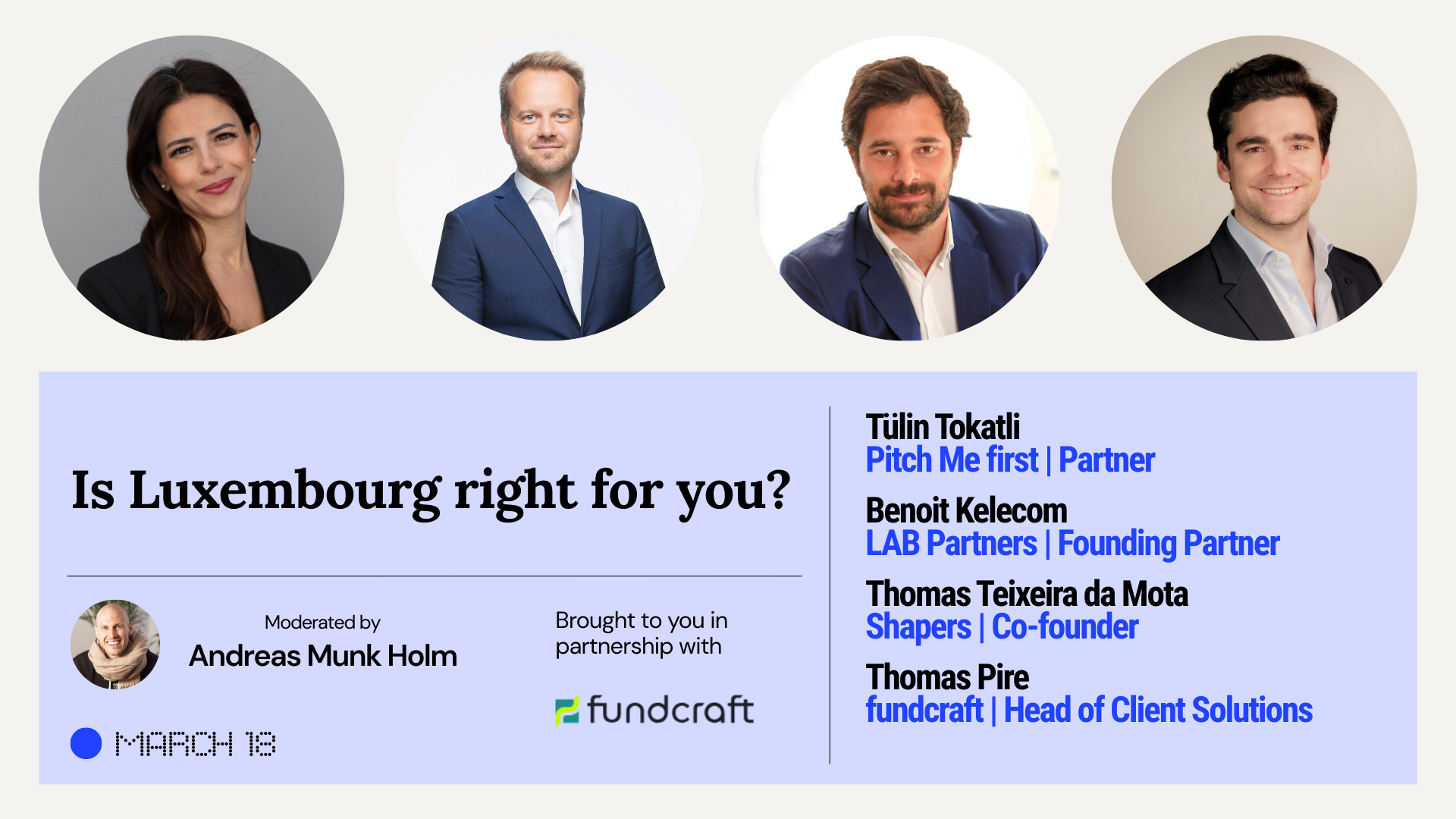

[Webinar] Is Luxembourg right for you? | 18 March, 12-1PM CET, Online

Brought to you in partnership with Fundcraft, join leading fund managers and operators for a candid discussion on whether Luxembourg is the right jurisdiction for your fund. Our expert panel will break down the practical realities—from structuring and regulation to operations and scaling—to help you understand when Luxembourg makes sense and when it doesn’t. Expect real-world insights, clear trade-offs, and actionable takeaways for emerging and established fund managers alike.

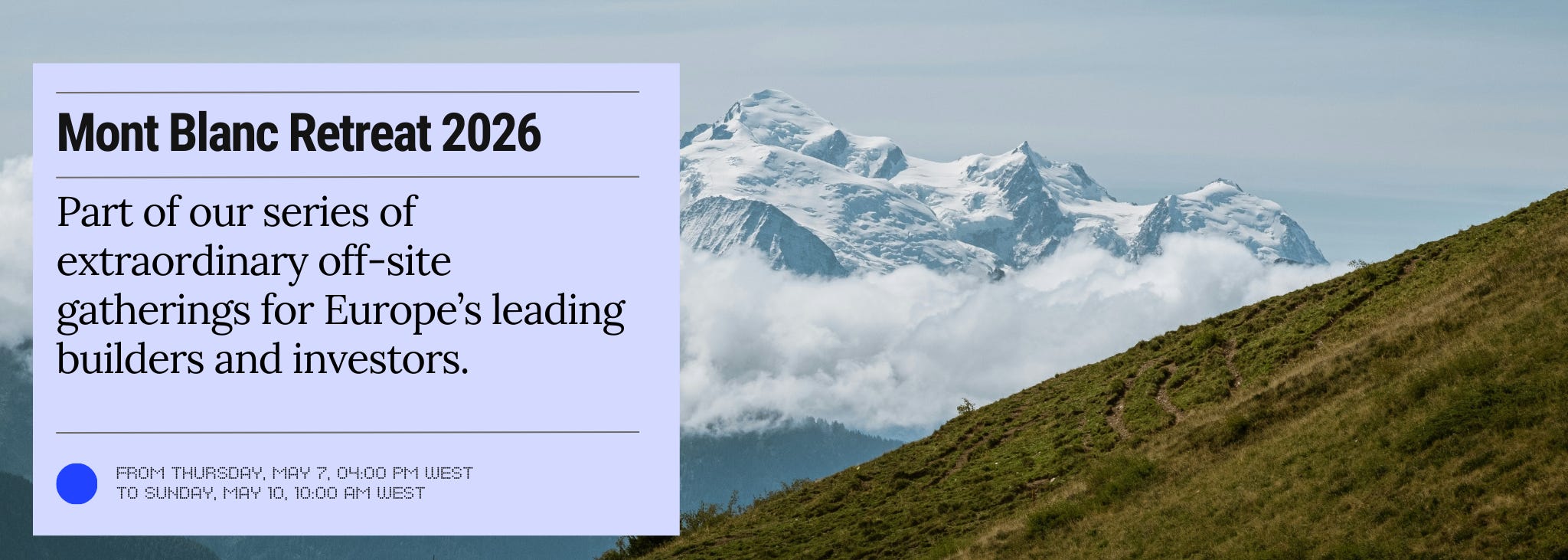

Mont Blanc Retreat 2026 | 7 -11 May | Piedmont and Chamonix

Join us in the French and Italian Alps for a small, carefully curated gathering in Piedmont and Chamonix, co-hosted with Paolo Pio (Exceptional Ventures) and Itxaso del Palacio (Notion Capital).

We’re bringing together a handful of thoughtful builders and investors for a few days away from the usual tech rhythm. Expect a balanced mix of guided treks and genuine downtime — mountain walks through spectacular scenery, long lunches, fireside conversations, and proper rest. And yes, for those who feel like it, even a bit of ice climbing.

You set your own pace. Push yourself physically, lean into deeper conversations, or simply breathe and take it all in.

There are no panels and no pitches. Just good people, honest dialogue, and space to reflect on the road ahead — and who you want to walk it with.

We’d love to have you join us.

Private Off-Site for Corporate Venture Leaders | 11–14 May | Piedmont

We are hosting a private, invitation-only off-site for corporate venture leaders and senior executives in the Piedmont region of Italy.

Designed as a deliberate alternative to traditional conferences, the off-site brings together a small group of experienced leaders for thoughtful dialogue, peer exchange, and reflection. Set in Piemonte’s wine country, the experience combines guided vineyard walks, unhurried meals at family-run wineries, and intimate fireside conversations in a private residential setting that fosters trust and candour.

This is a rare opportunity to step back, connect with peers, and reflect on leadership, strategy, and long-term perspective.

Learn more and request to join below.