Firm Spotlight | Pacenotes

Hybrid fund investing in top tier funds and co-investing in the breakaway companies of their portfolio for strong risk-adjusted returns.

🎧 To get emerging VCs straight in your ears: Listen on Spotify or Apple Podcasts.

This article outlines why the EUVC Investment Cub decided to participate in this investment opportunity. It is not, and should not be perceived as, investment advice.

The Memo [TL:DR]

Hybrid fund investing in top tier funds and co-investing in the winners of their portfolio to generate strong risk-adjusted returns. Pacenotes’ focus is on top-tier European tech funds.

GP is an exited founder and tech investor who has built two tech funds of €285M in total yield a skillset that allows the fund to bring value to GPs granting them unparalleled access.

The fund continues the strategy deployed by their previous fund, which outperforms many top quartile VC funds, to create a well-balanced tech fund of funds with the capability to double down on top performing portfolio companies.

Join the EU🔵VC Investment Club to explore the deal room and pick your funds.

On the move? 🚗 We’ve featured Jeroen in multiple episodes on the European VC podcast 👇 check out the two last two to better understand his thinking and strategy.

The Memo [Full Version]

As with our memo on 500 Istanbul, we’ve used the VC Fund Canvas to analyze the opportunity. As you’ll see below, we’ve made some updates as a result of our on-going effort to perfect it together with the EUVC community. X’s and O’s goes out to all who participated in this effort🙏

1. Thesis & Strategy

Pacenotes’ thesis is to invest in top tier funds and co-invest in their breakout companies to create a robust portfolio with strong risk-adjusted returns.

Top tier funds are defined by Pacenotes as funds that have proven to be capable of repeatably generating a return of more than 3x (TVPI). 75% of the fund is dedicated to fund investments, thus providing a solid foundation for stable returns and down-side protection.

To generate alpha/upside, up to 25% is dedicated to direct co-investments in the breakaway companies along the invested funds. For this reason, the strong direct tech investment experience of the team is absolutely integral to our passion for Pacenotes. See more on their ability to execute on these in a fund of funds setup below (cf. the 2nd section below for a bit more on this).

What is more, the fund is diversified across vintage, geo and stage but is skewed towards the early growth stage where the risk-return is most attractive. In this stage ticket sizes of € 1-5M for direct co-investments are also better positioned to acquire decent stakes. Pacenotes will never lead a deal and therefore does not compete with other funds.

Furthermore, on top of the co-investments done directly from the fund, Pacenotes will create SPVs to service LPs in exploiting the pro-rata rights secured in the initial Series A, B and C investments.

Market deep dive

The underlying market drivers for European VC are promising. A record $100B was invested in 2021 and 98 new unicorns were minted. The decacorn heard alone doubled in size to now number 26. With European tech creating value at its fastest pace, adding $1 trillion in just 8 months, Atomico concludes that the startup pipeline in Europe is at par with the US. All this is causing top US investors to double-down on Europe, only empowering the ecosystem further. While geographical differences in maturity level remain, talent mobility and distributed success is powering newer hubs. All of this creates a beautiful storm where getting exposure to all of Europe is paramount in a diversified tech portfolio.

Europe has its strongest ever pipeline of early stage companies. In fact, early stage companies in the region account for 33% of all capital invested globally in rounds of up to $5M. This makes Europe the second region globally when it comes to early stage investment, with a total of $3.8B vs the US at $4.1B.

But what is more important in the context of VC👇

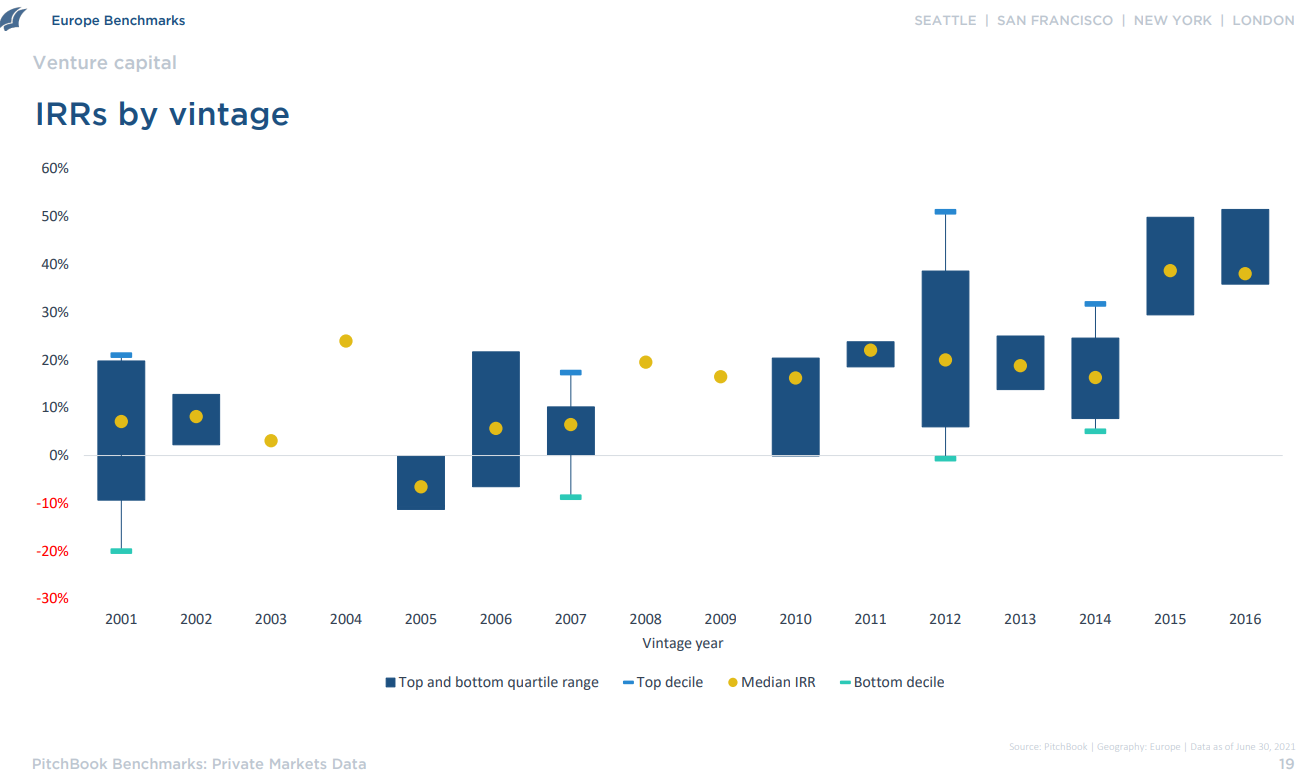

European VC is beating US VC & European PE, and outperforms across two decades 🤯

There’s only one conclusion. European venture capital is proving itself to be a highly attractive asset class: European VC outperforms its US counterpart.

New research shows that the top half of VC funds outperform public benchmarks and that VC fund of funds are more than worth their fees.

According to new scientific research half of all VC funds launched between 2009 and 2017 generated returns to investors, net of all management and performance fees. In other words, they outperformed the public market equivalents (PME) of both the S&P 500 and Russell 2000.

Research has also concluded that VC funds that outperformed in the past are highly likely to also outperform in the future. But returns for VC funds follow a power law distribution, making fund investing a game of access and picking. In our view, you really want to partner with the best. It’s the best way to avoid adverse selection. You don’t just meet great managers by accident. It takes skill, dedication and a process

VC fund of funds more than make up for their fees by selecting better VC fund managers than the average LP can do on their own.

Or the junked-up stockbroker you’ve got on speed dial.

Key take-aways on the market for VC Fund investing.

☑️ Venture is a maturing asset class providing strong net returns to investors.

☑️ Institutional investors (LPs) should double down on VC.

☑️ Getting access to the best VC funds will create a solid, predictable return.

☑️ VC FoFs are more than worth their fees if they can access the best VCs.

2. GP & Team

The Pacenotes team has previous founder & tech investment experience. This yields unparalleled access and ability to connect meaningfully with GPs around direct investment opportunities. Something exceedingly rare in the market.

Jeroen van Doornik, co-founder & general partner

Ex-founder with 15 years of experience in technology investments & top quartile investment performance. Formerly managing partner at Rabo Frontier Ventures with experience of building two tech funds of € 285M in total. LPAC member at Seedcamp and board observer at Speedinvest.

Notable fund investments include Seedcamp & Speedinvest in Seed, Northzone, HV Capital & Valar in early stage and Balderton and Greyhound capital in Growth.

Notable tech (co-)investments include Tide (Series B led by SBI group and Series C by Apax Partners), ProducePay (Series B led by Anterra, Series C by G2VP & IFC), Ageras (Series B led by RFV and Series C by Lugard Road), Candis (Series B led by Lightspeed), Wayflyer (Series A and B led by Left Lane & DST Global).

Menno Rijnsburger, co-founder & investment manager

Investment professional with broad experience in tech and fund investments, formerly associate at Rabo Frontier Ventures, analyst at StartGreen Capital and Accenture Strategy and Business Development at a renewable energy startup in Kenya called Riwik East Africa.

Jeroen & Menno have been working together at two different companies (StartGreen Capital and Rabo Frontier Ventures) where Jeroen hired Menno twice before jointly founding Pacenotes.

3. Track Record

Note: this section is considerably redacted compared to the information available to members of the investment club due to the sensitive nature of the information.

Together, the founding team has designed, built and executed on a tech Fund of Funds that outperforms many top quartile VC funds. We refer to this fund as the “track record fund” for Pacenotes.

In this “track record fund” there’s currently an unrealized upside that may lead the fund to yield more than >4,0x returns which corresponds to a top quartile performing VC fund in its vintage. As a fund of funds, which has a considerably lower risk profile (and carry!), this is astounding performance 🚀.

On top of this, the team made co-investments (with 10% of the fund) which may even bring returns to top decile VC returns which speaks to the strength of the strategy 🔥.

The EUVC Investment Club is investing into Pacenotes. Join us to explore the opportunity further with us.

4. Unfair advantage & value add

While Pacenotes’ thesis and strategy might not be revolutionary - invest in the best funds and co-invest with them in their breakout companies - it’s a surprisingly difficult strategy to execute.

Ask any GP and they’ll say that almost all LPs want co-investment rights. But they’ll also say that it’s equally rare that the LPs are able to follow through on these. The few that do, do so reactively and without a prepared mind (even though they’ve gotten quarterly reports from the GP for years so they could track the company). But what sets Jeroen and Menno apart from these is their proven ability to actually close co-investment opportunities due to their prepared mind and pro-active approach. This approach also resonates with the GPs of the funds to which Pacenotes commits.

Pro-rata rights on the table

The reason why this is such an interesting proposition to GPs is that they’re often leaving pro-rata rights on the table in later rounds. Having an LP that will pick this up (sometimes at a fee) and help fund, guide and open doors can be very powerful.

In consequence, Pacenotes becomes a hands-on lifecycle partner for its funds. by providing continuous funding throughout the funds’ life cycles and doubling down through co-investments. This is, to many GPs, among the core characteristics they look for in an LP.

To LPs the value proposition is exciting because it allows them, with a single ticket, to get diversified exposure to

well-established VC funds with a >3x track-record across multiple funds for downside protection;

direct investments that have proven themselves inside the portfolio of the very same VCs for significant alpha.

For the passive LP looking for broad exposure to European VC this is a match made in heaven.

The savvy LP looking for access to exclusive deals at Series A and beyond will feel like a kid in a candy shop.

5. Terms

Domicile: The Netherlands

Entity structure: transparent C.V. (similar to a Limited Partnership)

Target Size: 50M€

First close: 8M€

Final close: Q1 2023

Management fee: 1% per year on committed capital

Carry: 10%, with a hurdle at 1,8x net and catch-up.

GP commit: 1-2% (dependent on final fund size)

Legal counsel: Venture Lawyers

Fund notary: Zuidbroek

Tax advisor: Atlas

Regulatory advisor: Finnius

Accountant: Confinant

Fund Administrator: Fundrbird

6. Fund Model

VCs reading this section might want to pay some attention to the return profile that Pacenotes targets. For seed and early stage, the sought after performance is >5x and >4x respectively. And for growth and opportunity funds it’s 3x. Some good benchmarks there 🙏

As can be seen from the below illustration, c. 50% is dedicated to Seed & Early stage. 30-40% of which goes to Seed and 60-70% to Early Stage. The remaining c. 50% of the funds are divided between Growth (60-70%) & Opportunity funds (30-40%).

The commitments are also split across two vintages (2022 & 2023) and two continents (Europe + Israel & United States), which is interesting given the performance dispersion from vintage to vintage and geo to geo. This is one of the reasons why we, as a small ticket investor, and from a purely financial perspective, like fund of funds.

As our regular readers know, we refrain from going too deep on the underlying portfolio model in these public memo’s out of respect for the manager. As such, mic drop 🎤.

9. Governance & reporting

The team has experienced more than 300 funds and have used that broad exposure to develop their own setup. There’s a core founding team where Jeroen as the senior investor makes up the GP while Menno acts in the role of investment manager and rising star ✨. An operational team will be added to run the back-office, which is something we’re comfortable with as, honestly, much of this can be outsourced or run by a late-nighting GP. But given the handling of many co-investments and SPVs it makes sense to us that hires are in the pipeline. Pacenotes is aware of this and will, over time, hire an operations team consisting of a legal/general counsel and a finance director to handle all back-office tasks which allows Jeroen & Menno to fully focus on sourcing, closing and managing investments as well as on fundraising. The fund administration will be carried out by Fundrbird, a sophisticated and automated reporting and accounting company for investment funds.

The investment decisions of the founding team are double checked by a third fund investment expert in the investment committee. This is a healthy practice and, given the limited time-pressure on most of Pacenotes’ investments, shouldn’t cause delays or inhibit the team’s execution power.

Additionally, Pacenotes is setting up an advisory board for mid- & long-term strategy decisions and guidance along the way. The team is currently discussing these board positions with really big names in the venture industry (think Midas List VCs and unicorn founders) to join the advisory board.

Join us to invest into Pacenotes & other amazing European VCs ✊ Minimum investments starting at 1k€.

Risk Warning Investing in venture funds, start-ups and early stage businesses involves risks, including illiquidity, lack of dividends, loss of investment and dilution, and it should be done only as part of a diversified portfolio. The EUVC Investment Club is targeted exclusively at investors who are sufficiently sophisticated to understand these risks and make their own investment decisions. You will only be able to invest via EUVC once you are registered as sufficiently sophisticated. This content is for informational purposes only and should not be considered investment advice.

I'm ridiculously excited about backing JD and Pacenotes with our syndicate 🤩