The New Space Age is Near

Guest post by Bogdan Iordache originally published on the Underline Ventures page.

Since forever, it has been the destiny of humankind to explore the frontier – and today’s frontier is space.

Look up to the sky – we’re a miracle living on one of the millions of other pebbles in the universe. And after millennia of civilization, we’re only truly conquering the orbit of our planet.

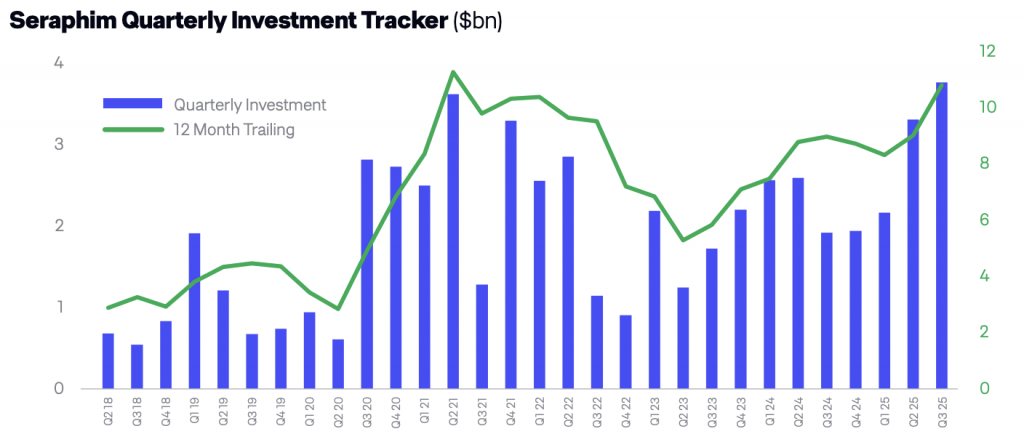

Similar to the Internet 30 years ago, space tech is just emerging, although the building blocks have been around for longer, and Q3 2025 space tech investments have hit a record $3.5b value, as per Seraphim’s Space Index, driven by new demand (defense, EU sovereignty), better tech, and new regulations.

80 years ago, mankind set out to conquer space. Each space program reached further — first the Earth’s orbit, then the Moon, and later the outskirts of our solar system. Their progress has been slow and heavily dependent on state-sponsored research and infrastructure.

However, in 2015, SpaceX reignited the space race by inventing the reusable rocket—an incredible accomplishment, especially for a private company, which enabled much faster iteration in all aspects of spacecraft development. Since then, SpaceX has launched over 500 successful missions.

The decrease in cost/kg launched into space, the miniaturization of electronics, more reliable and powerful engines, better energy sources, and communication infrastructure have allowed for an acceleration of space development, starting with the Low Earth Orbit (LEO) satellites.

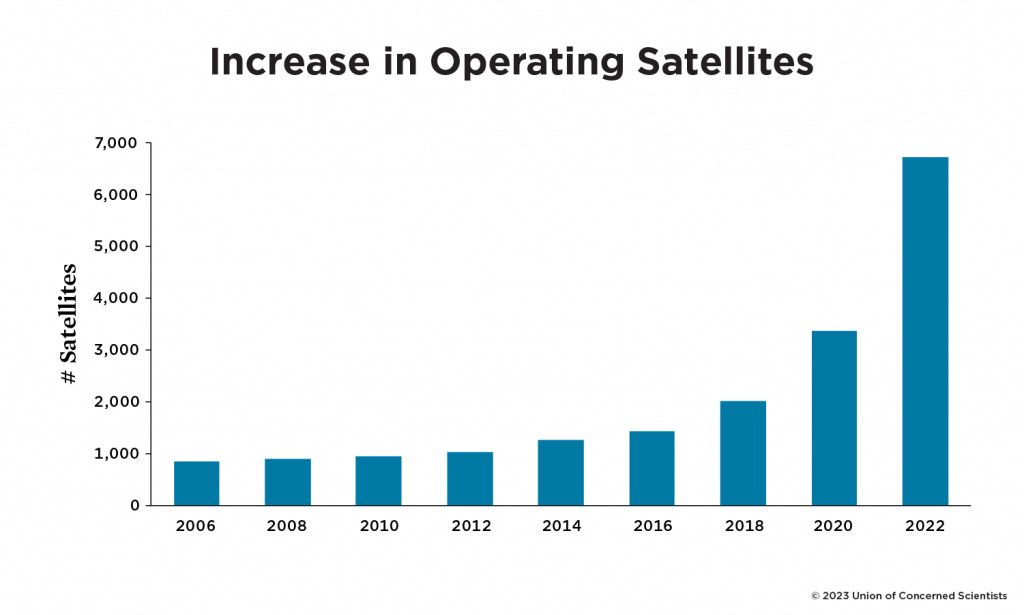

The proliferation of LEO satellites, which are smaller and cheaper, is the primary reason why the number of operating satellites has been growing by 40% in absolute terms year by year, and it’s projected to continue growing at the same rate until at least 2030.

Source: https://blog.ucs.org/syoung/how-many-satellites-are-in-space-the-spike-in-numbers-continues/

This new class of satellites has extended existing services and enabled many new, exciting use-cases.

Earth Observation allows satellites to capture optical, radar, SAR, RF, thermal, and hyperspectral data, and use it for a multitude of use-cases, including forest and crop monitoring, city monitoring and planning, tracking ships, disaster monitoring, defence tech use-cases, and many others.

By far the most successful use-case, EO has already generated multiple billion-dollar companies – such as Planet Labs, Maxar Technologies (now Vantor), ESRI, and many others.

But LEO satellites, and soon VLEO satellites (Very Low Earth Orbit), have enabled other services, such as:

high-speed, low-latency broadband internet offered by Starlink, the satellite constellation developed by SpaceX,

Hubble Network’s in-orbit satellite Bluetooth data connectivity service,

in-orbit microgravity manufacturing for pharmaceuticals and special materials developed by Varda Space Industries (US) or Space Forge (UK),

in-orbit data centers built by Starcloud (US), using the low temperature in space as a cool-off system.

However, all this infrastructure has to be put into orbit and then maintained.

And SpaceX is not the only one providing launch services and building reusable rockets anymore. Blue Origin (US), RocketLab (NZ), Firefly (US), Isar (DE), Space Pioneer (CN), Skyroot (IN) are in different stages of building launch vehicles for different use-cases (small/mid/large payloads), joining established players such as Arianespace (FR).

New satellite manufacturers such as EnduroSat (BG), Apex (US), Kepler (CAN), Gomspace (DK), and many others are also launching new products, along with the existing traditional satellite manufacturers such as SpaceX (again, US), Airbus (FR), Thales (FR), Lockheed (US), and others.

To power this accelerating industry, new players are developing power and propulsion, communications, optics, telemetry, and re-entry capsules. While some of these components are proprietary for each manufacturer and act as a differentiator, many others are similar and will be manufactured at scale for all of them.

One special use case is space cargo, which enables direct cargo transportation from one location to another on Earth via orbit. Companies such as Space Cargo (LU), Atmos (DE), and The Exploration Company (DE) are building specialized cargo space vehicles.

Maintaining all this infrastructure in space is not yet a “today problem”, but definitely a “tomorrow problem”.

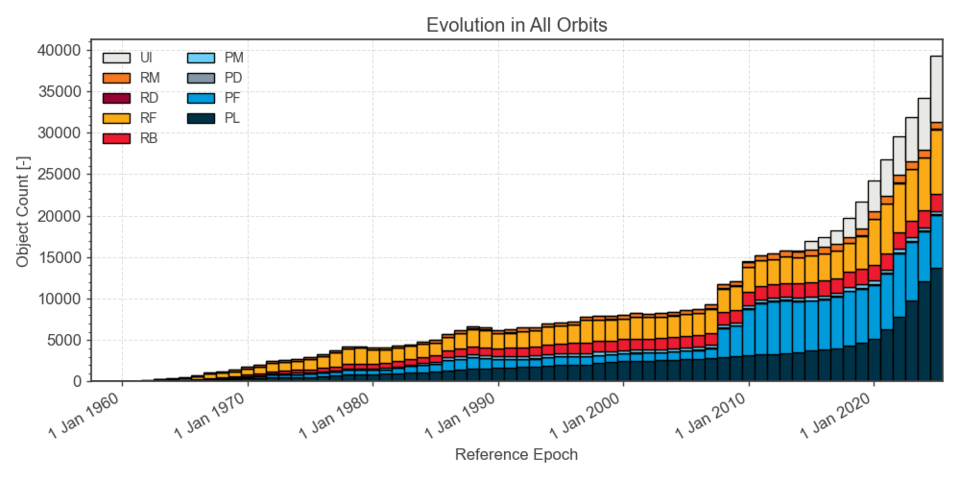

ESA’s Space Environment Report shows an acceleration of all tracked objects in Earth orbit over time:

Source: https://www.esa.int/Space_Safety/Space_Debris/ESA_Space_Environment_Report_2025

A busy orbit means more challenges for space monitoring, mission design and simulation, in-space maneuvering and servicing, and, later on, debris removal. And many new space tech startups are already working on these challenges.

Take debris removal — imagine maneuvering a satellite flying around the Earth at over 25.000 km/h, to gently push spacecraft debris or a piece of rock, so that it is directed towards the Earth on the right trajectory, and it does not collide with other in-orbit satellites or in-mission spacecraft, before moving to the next task. To fully exploit the Earth orbit, we’ll need to solve incredibly complex problems, requiring improved engines, sensing capacity, and other capacities.

The stakes are getting higher, and failures now cost millions. As launches, satellites, and human spaceflight are becoming increasingly common, they need to be easily tracked, financed, and insured, and companies like Flow Engineering (UK), Epsilon3 (US), or Charter Space (UK/US) are building the right products for the job.

But not all satellites need to be fully assembled on Earth; some parts can be manufactured in orbit. In-space manufacturing providers, such as Dcubed (GE), Solestial (US), or Redwire (US), are using either 3D manufacturing or rollout solar array technology to manufacture or assemble solar panels in space directly, simplifying the deployment of satellites.

Space is also the next barrier of defense. The Trump administration, which previously established the United States Space Force in 2019, has promised to put a special emphasis on space defence and potentially revive the “Star Wars” plan first promoted by the Reagan administration to create a space force of satellites equipped with laser weapons.

Until then, using Earth Observation services for defense purposes has become common, especially in the context of the Russian war in Ukraine, where the services provided by ICEYE (FI) have proven to be highly efficient.

So far, we haven’t even left the orbit.

Beyond VLEO, LEO, and GEO, we can start planning for asteroid mining, Mars colonies, and deep space exploration.

The future starts again tomorrow.