Welcome tothe newsletter that rounds up the week in European Venture from a GP/LP perspective.

And a heartfelt welcome to the 144 newly subscribed venturers who have joined us since our last post! If you haven’t yet subscribed, join the 7,253 angels, VCs and LPs 👇

And help us connect European venture by sharing the below super promotional pre-written email with your friends 💖 we’ll buy you a 🍻 next time we meet for it!

How do you source deals?For most VCs, Affinity.co is the go-to CRM. But do you know how to get the most out of it?

The team recently put out their 2023 VC Invetment Sourcing Guide and I think it’s well-worth a read - and the perfect hand-out to your associates and analysts (!).

🤔 Why track records are so important 💾 What data's required 📈 What the track record should cover ⛔ Top 3 mistakes made by VCs 🧙♂️ Why storytelling is key and how to compensate for a thin record (so far).

About Michel & Betterfront: Michel is the CEO and co-founder of Betterfront, a B2B vertical SaaS company dedicated to private markets. Previously, Michel led due diligence and fund managers selection for the Siemens’ pension fund. He started Betterfront out of his frustration of poor alternative investment analytic solutions.

Campfire London

Wednesday, Feb 8, 2023, London

Been wondering how some dealmakers remain successful in the face of a shifting market? Register today and see what Affinity's Relationship Intelligence conference, Campfire London, has in store for you on February 8!

The Super Angel, #03 Joe Cross, ex-operator angel on thesis development, building your network and adding value

Today, we're happy to welcome Joe Cross, early stage angel investor, with a portfolio of around 25 companies so far, and LP in Cocoa. He focuses on companies with the potential to make a positive impact at scale, and helps founders on growth & marketing challenges across a whole mix of sectors. Previously, he was employee #12 at (Transfer)Wise, where he wore various marketing & growth leadership hats from 2012-2020.

In this episode you’ll learn:

How Joe thinks about applying his ex-operator skill set to add value to founders & why it’s often operations and tactics over strategy!

Why Joe’s investment thesis is centered around Good, Big & Fast and how he thinks about impact investing.

Why Joe is changing strategy from having done 25 investments in just 2 years to doing fewer more concentrated bets in the time to come

How Joe thinks about building valuable networks to access and win the best deals

The European VC, #145 Monik Pham, Pact VC

Today we are happy to welcome Monik Pham, co-founder of Pact VC, an early stage tech fund backing mission driven founders with global ambitions. They have over 40 years’ experience building businesses in Asia, Middle East and India, and a strong track record investing in them in the UK and Europe. Pact invests in seed-stage companies under three themes which they call their ABCs - Access, Betterment, and Climate.

In this episode you’ll learn:

On Pact’s origin story and raising a fund, the route to their name and having Anne Hathaway as an LP

Everything about Pact’s ABC thesis and how it connects and leverages the team’s track record and experience

Why Pact enters with large initial tickets and how it impacts their operational setup

A deep dive on impact & diversity in VC

The European VC #144 Fridtjof Berge, Antler

Today we are happy to welcome Fridtjof Berge, Chief Operating Officer and co-founder of Antler, a startup generator and early-stage venture capital firm. Fridtjof works with a global team dedicated to developing the next generation of world-changing technology companies. He oversees external activities across the firm globally and serves as a member on its investment committees.

In this episode you’ll learn:

The founding story of Antler, where the name came from & where the team drew inspiration from

Why and how Fridtjof and the team built a rapidly scaled global VC firm

The Antler GP Talent Thesis

How Antler thinks about marrying local and global and the role of process and systems in doing so efficiently

How Antler thinks about building GP teams for new locations

Why Antler launched out of Singapore

GIFs & Memes 🙊

🚨 View the newsletter in browser to watch the films without it being a mess. Promise it’ll be worth it.

Being a founder in today’s market

VCs introducing a new portfolio company to their super helpful not at all distracting, value creation team:

2022 vs 2023 VCs response to portfolio companies asking for value add/bridge financing

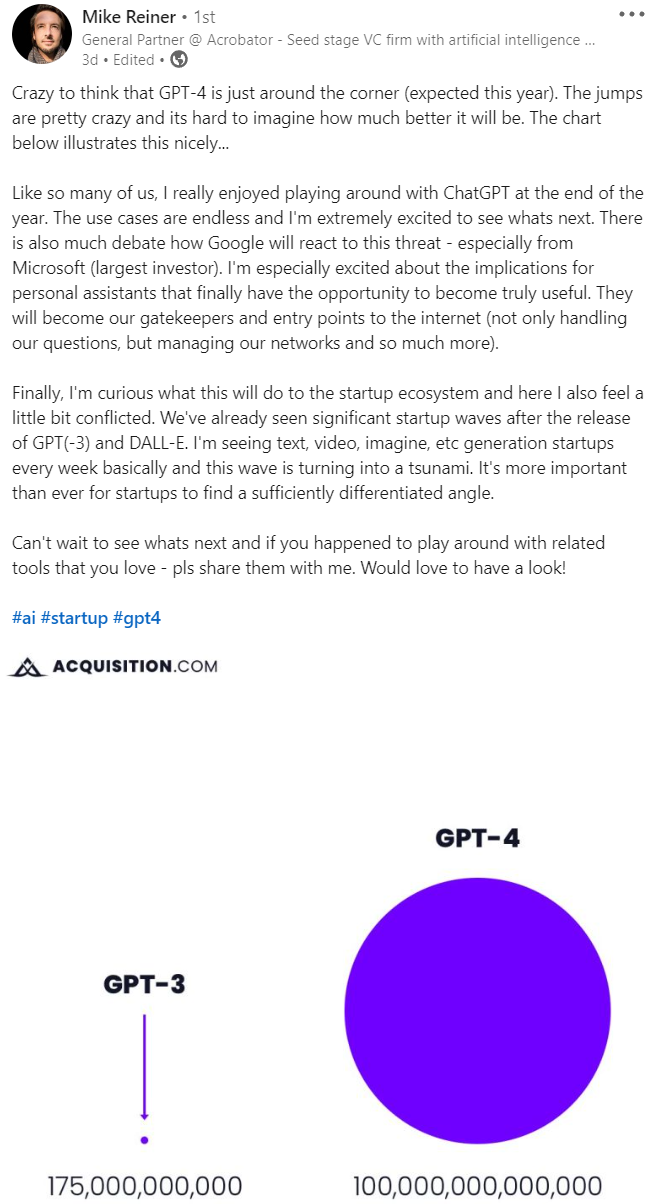

Open-AI, Google and Microsoft is on the lips of everyone these days. Mine and Chris’ too. News is that OpenAI is discussing a new round at $29Bn, so what does Chris think about this?

It’s hard for my mind to not quickly think about all the recent conversations about returning to value investing and all that. I mean. Let’s look at the facts about OpenAI:

Understandably, the business hasn’t disclosed any revenue numbers, but the FT suggests a few $10m, but it’s unclear.

Clearly, all the the greats of VC believe that this is one of the future’s big bets and some have even compared it to the next Google ..

OpenAI as the next Google. What do you think about that statement Chris?

Well, to make that comparison, the obvious thing would be to dive into Google’s history:

Google started in 1998 with a banner ads business

In 1999 revenue was sub $1m

In 2000 the company raised $25m at an appropriate valuation of $125m

By 2023 revenues grew reportedly to $1Bn

Successfully achieved an IPO in 2004 at $23Bn market cap

So, is OpenAI worth $29Bn in ‘23? Well, if the revenue forecast is to get to $1Bn in the next 3 years (which the above suggests Google achieved) then it has some equivalence to Google history. But there’s many ifs and buts in that… I think I’ll let the reader make their own conclusions on that one.

But one thing remains a constant: investing at seed looks like a very smart thing to do!

Reflecting on this conversation with Chris, I came to think of the below post by Mike from Acrobator Ventures, one of our shared portfolio VCs 💖

This week, we published the second instalment of the series “Why invest into venture funds”. Read it below and join us to dive deeper.

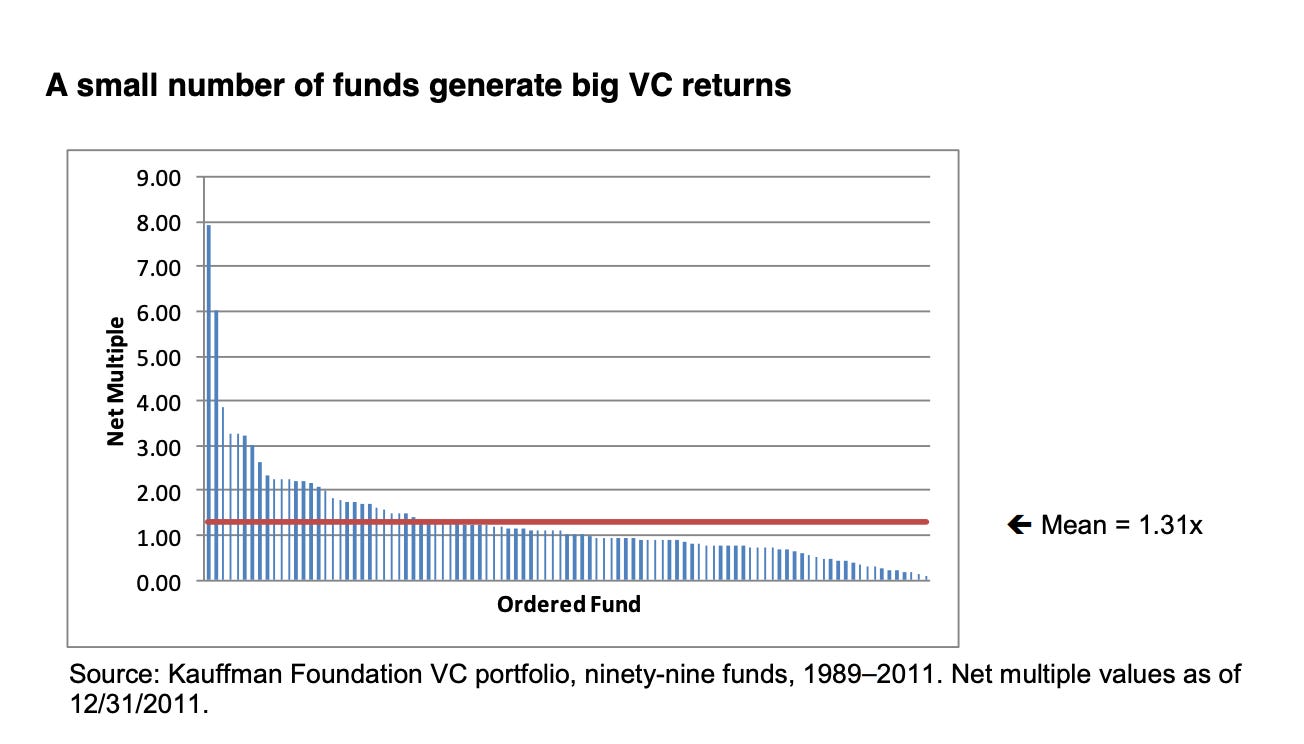

Diversification is, by no means, the only reason (or main reason for that matter) why we think funds are a good addition to your angel portfolio. But hey, it’s still a pretty solid one 💪.

A model of venture returns built by Steve Crossan suggests that, under the power law and using reasonable assumptions, rational venture investors should have bigger portfolios 🤔

The model does, as expected, have its limitations 😱. It’s very sensitive to the value of alpha, we are yet to understand what realistic ranges for alpha are (it outperforms reality, which is likely due to a too low value of alpha), the modelled portfolios are not independent, the universe of investible startups in reality is limited (and much smaller), it has an unrealistic positive minimum return, and our inner skeptic 🧑⚖️ could probably go on with the naysaying and finger pointing.

Fair question. Well… All things considered the overall trend that more investments are better is very consistent 🤯. Even when we fiddle with the value of alpha, run the power law model with pooling or reduce returns by zero-ing out returns below certain thresholds 😲.

All together we conclude👇

Your chance of tripling or quintupling your money is significantly higher with a bigger portfolio

Your chance of 10xing your money doesn’t decrease

What’s specially interesting in the above model is that in any given cohort, fund performance was dominated by whether you got into that 1 investment. That one single true outlier 🚀! Any fund that does will tend to outperform every other fund in that cohort. In other words, the upside of a true outlier outweighs the downside risk of losing money on all others. This is why we’re not hunting for funds with a more conservative, PE-like, investment strategies. We don’t care that much for investors looking for 3-5x’ers and low loss ratios.

We care for the unconventional contrarian investors hunting for the 10x and plus. To hit the true outlier, you need to take big swings. And often under extreme circumstances.

But there’s a third reason to have a bigger portfolio. And it should not be neglected 🚨. As your portfolio grows the likelihood of you loosing money decreases. According to the model, a portfolio of just 5 investments has more than 40% likelihood of losing money. This goes down rapidly until portfolios sizes between 100 and 150 when there’s very little or zero chance of losing money.

So you’re saying I should index venture?

⬆️ gif representation of where EUVC stands on indexing venture ⬆️

Not at all. When you invest into funds, you still need a quality filter. We’ve got north of 5.000 VC funds in Europe (anyone out there with data on this? This is our best estimation so far 🤷), and returns for “the average VC” aren’t exactly spectacular.

ot at all. When you invest into funds, you still need a quality filter. We’ve got north of 5.000 VC funds in Europe (anyone out there with data on this? This is our best estimation so far 🤷), and returns for “the average VC” aren’t exactly spectacular.

That’s why we’re partnering with one of Europe’s very best institutional LPs around sourcing, diligencing and picking the funds we bet on in our LP syndicates. Together, we’ve screened more than 2.500 funds, actively track more than 1.000 and have invested in more than 65 funds, yielding an underlying startup portfolio in excess of 1.500 companies. So far 😏….

In Europe, some have made it very popular to talk about “indexing venture capital”. You don’t want to index VC - not even at the fund level.

If you index, you get the average. And you don’t want the average. So if anyone tries to sell you on indexing, I’d suggest you take a cue from television personality, entrepreneur and Shark Tank investor Lori Greiner 👇.

Instead, we say go for a carefully selected set of funds and optimise for returns and strategic value. This is where the EUVC LP Syndicates come into play as we give you access to such a set of funds and the freedom to pick which manager you want to back & work with 🤝. Note that I highlighted “work with”.

ℹ️ Watalook - is a beauty tech startup, designed to empower and help independent beauty professionals grow and manage their beauty businesses more efficiently.

Looking hot is all I can say ❤️🔥

“The EUVC team has figured out how venture works and what lacks in our market. Many investors haven’t yet figured it out. If you want to earn good returns in venture you need to invest in a lot of companies (so many that you can hardly do it on your own). While funds can do it for you, there's still one problem: usually you don’t have access to the best funds. This is because venture is a game of access. And only the best funds have access to the best deals. With EUVC you can invest in a diversified portfolio across the best funds in Europewhile becoming part of a value-add community that gives you the chance to get real close to the assets and learn from what would otherwise be a purely passive investment. I really like this strategy, and I think it’s the ideal way to get exposure to venture asset class.”

This week’s stories 🗞️

Narrative violation in VC

So, we’ve had some pretty cool years for VC. Actually a full decade of cool years more or less. With cool, I actually mean hot🔥 with (even) long term performance of the asset class landing squarely at the top of the list. But is it all just fake? Nnamdi Iregbulem, Partner at Lightspeed Venture Partners wrote a piece wielding his economics degree with brilliance that might suggest that (at least) some of it is. I’ll republish practically all but some introductory stuff of his original article below. I think we’re all looking for analyses rooted in fundamentals rather than just quick knee-jerk reactions these days and that’s exactly what Nnamdi delivers. Enjoy 💖

Supply and demand together determine equilibrium prices (Y-axis) and quantities (X-axis)

In simple terms, when everyone wants the same thing and wants it really badly, the price tends to go up and more of that item gets bought and sold. When everyone wants to produce and sell the same thing and wants to do so really badly, they compete against one another, driving prices down to accommodate the increased activity.

In venture terms, when investor demand for startups rises, valuations increase and more deals get inked. When entrepreneurial supply expands, valuations decline and more deals get done.

Venture deals and valuations have both grown over time, so it's all demand-driven right?

Not so fast.

The key is to "de-trend" the data first. We need to remove the long-run trend and then compare deviations from that trend.

Ignoring the details, here's what that looks like (data normalized and smoothed slightly to remove noise):

Lo' and behold: deal flow and valuations fluctuate together around their respective trends.

OK, maybe that's not always true, but it's nearly always true. Early stage is the exception to the rule.

Seed financings were negatively correlated with valuations before roughly 2017:

When deal flow increased, valuations plummeted, and vice versa

This smells like supply to me – there was only so much investor demand, so when more startups came to market, they competed, and prices tended to fall, benefitting investors. When the supply of startups contracted, prices rose as investor battled over the few remaining deals

Series A rounds used to be positively linked to valuations, but they've de-correlated over the last few years:

Pre-2019, Series A deal flow and valuations tended to move in the same direction

Sounds like demand to me – startup supply was constrained, so investor sentiment drove the market, moving prices up as they grew more eager and down as they soured on the venture ecosystem

Across growth and later stages, deal flow and valuations are unambiguously positively related, moving almost in perfect unison for the last decade:

Demand clearly wins it – late stage supply is badly constrained, so investor demand is the prime mover. Their manic and depressive episodes move the market accordingly

Some of these relationships have shifted over time, so let's visualize that with rolling three-year correlations for each stage:

This is my qualitative narrative in quantitative terms:

The Seed stage flipped being negatively correlated to positively (supply → demand)

Series A de-correlated to effectively zero (demand → ❓)

Series B and later deal flow and valuations have always been strongly positively related (demand all day baby)

Channel attribution

This is the best evidence I've seen to date for the demand-side hypothesis.

The scorecard so far suggests demand reigns:

Investors are the primary driver of fluctuations in venture activity and equity prices around their long-run trend

Yes, more deals are getting done (so by definition more startups are getting funded), but that appears to be a function of increasingly desperate investors rather than increasingly bold and enabled founders

In other words, the supply of startup equity is badly constrained:

The venture ecosystem is supply-constrained – there isn't nearly enough startup equity out there to satisfy investor demand.

Additional capital drives opportunistic company formation at the Seed stage. However, the additional capital doesn't improve survival to the later stages – it simply drives prices up for the remaining companies – It's Valuations (Almost) All the Way Down

As a reminder, our evidence for this is the positive link between de-trended deal activity and valuations. That's a nice trick, but it only tells us at each point in time whether movements in demand or supply dominated. I want to explain the entire last decade or so of venture history in terms of supply and demand channels.

Yes, yes, history is not bi-causal, hammer looking for a nail, etc, but how about one more magic trick to close things out?

Warning: armchair econometrics ahead!

Let's stretch our simple supply and demand model to the absolute extreme:

Remember, a positive relationship between deal flow and valuations suggests a change in demand, while a negative or inverse relationship suggests shifting supply

So, we could simply attribute each quarter of venture activity to either demand or supply demand based on whether deal flow and valuations move in similar or opposing directions during the quarter

We can then cumulate the respective contributions of demand and supply to the growth of the venture ecosystem over time

Here's what that looks like for venture deal flow since early 2010. Demand is red, supply is blue, sugar is sweet, and so are you:

That's a lot of red out there:

The demand channel drove most of the growth in venture activity in nearly every stage other than Seed, where its relative contribution is closer to 50/50

Early stage supply contributed positively to deal flow from 2010 to about 2015 but then stagnated

Supply has never been a meaningful contributor at the growth and late stage and even seems to have contracted in certain cases

Et tu, valuations?

The story isn't much different for valuations, except perhaps with some signs flipped:

Here again, investor demand was the main driver, pushing prices higher in every stage

The increase in early stage supply in the early 2010s relieved some price pressure, but this eventually receded

The effect of late stage supply on valuations is somewhat noisy, but by the end of the sample those supply constraints appear to have driven prices higher, on balance

In case I haven't sufficiently caveated already: this is extremely unscientific. No Nobels will be awarded for this work (your subscription is enough reward for me, awwww), but it does serve as coarse, suggestive evidence that demand is, or at least has been, king in venture over the last decade.

Meanwhile, the supply of startup equity remains constrained. Rather than potential founders becoming more eager to start companies for "fundamental" reasons, entrepreneurs are reacting to investor sentiment. While there's been some growth in supply at the earliest stages, the fundamentals haven't necessarily improved much, which is why late stage deal flow hasn't grown any faster than U.S. GDP.

I'll repeat what I said earlier – we'll all be much better off if more people start companies for good, wholesome reasons that don't have anything to do with valuations.

There was a time where the notion of handing millions of dollars to an extremely young company sounded crazy, and anyone willing to do so extracted a significant ownership stake for taking on that risk. Founders got diluted, badly.

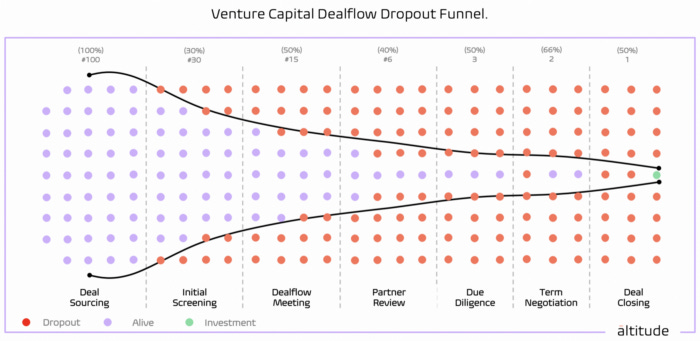

Let’s start with a regular venture capital dealflow funnel. Typically, when a deal comes into a venture capital firm it will run through a process with different decision gates, hence there are many points in an internal venture capital process where deals are lost.

This journey is illustrated in a simplified chart below.

Most deals actually dropout fairly early in the funnel, within the initial screening and the first internal dealflow meetings, roughly 90%.

“The remaining 10% of the deals are great, but for so many reasons the vast majority drops out of the funnel at some point.“

And very often, the dropoff from 10 - 1% isn’t caused by factors internal to the startup, but rather the match with the VC.

Just think about it, if a VC looks at 100 deals and ten happen to be great opportunities and they execute only one — what happens to the nine great deals, which just don’t fit to the respective VC?

Well, this is what Trojan is all about — They want to see these deals.

If we do the deal, we’ll reward you for bringing it to us with a five figure finders fee. This is a closed network. Confidentiality is very important to us, if you want to be involved then let us know. - Marc Penkala

Sounds interesting?Read the full article here, including who qualifies to join, investment criteria and how to get in touch 💌

Universe 25 - the world’s most terrifying experiment

"The "Universe 25" experiment is one of the most terrifying experiments in the history of science, which, through the behavior of a colony of mice, is an attempt by scientists to explain human societies.

The idea of "Universe 25" Came from the American scientist John Calhoun, who created an "ideal world" in which hundreds of mice would live and reproduce.

More specifically, Calhoun built the so-called "Paradise of Mice", a specially designed space where rodents had Abundance of food and water, as well as a large living space.

In the beginning, he placed four pairs of mice that in a short time began to reproduce, resulting in their population growing rapidly.

However, after 315 days their reproduction began to decrease significantly.

When the number of rodents reached 600, a hierarchy was formed between them and then the so-called "wretches" appeared. The larger rodents began to attack the group, with the result that many males begin to "collapse" psychologically.

UNIVERSE 25: John Calhoun crouches within his rodent utopia-turned-dystopia that, at its peak, housed approximately 2,200 mice. Calhoun was studying the breakdown of social bonds that occurs under extreme overcrowding, a phenomenon he termed a “behavioral sink.”

As a result, the females did not protect themselves and in turn became aggressive towards their young.

As time went on, the females showed more and more aggressive behavior, isolation elements and lack of reproductive mood. There was a low birth rate and, at the same time, an increase in mortality in younger rodents.

Then, a new class of male rodents appeared, the so-called "beautiful mice". They refused to mate with the females or to "fight" for their space. All they cared about was food and sleep. At one point, "beautiful males" and "isolated females" made up the majority of the population.

According to Calhoun, the death phase consisted of two stages: the "first death" and "second death." The former was characterized by the loss of purpose in life beyond mere existence — no desire to mate, raise young or establish a role within society.

As time went on, juvenile mortality reached 100% and reproduction reached zero. Among the endangered mice, homosexuality was observed and, at the same time, cannibalism increased, despite the fact that there was plenty of food.

Two years after the start of the experiment, the last baby of the colony was born. By 1973, he had killed the last mouse in the Universe 25. John Calhoun repeated the same experiment 25 more times, and each time the result was the same.

Calhoun's scientific work has been used as a model for interpreting social collapse, and his research serves as a focal point for the study of urban sociology.

Watch a film made about the study below 👇

Ukrainians Can Destroy a Russian Tank For About The Price of a Nirvana Artifact.

Hunter Walk took me for a trip down memory lane. Wanted to give you the same chance 🛣️.

One thing is for sure, I never should have tossed those hair metal concert relics and other memorabilia from my teens. You know, the ones that in the eras before social media you’d buy and wear to school the next day to show off that you were At The Thing.

[Sidenote, my first concert was 1985 Madonna ‘Like a Virgin’ tour w Beastie Boys opening. The t-shirt might have had that old school raised webbing on her bustier top]

I’ve been sharing the above linked FT article a lot because it’s so relatable to us of a certain age. Perhaps even more than ‘mom threw out my baseball cards!’ (most of which have plummeted in price anyway), almost every I know had some variety of this gear that got tossed, worn out, lost, or traded away. Most of my stuff is gone although I did manage to locate a Grateful Dead Giants Stadium (NJ) tie dye and a Poison tour short (unfortunately later era — by that I mean third album). So it was top of mind when I read about another object which costs just a few thousand dollars.

“War is an economy. It’s money,” said Graf, a stout, bearded Ukrainian soldier in charge of his unit’s drone team. “And if you have a drone for $3,000 and a grenade for $200, and you destroy a tank that costs $3 million, it’s very interesting.”

As the Russian invasion approaches its year anniversary the suffering inflicted is heartbreaking. But the resistance of Ukrainians, and their forced resourcefulness, is quite inspiring. The activities describe above are of course more commonly known as asymmetric warfare and practiced by all sorts of fighters, many of whom are more morally compromised than the men described in the Times article.

To get the grenade closer to the desired weight, his team has been using a 3-D printer to try to make a lightweight casing that can hold the explosives needed to penetrate a tank’s armor. The painstaking task involves experimenting with grenades of differing designs, clasped in a vise in their workroom, and operating around the explosive mechanisms to fine-tune them.

It’s just like my life, only if making an error in an Excel spreadsheet caused my laptop to combust with the force of a land mine.

This blog post doesn’t end with some grand statement of economic theory or judgment about a world where some fashionable people are wearing off the shoulder grunge nostalgia to brunch while others are shaving ounces off of a bomb.

A simple solution to a big problem

This CNN article about a startup called Satavia who can remove 57% of Airtravel’s warming impact with a pure digital play, had me remembering how beautiful a simple solution can be.

On a clear day, with the right weather conditions, a portion of the sky busy with commercial flights can become riddled with contrails, the wispy ice clouds that form as jet aircraft fly by.

They might look innocuous, but they're not -- contrails are surprisingly bad for the environment. A study that looked at aviation's contribution to climate change between 2000 and 2018 concluded that contrails create 57% of the sector's warming impact, significantly more than the CO2 emissions from burning fuel. They do so by trapping heat that would otherwise be released into space.

And yet, the problem may have an apparently straightforward solution. Contrails -- short for condensation trails, which form when water vapor condenses into ice crystals around the small particles emitted by jet engines -- require cold and humid atmospheric conditions, and don't always stay around for long. Researchers say that by targeting specific flights that have a high chance of producing contrails, and varying their flight path ever so slightly, much of the damage could be prevented.

Adam Durant, a volcanologist and entrepreneur based in the UK, is aiming to do just that. "We could, in theory, solve this problem for aviation within one or two years," he says.

The events of this year — the war, inflation, market downturn — will continue to heavily influence 2023. But, that said, VCs [in CEE] also raised a record-breaking amount of funding this year, which will have an impact on the ecosystem in the upcoming months.

With the market correction, we’ll see a drop in startup valuations and less investing based on hype, and more investing based on creating actual value. With inflation, potential customers will closely watch their spending, and the startups which offer the biggest and most necessary value will be better able to operate, earn cash and thrive.

We also started seeing big layoffs from the startups who raised huge rounds — it’s a chance for talent redistribution and more cost effective hiring. In terms of industries, I’m betting on security (in fintech, API, blockchain), AI and all low-code and no-code solutions.

The uptake of remote work has made many CEE entrepreneurs stay in the region and build their international business from here, rather than relocate to the west. With the growing number of unicorns, there are more and more alumni of regional startups starting their own companies in CEE and raising local and international funding. We also have more serial entrepreneurs who’ve achieved some exits, but are still hungry for bigger ones. These trends are also likely to affect the ecosystem in 2023.

In CEE, the overall climate is similar to the one we saw in Europe in 2021, and the trends in 2023 will be very similar to the trends of H2 2022. What is great is that we are seeing the fruits of the growth from 2021; the volume of funding is, comparatively speaking, quite high.

The biggest “drama” at the moment is in early-stage investing, from the first investment up to pre-seed. Here, due to the state of the market and macro trends around the world, the conditions of negotiation are very tough. Also, many government-backed accelerators are no longer government funded. This all makes the estimated number of startups funded in the early stage lower.

“Having said that, the overall panorama for CEE startups is quite good, as they are usually way less capital intensive, way more resilient, breakeven focused, less speculative and unicorn driven”

This creates a good pathway to growth in the next five years for this region. If they can survive with little, when opportunities for growth come along, they will be capable of capitalising well.

Yes, that’s not Sifted’s original photo of Bogdan. But in a past article by Zosia, he was styled as Batman without Robin, which I just freaking love.

2023 will be the year of the unknown. With a potential deep global recession looming over the world, a significant drop in the valuation of tech companies, many startups with short runways and a slowdown in venture activity, and an active military European conflict due to the Russian invasion of Ukraine, one thing is for certain — we don’t really know what 2023 will look like.

Given the uncertainty, caution will probably be most venture investors’ strategy, and the flow of capital will start slow and may pick up again by the end of the year. If you’re a founder, it would be ideal not to need to fundraise in 2023. If you still do, start early (six months in advance) and prepare a plan B in case the fundraise takes longer or fails to materialise. And let’s hope for the best.

Read the full article here.

How to cope when you meet someone younger and more succesful than you

Being a podcaster turned investor with Harry Stebbings staring in my face daily on my LinkedIn feed, this one comes home here. Or at least, it should, if I weren’t so busy thinking that I’m above that type of feeling. Hope the proverb “Pride comes before a fall“ doesn’t apply here.

Last Wednesday, I turned thirty-five.

As a newly geriatric tech worker, I regularly encounter people who are younger and more successful than I am.

If you’re not familiar with the despair that accompanies these interactions it’s because you are either Jeff Bezos or, a newborn baby.

While our ancestors only had to deal with these encounters in person, we moderns are under assault at all times. Whether you’re listening to a podcast or scrolling social media, you’re bound to come across one of these younger, more successful people flaunting their latest professional milestone or passive income stream. Unlike our grandparents, we don't have the option to just move away. So, we must learn to cope.

Fortunately, in my thirty-five years of living, I have developed several strategies that will help you overcome the existential dread of your next encounter with one of these younger, successful types:

1. Assume they aren’t actually successful

Sure, this guy says he “sold his company,” but how much money did he reallymake? Is he even twenty-seven, or is he making that up too? Sad that he needs to lie about his success to get strangers to like him…

2. Picture their misery

Even if he did make some money from selling his company– at what cost? Does he have any friends? His girlfriend looks pretty miserable– maybe it's because of their debt burden from his gambling addiction.

3. Question the value of success

What good is "success" anyway? It's not like earning more money makes you any happier. Didn't you once read that $70k per year was all you needed for a happy life? Was that adjusted for inflation? Who cares.

4. Rewrite your own narrative

It's not like you haven't been successful– you're just playing a different game. This guy did exactly what his parents expected while you pursued your own path. One that isn't measured by society's standards. When you think hard enough about it, you actually feel kinda bad for this guy.

5. Despair

Jesus, are you really that insecure? Has one encounter with a stranger really turned you into such a petty person? Maybe if you were more secure you would have achieved more of what you wanted to in life. Maybe if you were less obsessed with status, you would be a happier person.

6. Pursue self-improvement

Okay, you can't change the past, but you can certainly improve the future. Start eating more salads. Get back to lifting three times each week. How much does testosterone replacement therapy cost?

7. Compare yourself to older, less successful people

When you really think about it, things could be much worse. You could be that investor who was a couple of years ahead of you in college that got ousted from his firm after his deleted Tweets got leaked. Or what about your old boss who's still stuck in the same job after five years? Bet if you went back to that company you'd end up being his manager…

8. Be Grateful

Or maybe, you don't need to compare yourself to others to appreciate what you have.

Maybe it's enough that you get the opportunity to spend another year, another month, another day, another minute above ground.

Sure it's an emotional roller coaster of triumphs and setbacks– but that’s just what it means to be human. What else could you ask for?

European LP’s reflections on Jason Lemkin’s post on VC Dry powder, LP dynamics and what will happen in 2023.

This week Jason Lemkin shared his views on what would happen in 2023 and had some considerations about LPs that I couldn’t quite make up my mind about. So I asked two friendly LPs for their take. Check it out below.

Yes, there is a lot of "dry power" in venture. But for now -- it's not putting any pressure on VCs to invest. In fact, quite the opposite.

2022 was sort of a tale of 2 worlds. At the start of 2022, things were still part of the Boom Times of 2021. Unicorns were minted daily and weekly, and valuations were sky-high. By late Q1, it was over. And things just got tougher and tougher as the year went on. Growth rounds essentially stopped.

So far, things aren’t any better in 2023. But they are arguably calmer. Everyone now has a thesis for investing in 2023:

1/ Successful seed investors are planning to invest as usual, just looking for lower valuations.

2/ Successful, established growth investors are mostly sitting on their hands. They are hoping to do maybe 10% of the deals of 2021.

3/ Many seed investors probably can’t raise another fund, unless they have amazing results or strong LP support.

4/ Upstart growth investors have mostly disappeared. “One and done” new funds, random SPVs, Tiger’s deal-of-the-day, Softbank loving SaaS … that’s all gone for now.

Now, there’s just one point I think it’s important for founders to understand in 2023, and it’s both important and non-obvious:

-> Yes, there is tons of “dry powder” in venture today. But now, with one exception, there is zero pressure to deploy it, to invest it. None.

What does this mean? Well, VC funds are in most cases sitting on tons of undeployed capital. You might think that means they have to invest it, even in a down market. But that’s wrong — at least for 2023. VCs have their own investors, Limited Partners, or LPs. And right now:

-> LPs have too much committed to venture (for now). So they are not only fine if VCs slow down the pace they invest, in some cases, they are strongly suggesting it.

-> LPs want to slow down when VC funds “come back to market”, i.e. ask for another fund. So the longer, as a VC, you have to wait to raise another fund, the more slowly you’ll invest the current one.

-> LPs are worried about the amount of cash all these funds will call. When a VC fund raises say $1B, it rarely “calls” it all. It generally calls that money from LPs over a decade. But VCs raised so many new funds, and bigger funds, so quickly, that LPs just want in many cases for it all to just slow down.

So while you’d think all this so-called “dry powder” will create investment velocity, really for now, in 2023, it’s the opposite. Right now, VCs’ own investors just don’t want them to call it and invest it. They’re overloaded already.

That will eventually change. But not likely for some time, and almost certainly not until late 2023 at the earliest.

So net-net, don’t count on “dry powder” creating a lot of desire to fund you in 2023. It might seem like it should be the case. But the reality is, it works the opposite. At least in the short term.

A lot of conclusions based on LP behavior in that. So let’s hear what three European LPs say to that!

While the situation is certainly different for many LPs, we are happy to chip in with our two cents and share our POV.

In general, we think the assessment in the post reflects the current market quite well. It's basically like a domino - institutional LPs are often over-allocated, the net worth of HNWIs has decreased significantly in many cases, FoFs are having trouble fundraising… GPs are seeing this as well and they understand that if they come back to LPs for cash while not giving portfolio companies enough time to progress significantly, they will have a hard time raising their next fund. This then translates into a more cautious deployment cycle for everyone involved and we don't see this changing in the first half of 2023 at least.

For us specifically, we have the privilege to see things from a bit of a different standpoint. When a GP successfully gets through our very selective DD process, we essentially acknowledge their skill of investing and shift all investment decisions to them. This means that if they think it's best for them to hold the horses for a bit now and slow down, we're happy for them to use their entire investment period which is often defined between 3 and 5 years. At the same time, if our portfolio fund sees great opportunities in the pipeline on which they would love to capitalise, we're going to be cheering for them and we'll be glad to wire any capital calls. A part of the GPs' skillset is the 6th sense to know when to invest and when not to invest - which holds true in a bull market, but even more so in a downturn. Being in venture for 10+ years allowed us to nurture relationships with some outstanding GPs and gave us the opportunity to see the greater picture. We're in VC for the long run due to our core beliefs, not because the sector was hot a year or two back.

Connected to the statement that various GPs currently benefit the most from various investment paces, it is a part of our job to make sure that the LPs don't limit the GPs in doing what they do best, aka. investing. What this means is that, aside from the cases where we back a first-time GP as their first believer/before anyone else, a part of our DD process is also going through the list of other LPs and assessing, whether the LP structure is appropriately diversified in order to support the fund over multiple cycles. The ideal scenario is to have large institutions supplying a majority of the capital, but at the same time having a wide range of entrepreneurs on board, who might have smaller checks, but provide tons of value.

To summarise in a single sentence, it’s obvious that the ecstatic mood from late-2021 is long gone, and it’s not coming back anytime in the near future, but as hinted on by several people from the ecosystem already, the ratio of nonsense startups/funds decreases in times like these, creating a great time for everyone to look back and re-evaluate, what is an actual solution to an actual problem, as opposed to a marginally better solution to a non-existent problem surviving on VC money and hype.

In general I would agree but two points he is missing imo:

1. Not every fund (especially the smaller micro funds) is backed by institutional LPs. Many of them are backed by individuals from the ecosystem that still strongly believe in VC and are willing to allocate during a bear market. However, we've also heard from some emerging managers that even individuals have slowed down their deployment pace to companies and funds, as they too are overallocated to venture.

2. Even though Deal velocity will go down and VCs might struggle to raise at the same pace as before there is a lot of potential for secondary activities (on both sides). This a) bears a lot of investment upside and b) also allows the investor bases (on the company and LP side) to get more diverse.

IMHO, what Jason did not touch on is the possible scenario of fund downsizing - many VC funds raised very large funds in the last two years, believing that the high revenue multiples environment was sustainable, thus claiming they can still generate outsized returns with large funds. However, some of these VCs will either reduce their currently active fund sizes and/or raise smaller successor funds.

On the secondary side - we will see many secondary opportunities in the next couple of years, both GP- and LP-led, coming from non-traditional or what we call them "Tourist VC Investors" that will look to strategically liquidate their positions as well as GP-led secondaries from VCs looking to show DPI to be able to raise subsequent funds.

We’re definitely happy to see - certain - VCs deploy more slowly (think 2-3 year deployment periods vs 18-24 months) but that doesn’t mean we’re happy if they don’t deploy at all.

We’re big believers in investing through thick and thin and in the relative inability of investors (even the best of them) to time the market. Hence a healthy level of investing each year is preferred to no investing at all.