The Lowdown | 26.08.22

The show that wraps up the week in European Venture 👀 - and what a week it's been!

Welcome to another busy week in August (the busiest so far? Seems like summer isn’t stopping anyone this year🏃♂️💨)

Wanna co-anchor the show with us? Reach out - we’re always keen to play ball! Right now, we’re VC & male heavy, so if you’re a founder or woman, we’d be truly excited to hear from you and bring your perspectives into the ring!

Wait what!? Why so focused on getting a female anchor? We’ve got a problem 👇

The gender problem in startup land:

All-men founding teams raised 89% of venture funding.

All-women founding teams raised 1.8% of venture funding.

Mixed-gender teams raised 9.3% of venture funding.

The gender problem in VC land:

85% of VC GPs are male, 15% are female.

91% of male GPs have access to carry. Only 70% of the female GPs have.

The gender problem in LP land:

Only 20% of VC interactions with LPs are with women.

Only 53% of these have actual decision-making power (53%).

Data from the European Women in VC report by Kinga Stanislawska, Isomer Capital, Speedinvest and others.

Don’t pretend to be something you’re not.

Over the last few weeks we’ve seen to many founders not be who their PR says is. Dan Price being the one spotlighted here, but it could’ve been many others.

But it raises the question; while sexual misconduct and the like is an obvious red flag that no-one should condone, venture land is a game of extremes, the power law and where most of us are probably somewhere on the spectrum. Outlier results come from outlier personalities.

So how should we think about this in VC? 🤔 Cristobal from Startup Wise Guys shared his philosophy around cohort creation and the maximum threshold of narcistic, dominating founders with psychopathic tendencies - saying that the magic number is probably 1 or 2 teams out of a cohort of 20 (fact check me by listening to the episode here).

Fact of the matter is; there’s the human side where you might say “that’s ugly” but there is a psychopathy to building and running a startup, so as an investor you will need to find out how you navigate that and walk the fine line.

Replay the show to hear Dan’s deliberations around working with a psychopathic founder at minute 7:00.

Read the original article here.

Mentioned startup in the spot; Hypt.

Blitzscaling still in vogue - SPACs a different story

First a fun and completely irrelevant note for the topic at hand: Reid hates trump and is quoted for calling him “a Chernobyl…within the U.S. system.”

On blitzscaling the article points out that “the concept looked less convincing when recent blitzscalers including Coinbase, Peloton and Robinhood—all of which hired fast, spent extravagantly and raced to enormous valuations—crashed back to earth when the market turned.”

But for Reid Hoffman, he’s mostly mostly unapologetic. “Hindsight is always 20/20,” he allowed, but “all the principles of blitzscaling still apply.”

Or as Dan put it in the show:

There’s nothing is wrong with Blitzscaling if you have a working profitable model. But if at any point you cannot turn on profitability and your business model is bonkers - that’s not cool.

And along this vein of changing business and go-to-market models - or the perception of them at least, David Peterson from Angular Ventures put out a great post on the the over-hyped status of PLG-based models commenting in summary:

By publicly eschewing the need for sales reps, Atlassian and Slack really messed with the heads of a generation of entrepreneurs.

SPACs are a different story though. [12:00]

In the article, Hoffman is a bit more remorseful about the SPACs; “having engineered two deals that have worked out horribly for public market investors. Autonomous car startup Aurora, which Greylock had invested in as a private company, is down 70% from its November initial public offering price. Joby Aviation is down 40% since its IPO a year ago.

“I got drawn into the SPAC stuff on the theory that—and this is one of the things that I have some regrets about—[they provide] a kind of democratization of the public markets and ability for people to participate,” he said.

SPACs, in other words, allow ordinary investors to invest in VC-stage outfits. “That impulse is good,” said Hoffman, “but I’m not sure the public markets are really ready for that sort of thing, especially in downturns.”

It was never going to work where you could have an empty vehicle where everyone could invest where you just don’t know what’s going to go in there and you just know by proxy that it’s going to be all the stuff that’s not working in the real world that’ll go in that pot. SPACs were never a good idea.

Read the original article here.

Democratization of VC [15:00]

But this does beg the question; what about the trend towards democratization of VC in general? Are there learnings to be made from the fate of the SPACs?

We believe there is. There is a need to curate deals and not just work out a platform where all deals are accessible to everyone. At EUVC we’re building quite a few syndicates into venture funds, bringing the ecosystem together around investing into some of the best European VCs - established as well as emerging.

When we do that, we deliberately put our own cash at risk (GP commit - more on that topic later!) so at least there’s that level of curation. And we focus on funds rather than direct deals to ensure diversification through that. But for sure, investors need to educate themselves before they put there money in 📚 .

But there’s another side to democratization - LP perception.

Every time we do an LP syndicate we have the same conversation with GPs: how will LPs react to this? Fact of the matter is that many don’t like it too much. Even though a syndicate of investors from the all across the European ecosystem can work as a beautiful extension of the team. Think deal sourcing, value add to the portfolio and understanding of tech/markets/industries outside of the fund’s typical sweet spot.

But for some LPs, there’s a perception problem, they don’t like things that are out of the ordinary, etc., etc.. And that is something we need to change. ‘Cos in our views; democratization of VC is coming, it’s only a matter of when.

What we’re seeing with our syndicates is; they’re quite powerful and they will become a competitive advantage for the funds that nail how to manage a broad cohort of small tickets investors backing their fund.

Join the euvc community syndicates here.

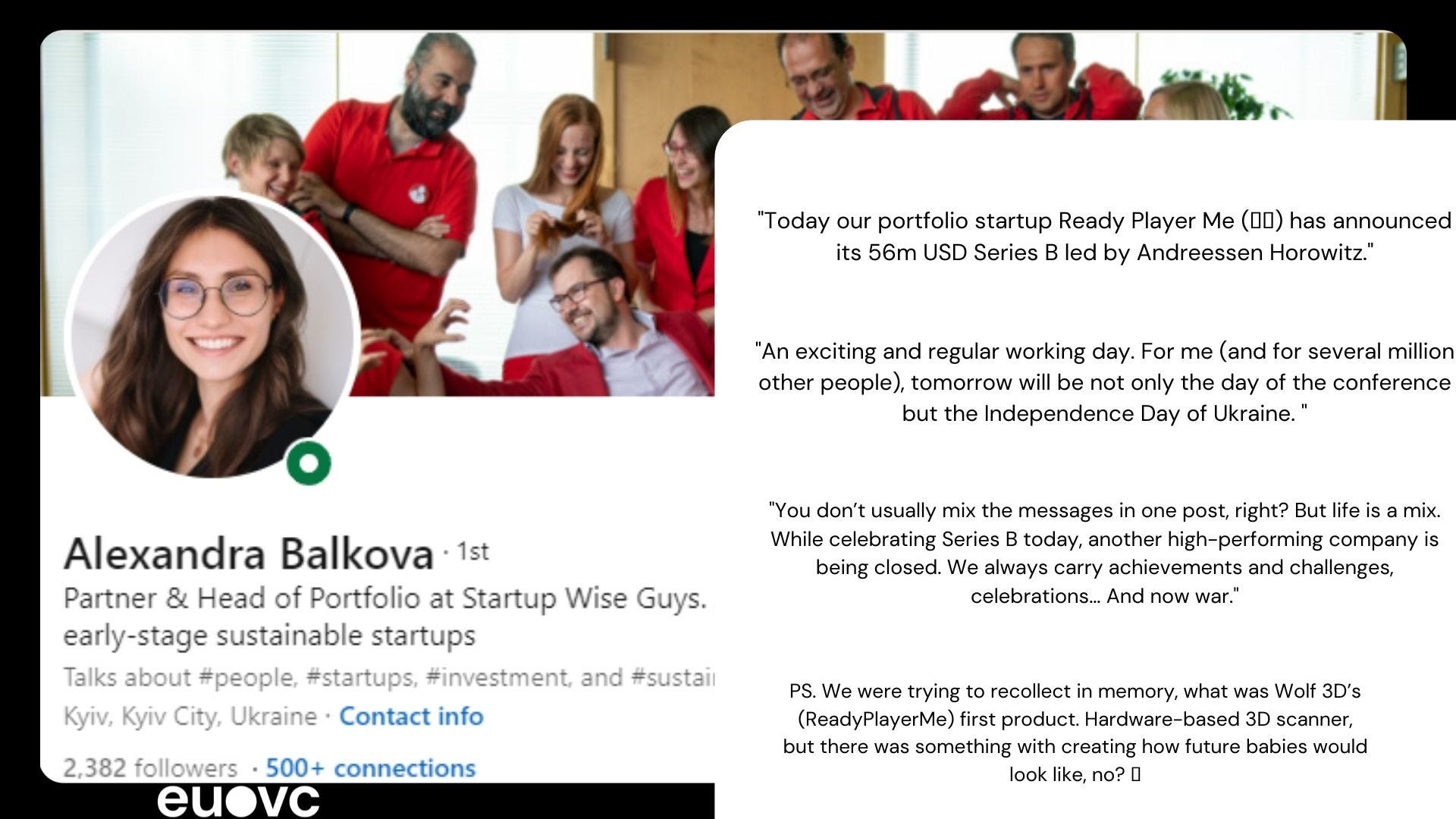

a16z joins Startup Wise Guys Series B & The War

We wanna highlight this post by Alexa from Startup Wise Guys.

It shows so clearly the way Europe has changed after the war in Ukraine. The same day as Alexa and the SWG team can celebrate the raise of a 56m USD round led by a16z into Ready Player Me, they can wait for the National Flag Day of Ukraine coming the day after where the tensions of the war were high. Absolutely heartbreaking.

And if you can, do support the founders, VCs and whoever you might be able to help in the Ukranian community.

Read the original post by Alexa here.

Shout out to a real leader: Sanna Marin

We just wanted to show our support to Sanna Marin and remind all to remember this front page image of her, rather than the party picture being shared everywhere. She’s a leader, a public servant and she’s doing a huge service to her country. Hats off.

Return to Office bites the Apple [23:00]

When we see the stories of uprising against “back to work”, it’s important to remember that in the story of Apple, as an example, 600 people out of 12,000 signed the petition, but in early stage startup: does fully distributed work? Dan isn’t so sure.

I get punched in the face for this a lot, but fully distributed in the early stages - pre product and PMF - just doesn’t work. As a rule; don’t put blockers in the way where you don’t need to. Get as much as possible out of the way so you can focus on building.

Andreas does have a caveat though:

We’re seeing some teams come together that would otherwise never have come together to form a startup. I think that’s important to remember.

Read the original article here

Startup of the week

Garvis

Shameless plug by Dan here: Superseed have just invested in Garvis. Why?

I’ve seen in a long time. TTV 1 day. White box solution. 2-5% efficiency gains. Which in enterprise is MASSIVE.

And on top of the gains for the customers, there’s also a save-the-world angle: every time we improve efficiencies in the supply chain (especially manufacturing), we’re doing us all a favor🌳.

VCs of the week

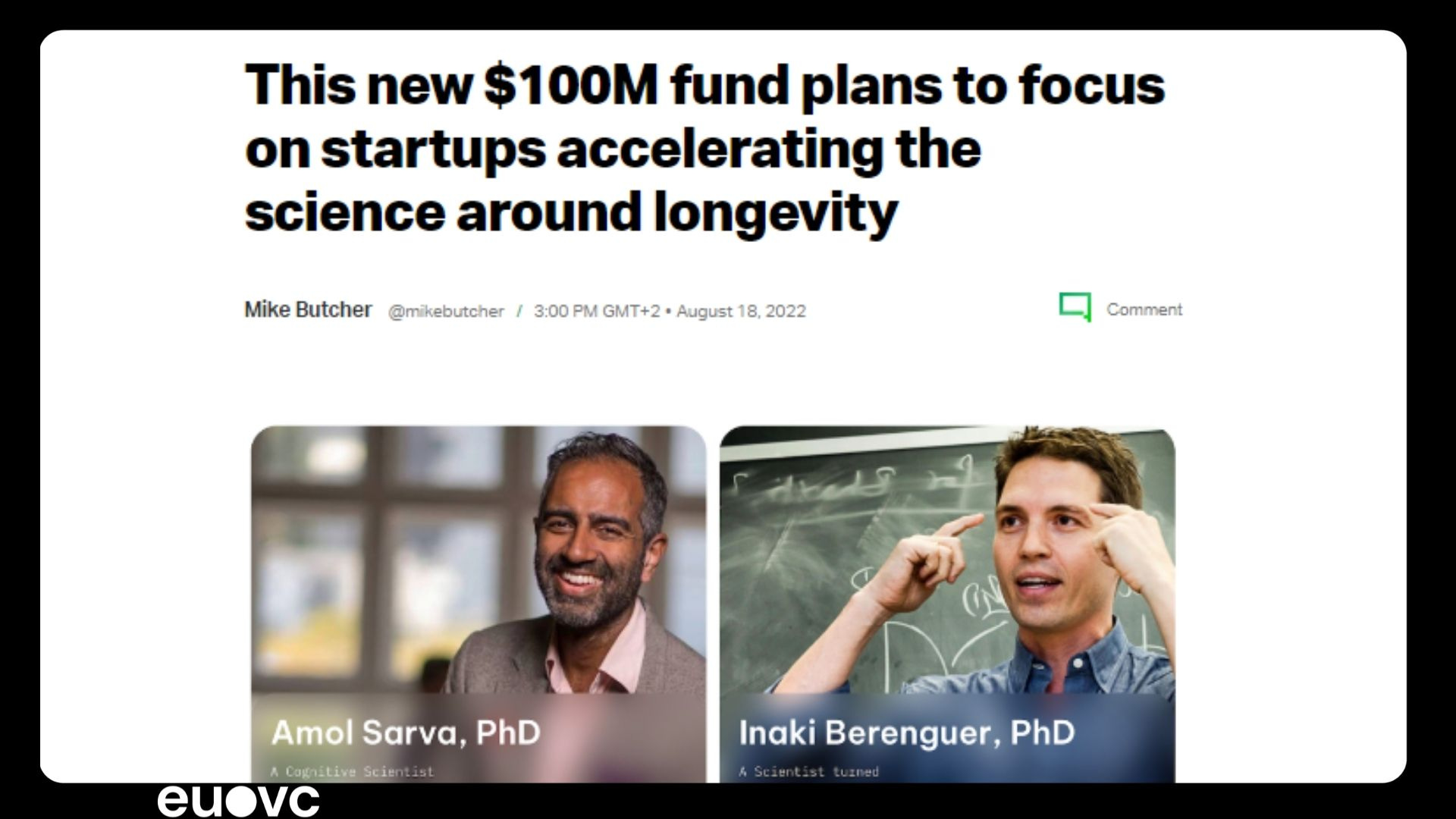

Life Extension Ventures

Just because we love longevity. Shout out to Life Extension Ventures - we hope you’ll allow us all to spend a little more time on this earth 💖🌍

Read the original article here.

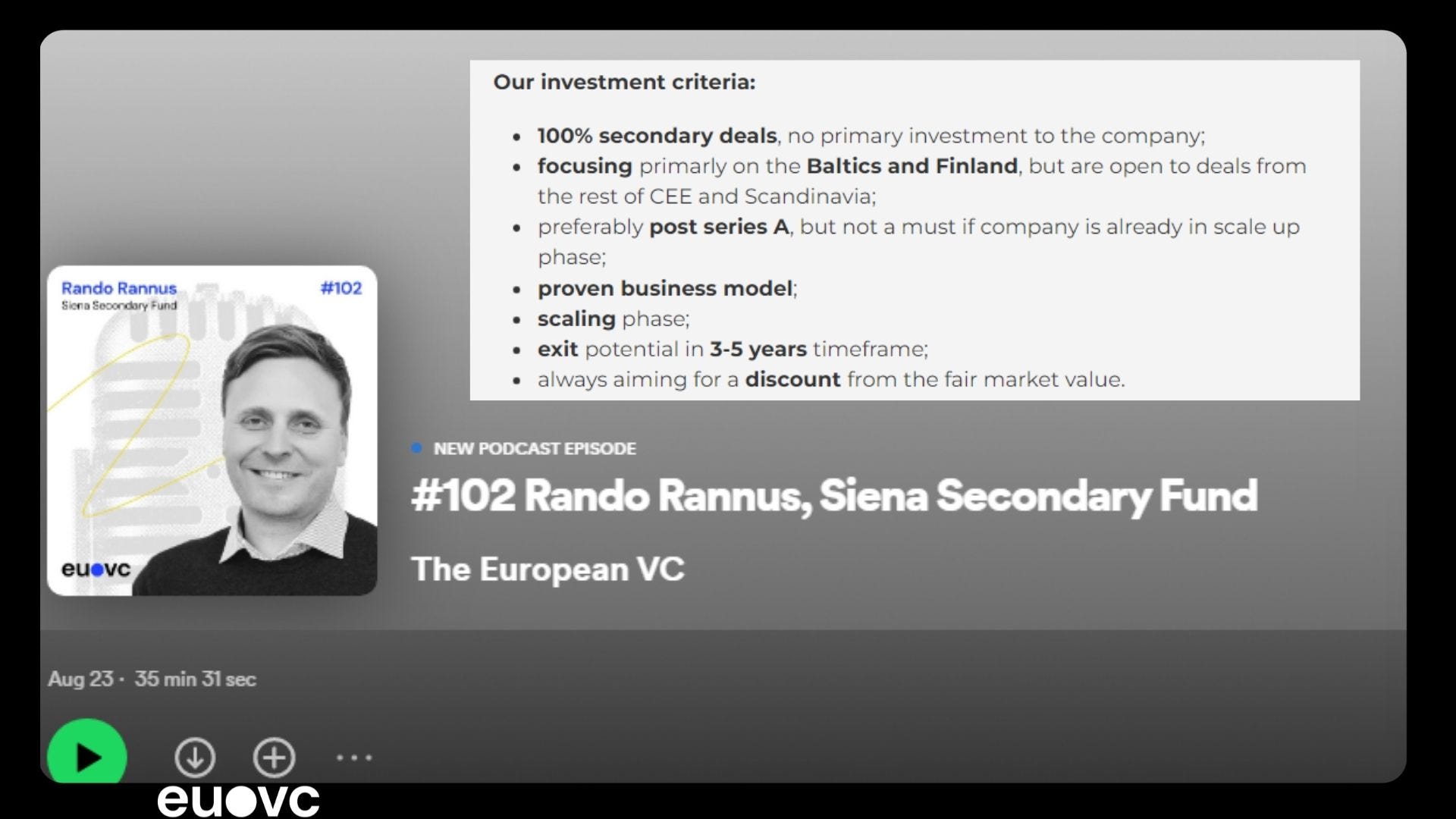

Siena Secondary Fund

We’re entering into a new era in European VC. We’ve never had an emerging manager raise a secondaries fund focused at the Baltics. Now we do.

So while this is shameless self promotion of our EUVC pod episode from this Tuesday (sorry), we thought it was fair enough bringing. And on top of that, it led to the Andreas’ learning of the week 👇

What we learned this week

Computer says no: Paper money doesn’t cover the GP commit

As European VCs are getting bigger and bigger and also younger and younger, we’re seeing a real crunch for many GPs. How does one come up with the GP commit for 3x bigger new fund, when distributions have hardly started from the last fund(s)?

It’s incredibly perplexing and we’re seeing it more and more. I don’t know if I should name the inventor of the following quote, so I won’t.

We’ve taken to calling it our “cash for houses”-program internally. ‘Cos 9 times out of 10, that’s what the GPs need to finance - together with the GP commit it can be really difficult.

Anyways. Core message here being, we feel ya, selling GP commit, much less carry, can be difficult to swing. So do reach out if you’ve got this issue. We might know someone who can help 🤗

Finding Product-Market Fit? How do you know when you’ve got there?

Dan talks about this a fair amount. So let’s hear it from him:

“I had a hard time with this personally in my #startups. The #founders I work with sometimes do too. Here are some ideas (love yours) around how you know what product-market fit is via proxies that show when you’re tipping the velvet:

You’ve Bottled Founder #sales

- When you’re able to systemise and process’ise sales.

- Someone else is now sales lead.

- Lots of caveats here around success and stability of that sales success over time. Which are all pretty obvious depending on your style of business.

- If lower ACV - you’ve systemised inbound.

Full Fee

- ICP 1 clients are buying you on model at full asking price.

- You are in growth mode, with a sniff of scale at choice (diverging cost base from margin from either side).

- You’re not running at growth at all costs by packing investor cash into the marketing column.

You Get Referred

- ICP clients refer to similar ICPs.

- They’re not prompted and inbound requests have been pre-qualified i.e. you don’t have to sell because the referred client already knows and loves the value you add.

Measured Churn

- Over a period of time - at least 4 months, you can measure and predict churn. Ideally zero but that’s just not reality.

Short Sales Cycles

- As a guide, your sales cycle should be less than 3 months regardless of ACV.

- Self serve will obviously not count here but longer sales cycle might be problematic (yes oc there are outliers).

Once you've found #productmarketfit it's into serious growth mode.

And when ready, you're into scale.”

Come meet us 🤗

Final shout of the day is: we’re gonna be at TechBBQ on the 13th - 15th and How To Web in Bucharest from the 20th to 22nd. So if you are too, do reach out!

We’re gonna do a side-event for each, so join the EUVC community and we’ll circle back with the deets✌️